AI isn’t just another trend. It’s a force reshaping everything. The only real question for investors now is how you choose to embrace it.

We have been arguing for some time that, in the end, all the discussion and worry over interest rates, the dollar, tariffs, etc. is largely overdone. We spend too much time pondering those movements and not enough on the one thing that has driven, and will likely drive, investment returns for the foreseeable future.

That one thing?

Artificial Intelligence. AI.

Period. Full stop.

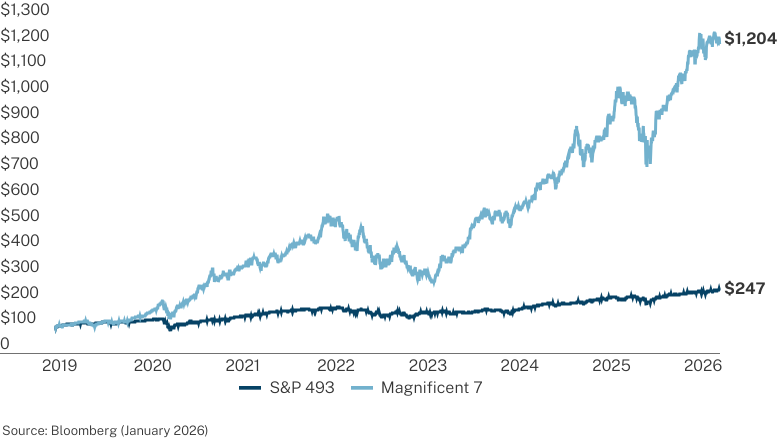

AI now dominates public markets, with a few mega-caps driving performance and creating major concentration risk tied to the LLM story.

AI & the Markets Today

Growth of $100: S&P 493 vs. Magnificent 7

We all know it, but don’t fully acknowledge it. We tell ourselves we have a diversified public stock portfolio with our holdings in “an index.” No, you don’t. You have seven stocks. You have seven AI-related stocks. We said during a recent presentation that everyone should sell all their public equity holdings and buy two or three of the AI-related stocks and go to sleep. Someone came out and frantically said, “This is NOT investment advice!” Yes, it is. Why pretend otherwise? We’re not saying it’s good or bad, but we’re saying the performance of those seven stocks will determine the performance of your public investment portfolio. It has for the last 6+ years. It will for at least the next two or three.

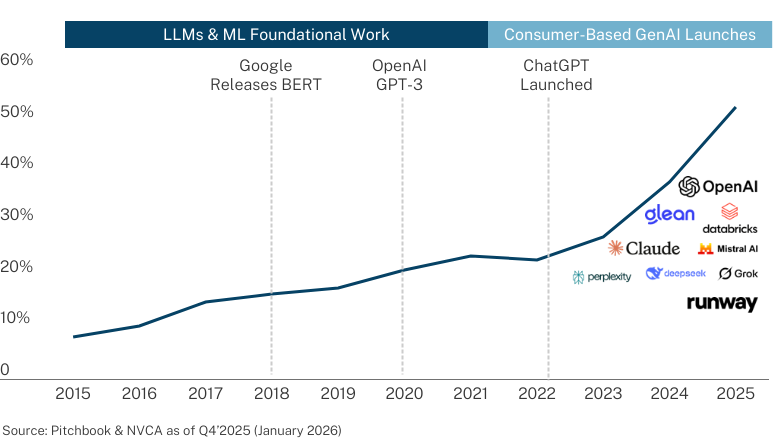

AI investing in private markets is booming, with early-stage VC pouring in and revenue scaling fast, making AI adoption the next big divider between winners and laggards.

AI's Percent of Deal Value Grows Across Venture

As of Q4 2025

It is no surprise that, if you are dealing with a big technology shift, venture capital will be leading the way with investments. It is fair to say that the scale of the movement to AI has been dramatic. Over 50% of deal value in the venture world is now going into AI-oriented deals. We will now utter that dreaded word we hear all the time.

“AI investments are in a bubble that will burst!”

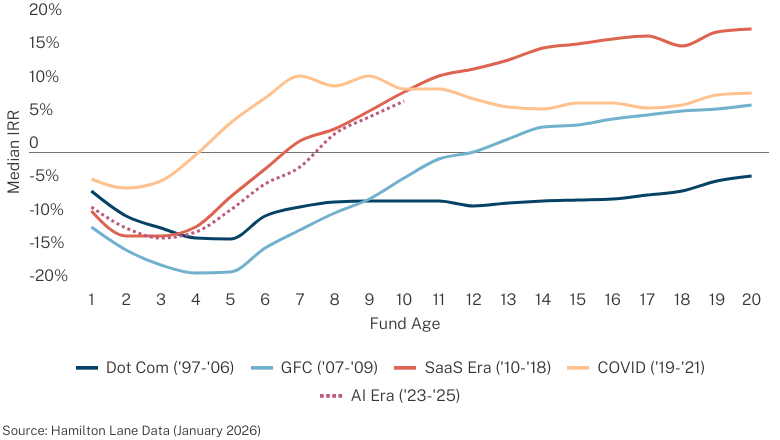

How Could The AI Era Compare to Prior Venture Cycles?

