Evergreen vehicles are quickly becoming one of the industry’s most dynamic growth engines as investors embrace a simpler, more intuitive way to access private assets.

The most impactful box we’re opening in the private markets may be the evergreen, semi-liquid vehicle box. The development and use of these vehicles will, we believe, have both positive and negative effects across the private markets and in ways that are difficult to predict today.

The most common reason given for the growing use of these vehicles is that they are semi-liquid. That is important, but there’s a different feature that is core to our thesis for their continued adoption by investors—evergreens follow consumer/investor preference for simplicity. A well-known example is Robinhood, a company whose success is predicated on delivering on its core premise of democratizing finance by offering easy-to-use trading tools and low barriers to entry. Think of evergreens as the Robinhood of the private markets. Let’s compare closed-end funds and evergreens.

Let’s be honest here: The closed-end model is a royal pain in the rear for the investor. They have to worry about how much to invest to reach an allocation target. They have capital calls and distributions that are coming and going at random times. They need an army of accountants to keep track of everything. Returns are measured in IRR.

The evergreen model turns that equation around. For the general partner, evergreens are a challenge. Look at Hamilton Lane. We have over 60 people dedicated to portfolio construction and liquidity management. Those numbers simply aren’t needed for closed-end vehicles. The general partner has to manage cash flows and determine proper portfolio allocation on a dynamic, not static, level. Reporting and cash flows must be managed daily.

For the investor? It’s easy. You make a one-buy decision, and you have full allocation. No bewildering and endless calls and distributions and incomprehensible tax reports that arrive 20 years late. You have returns reported on the same basis as your public holdings.

What business model has the more appealing structure for most investors?

Evergreen.

Does that mean it’s the answer for every investor? Of course not. Many investors have an infrastructure equipped to deal with closed-end funds, so simplicity is not a priority. Also, many investors prefer the flexibility a portfolio of different partnership vehicles can give them. But evergreens’ ease of use offers a choice to new and existing investors that did not exist 15 years ago and we believe that market channel will continue to grow, perhaps more than many expect today.

If there’s one area in the private markets that’s really shaking things up, it’s the evergreen funds.

A criticism of evergreens is that you are sacrificing return for ease of use and the lure of liquidity. The data shows a different story.

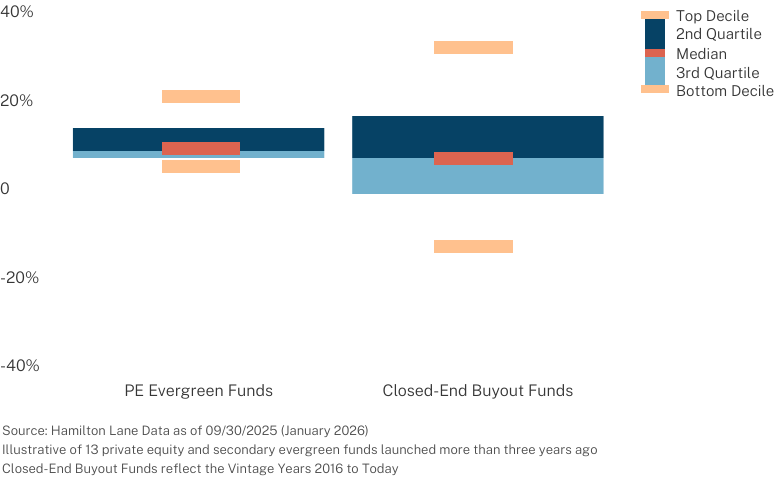

Annualized Return by Fund Structure

Over a one-year period, private equity and secondary-focused evergreen funds have outperformed buyout funds. Oh, you say, one year is too short to measure.

Evergreen outperformed over three years also. We do note that evergreen equity funds still underperformed the public benchmarks. Let’s look at dispersion of return as a measure of risk. First, the one-year numbers.

Trailing 1-Year Dispersion of Returns

You can get a much higher return from a closed-end fund than an evergreen fund. You can also make a great deal less money. You want a specific example? Over the last year, about a third of your closed-end buyout funds would appear, in your financial statement, in the loss column. Not good. On the other hand, it didn’t matter what evergreen fund you were in. The worst you would have done was a mid-single-digit return, which maybe not so coincidentally is the average return of your closed-end portfolio last year.

