Private equity has stumbled in the short term, but history is clear: Past periods of underperformance were followed by strong multi-year rebounds – setting the stage for what could be the next upswing.

Recent Performance

If you thought distributions were a sore spot for investors, let us outline the performance discussion for you.

PE is lagging while public markets sit at record highs, driven by the Mag‑7 and short‑term FX noise. History says this gap snaps back rather than remain extreme.

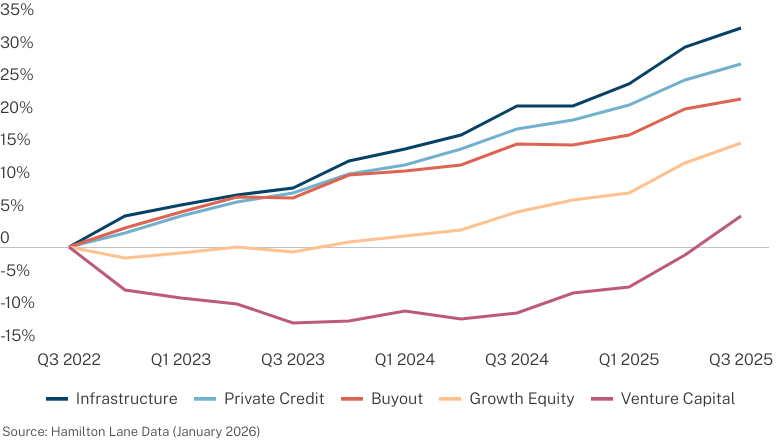

3-Year Cumulative Return

Cumulative TWRs Q3 2022 - Q3 2025

Infrastructure and private credit have been very strong performers over the last three years. Their cumulative performance has beaten buyout, growth equity and venture capital. But, again, we are investors, so let’s focus on the problems. It’s on the equity side.

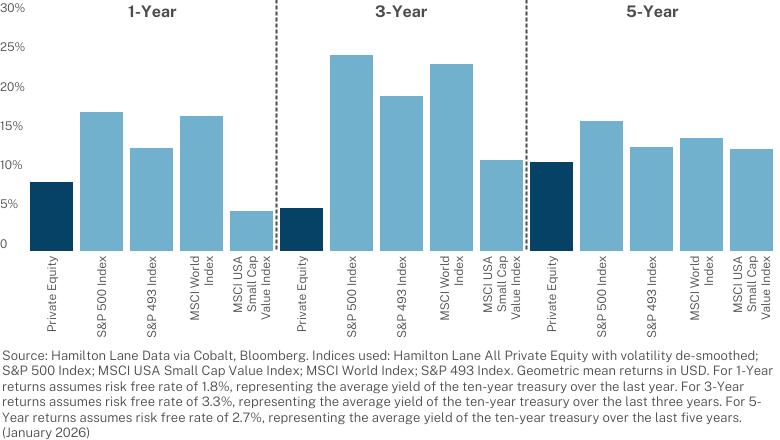

1, 3 & 5-Year Private Equity Performance

Annualized Time-Weighted Returns as of 9/30/2025

You can measure performance over a one-year, three-year or five-year period and you get the same result: Private equity has underperformed against almost all the public benchmarks. We included the S&P 500 with and without the Magnificent 7 and, while the underperformance may be less, it still underperformed.

No, we can’t predict the future, but we can make a pretty compelling case of what the odds are for the future course of prices.

Longer-Term Performance

We normally talk about returns in the private markets over a 10-year time frame. The theory is that we are all long-term investors, particularly in the private sphere. It’s a fiction; we all understand that now. We spend more time discussing quarterly and annual returns than we ever do discussing 10-year returns, but let’s at least look at the numbers over longer periods:

Have we reached the end of an era? Has private equity outperformance come to an end? Not so fast. Let’s add some context.

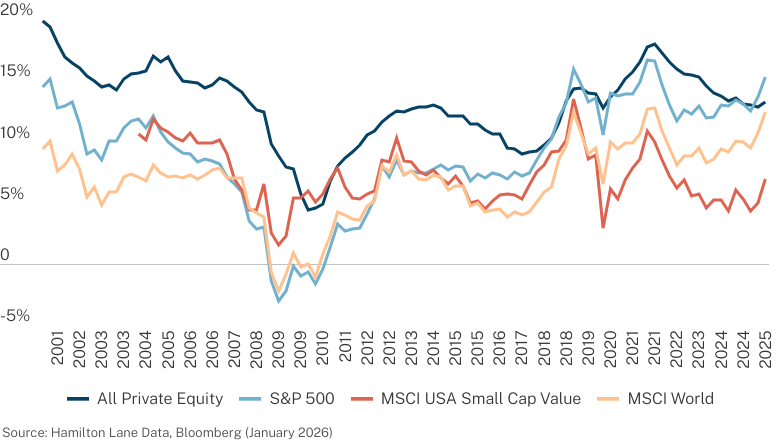

All Private Equity 10-Year Rolling TWRs

The underperformance of private equity occurred more recently and the outperformance against other benchmarks remains. We also note that there have been other times over the last 25 years where the 10-year period showed underperformance on the private side: 2011 and 2019. Both periods were followed by strong outperformance.