Median Venture IRR by Fund Age

We have tried to compare venture returns during this “AI Era” to prior periods where venture had strong, early returns. It most closely resembles the SaaS era, but we admit it is still early. The AI investments are often compared to the dotcom era, but you can see some key differences. The dotcom period, for all its hype, never had great overall performance. There were some big winners but, overall, it was a dismal investment experience. Our view is that the early performance of AI investments is encouraging and not indicative of a market in a bubble, or overinflated state. But, we say again, it is early.

![]()

Interested in learning about the data & tools that power our insights?

Connect with our tech solutions team.

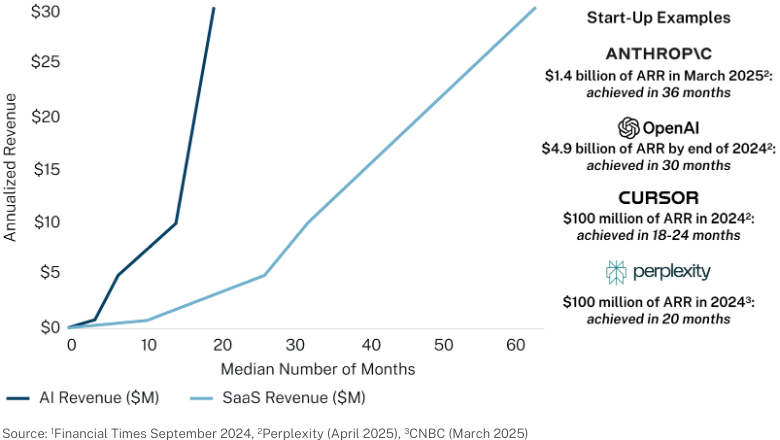

Time to $30M Revenue (AI vs Historical SaaS)1

We do find the comparison to the SaaS period intriguing. It also helps explain why returns have been good early in this cycle. The reality is that many of these companies have more and faster-growing revenue streams than we have seen in prior venture-oriented cycles. There is always the criticism that too much venture investment is premised on promise and not profits. We aren’t saying profits are here, but we are saying that the path to real revenue (that eventually does lead to profits) is happening faster than we have seen with other technology-driven cycles.

AI Bubble

We now get to that question you have been waiting for us to answer. Are we in an AI valuation bubble?

Let’s be clear, we are talking about a valuation question, not whether AI is a real technology that will change how we all operate. The answer to that last question is an emphatic yes.

Our answer to the bubble question is that the odds favor that we are not in a valuation bubble. There are certainly signs that point to it.

- The amount of capital being spent on LLM advancement makes it hard to envision the revenue that will justify it.

- Using addressable markets that include the entire value of the labor market seems a bit overdone.

- Circular funding arrangements that are common now in the industry are suspect. But there are many reasons it’s not.

- The capital being spent is done or sponsored by companies with large balance sheets and cash flows, which is very different from prior “bubbles” like the internet or fiber builds.

- AI can potentially be embedded in almost every aspect of business and life. The revenue models may surprise to the upside.

- The real constraints right now are not lack of demand, but the lack of infrastructure. It takes a long time to build centers and the energy needed to supply them. Ironically, it might be a bubble if there weren’t real-world constraints to letting the bubble happen.

While we somewhat favor the “no valuation bubble” scenario, you have to position your portfolio as if there is a real possibility that there is one.

This is a probability assessment, not a binary prediction model. A 60% probability assessment is close to a coin flip. It means, as an investor, you should be positioning your portfolio for both outcomes while slightly favoring one. We’ll complicate it even more. The public and private markets might not move in tandem here and the probabilities are of inherently different things. For example, would anybody be shocked if going forward LLMs stagnated but applications using today’s LLMs thrived? That might not be a great environment for Mag 7 stock prices, but a bevy of private venture-backed companies would be soaring.

2026 Market Overview Narrative

Our annual report offers a unique perspective on the private markets, leveraging our firm’s industry expertise, research capabilities and expansive database to help investors navigate the evolving investment landscape.

Dive deeper into the data with our full narrative, a comprehensive exploration of what’s driving markets now.