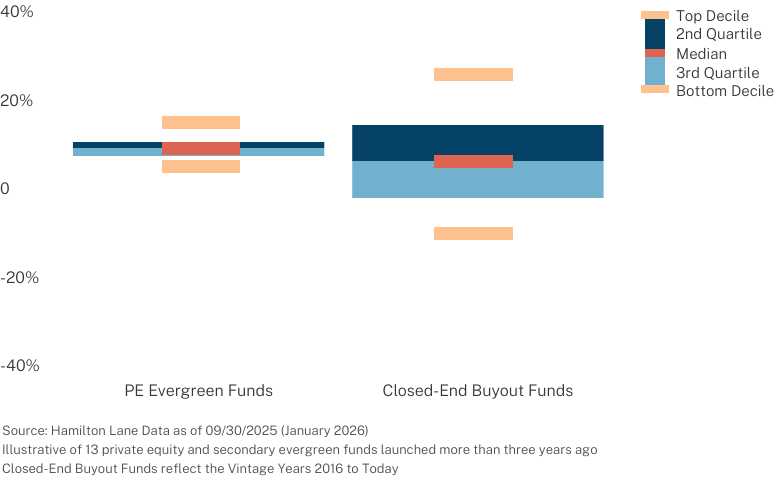

Yes, the dispersion of returns is much narrower for evergreen funds, but, over a year, there is still 600 basis points between top and bottom quartile. Selection does matter. Let’s go to the three-year numbers.

Trailing 3-Year Dispersion of Returns

It is no surprise that the dispersion is reduced in both forms of investing but is still 300 points for evergreen funds. The lower dispersion among evergreen funds makes sense. These vehicles are much more diversified than a closed-end fund. An evergreen fund can be a better point of entry for investors that don’t want the burden of selecting and managing dozens of closed-end fund commitments.

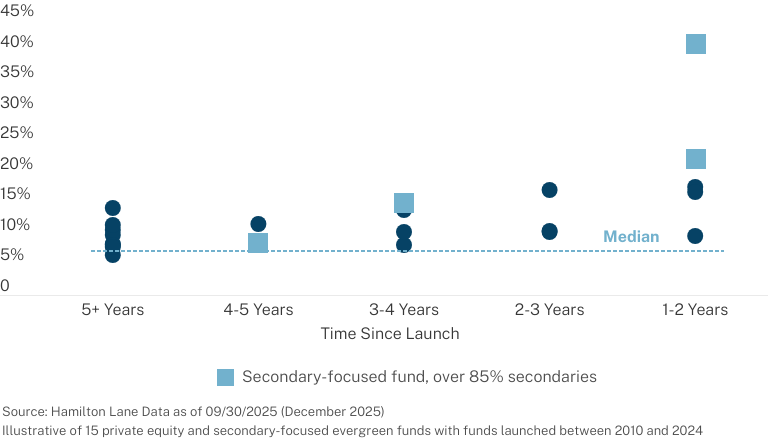

Another criticism of evergreens is that they are just using secondary investments to goose returns and none of it is sustainable.

1-Year Returns of Evergreen Funds

LTM Returns as of 9/30/2025 for funds with at least a 1-year track record

This is still a young market, but there are some conclusions. First, it is correct that first year or two returns can both be higher and more volatile. It is also true that secondary-focused evergreen funds have strong early returns and tend to come down over time. That is, by the way, true of closed-end secondary funds. The returns the secondary-focused funds generate early are not sustainable (those rates well above 20%), but they still have good returns in line with, or above peers after those first few years. Also true is that, even after five years, the selection of your evergreen manager matters a lot.

2026 Market Overview Narrative

Our annual report offers a unique perspective on the private markets, leveraging our firm’s industry expertise, research capabilities and expansive database to help investors navigate the evolving investment landscape.

Dive deeper into the data with our full narrative, a comprehensive exploration of what’s driving markets now.