Key Points

- The AI-driven tech revolution is creating powerful investment opportunities, with venture capital emerging as a key gateway to innovation.

- Venture capital now encompasses companies at various stages, from high- potential seed-stage companies to established, revenue-generating businesses.

- Investors seeking high-demand opportunities can access them through established private market fund managers.

The Question Is No Longer 'If'; It’s 'How'

Investing in today’s most innovative AI companies means investing in venture capital. The tech landscape has shifted dramatically, and many investors are no longer asking if they should invest in venture — but how.

Twenty-five years ago, venture capital focused on seed-stage companies which had a wide dispersion of returns. But the venture ecosystem is no longer just a launchpad for fledgling startups, it’s also a powerful engine across the full growth spectrum. This transformation has opened new doors for investors seeking exposure to the disruptive tech revolution.

In this piece we will discuss how venture capital has evolved — and what it means for investors.

1. VC Now Includes High Revenue Deals

Today, venture‑backed companies tend to go public later, once they are generating earnings or they may skip the IPO altogether.

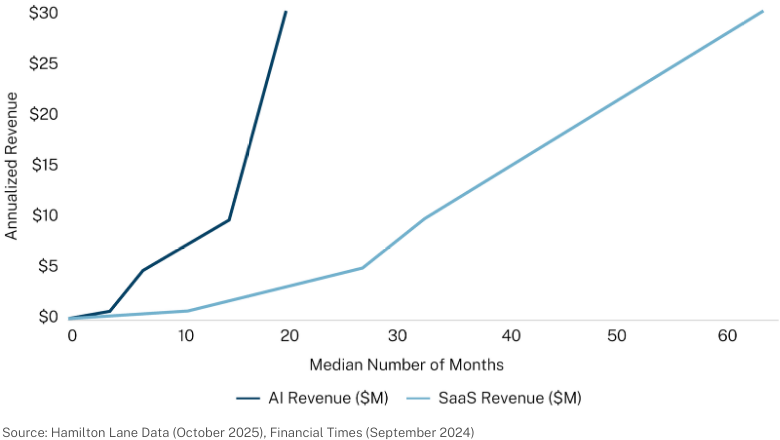

In addition, many AI companies generate revenue at much faster rates than historical tech companies. As the chart below shows, top companies that scale to $30 million in revenue do so about three times faster than traditional software-as-a-service (SaaS) companies1. This has a major impact on venture capital opportunities: In 2024, VC deal activity shifted heavily toward AI.

These changes have broadened venture capital’s scope to include companies of all sizes, from early-stage startups to multibillion-dollar firms.

Top AI Companies May Generate Revenue Faster

2. The Opportunity Set Is More Diverse

While seed-stage companies — offering the potential for high returns, often with high volatility — remain central to VC investing, today’s VC opportunity set is more diverse. Some of the highest-returning opportunities are still in smaller companies. But the addition of later-stage deals brings greater visibility, proven business models and more predictable growth. These companies have moved beyond the proof-of-concept phase, with established products, scalable operations, and expanding market share.

According to PitchBook, late-stage venture deals accounted for more than 60 percent of total U.S. VC investment value in 2024, with AI-focused companies capturing a significant share2. These firms — often pre-IPO or choosing to stay private longer — are delivering returns that rival or exceed public benchmarks, with far less exposure to the write-offs common in early-stage portfolios.

For investors, a combination of early- and late-stage exposure can help capture upside while moderating portfolio volatility relative to an all seed‑stage approach.

3. Access Is a Growing Challenge

However, as venture capital has changed, many top AI deals are oversubscribed, and accessing top-tier opportunities across all growth stages is more challenging.

Access often depends on partnering with experienced managers. Established private markets platforms can open doors to primary, co-investment and secondary opportunities that are otherwise difficult for most investors to reach.

Here's what to watch for when evaluating venture exposure:

- Focus on quality. Wide dispersion and the power law — where a few companies generate most of the returns—make it critical to invest with top-tier companies and managers.

- Consider liquidity. With companies taking longer to go public, holding periods are lengthening. Consider semi-liquid evergreen structures to gain access.

- Diversify. Mitigate risk and capture upside through thoughtful portfolio construction.

Conclusion: This Is Not Your Dad’s Venture Capital

Venture capital investing has evolved significantly over the past two decades. Today, fund managers with scale and deep networks can provide access to the full lifecycle of innovative private companies, from seed to scaled private growth.

Allocating to a semi-liquid evergreen fund with a venture capital focus can provide exposure to innovation while mitigating portfolio concentration. By including growth-oriented companies across various stages and revenue profiles, these funds inherently offer diversification and the potential for an attractive risk/return profile.

1 Financial Times, September 2024

2 Pitchbook, December 2024

This presentation has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this presentation are requested to maintain the confidentiality of the information contained herein. This presentation may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates, and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable, but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

Certain of the performance results included herein do not reflect the deduction of any applicable advisory or management fees, since it is not possible to allocate such fees accurately in a vintage year presentation or in a composite measured at different points in time. A client’s rate of return will be reduced by any applicable advisory or management fees, carried interest and any expenses incurred. Hamilton Lane’s fees are described in Part 2 of our Form ADV, a copy of which is available upon request.

The following hypothetical example illustrates the effect of fees on earned returns for both separate accounts and fund-of-funds investment vehicles. The example is solely for illustration purposes and is not intended as a guarantee or prediction of the actual returns that would be earned by similar investment vehicles having comparable features. The example is as follows: The hypothetical separate account or fund-of-funds consisted of $100 million in commitments with a fee structure of 1.0% on committed capital during the first four years of the term of the investment and then declining by 10% per year thereafter for the 12-year life of the account. The commitments were made during the first three years in relatively equal increments and the assumption of returns was based on cash flow assumptions derived from a historical database of actual private equity cash flows. Hamilton Lane modeled the impact of fees on four different return streams over a 12-year time period. In these examples, the effect of the fees reduced returns by approximately 2%. This does not include performance fees, since the performance of the account would determine the effect such fees would have on returns. Expenses also vary based on the particular investment vehicle and, therefore, were not included in this hypothetical example. Both performance fees and expenses would further decrease the return.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of 11/18/2025