Pooled Returns by Vintage Year

Buyout IRR vs. PME

Real Estate IRR vs. PME

Credit IRR vs. PME

Infrastructure IRR vs. PME

We have always liked these charts. It gives such a good representation of the vintage year-in and year-out movements and comparisons of the various markets.

- Buyout, no surprise, has outperformed or been in line with publics in every vintage year except the last four. The concerning part is that the underperformance has not gotten better. It has, perhaps, gotten worse.

- Private credit has outperformed its public benchmark every year for the last 24 years.

- Private real estate, for all the return tarnish it has endured since the Global Financial Crisis, has outperformed for the last 15 years.

- Infrastructure, like private equity, has struggled to outperform recently, largely due to the public market AI-oriented infrastructure stocks.

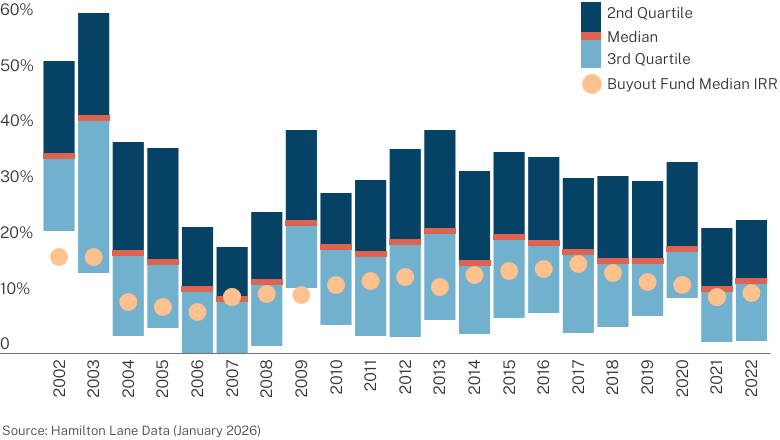

Looking at how different deals in the buyout sectors have performed in each vintage year, we have a plot twist nobody saw coming: Energy & Utilities.

Gross Buyout Deal IRR Quartiles

By Deal Year

Take a look at those numbers. This is why everyone wants to be a general partner. Sure, 2021 shows a marked decline in the median return at the deal level. It’s only ~10%. If we told you that there was a place where, over the last 20+ years, your worst year was around a 10% return, your best year was around a 40% return and your average return was around 18%, would you say that's the best investment ever?

You’d be right. Don’t overthink this. Private equity has been, and likely will continue to be, an incredibly attractive investment space. It is not just luck, or a moment in time, or whatever explanation skeptics provide for its performance. It’s a skill set, a superior governance model. This isn’t that hard to figure out.

![]()

Interested in learning about the data & tools that power our insights?

Connect with our tech solutions team.

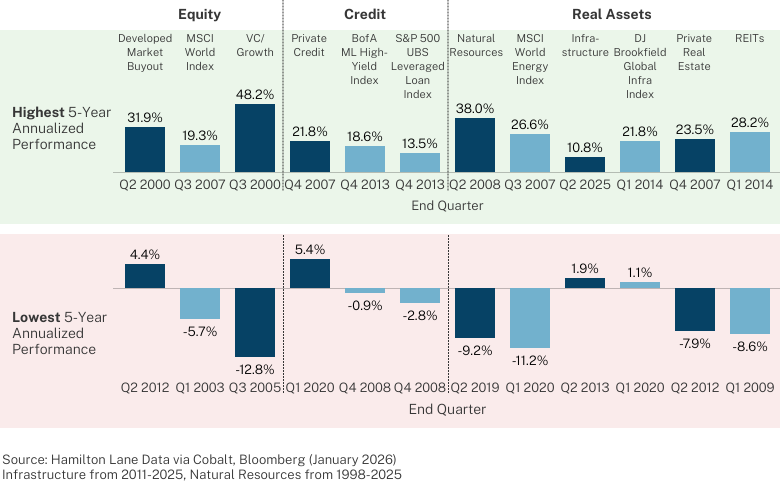

Worse Comes to Worst

This may not be the most important chart in the overview (although that is an almost infinite well), but it may be our favorite. We just pointed out how amazing the returns have been for the last 20 years. We’d fully expect that the price for those returns is greater risk of loss. Nope.

There has been no five-year period in the history of buyout returns or private credit returns or infrastructure returns (for infrastructure, since 2011, so not quite the span of history) where you have lost money.

That’s extraordinary enough, but then note that, for all that downside protection compared to the public options, your highest five-year returns exceed the highest five-year return in the public world.

Persistence in Performance

One question we are often asked is, “What is the persistence of performance in private markets?” Over the last 20 years, top-quartile persistence has been greatest in venture capital, growth and real assets and least in buyout and credit. It’s not as persistent as you would want given the maniacal focus some investors have on only investing in top-quartile funds. It is much better if you are looking for top-half performance.

Let’s consider the probability of persistent fund performance. In other words if a manager outperforms can they do it again?

2026 Market Overview Narrative

Our annual report offers a unique perspective on the private markets, leveraging our firm’s industry expertise, research capabilities and expansive database to help investors navigate the evolving investment landscape.

Dive deeper into the data with our full narrative, a comprehensive exploration of what’s driving markets now.