Venture Secondaries and AI: $80B+ in Liquidity Potential

.jpg?language=en-US)

Executive Summary:

- AI innovation and sluggish exits have sparked robust VC secondaries opportunities.

- Venture secondary market penetration remains less than 20% of a $100B+ total addressable market (TAM).

- Firms with capital and expertise can unlock liquidity now.

Investor interest in artificial intelligence (AI) continues to reach new heights as AI drives unprecedented innovation and growth among startups and established companies alike, dominating deal flow and fundraising round after round. This strong demand, paired with oversubscribed fundraises and high valuations, can prove challenging for investors seeking stakes in the fastest-growing companies today. Simultaneously, GPs, LPs, companies and shareholders have all become increasingly motivated to find alternative paths to liquidity as the sluggish exit environment persists. The solution? We believe turning attention to the venture capital (VC) secondary market can help investors gain access to attractive upside potential from highly sought-after AI companies, while giving GPs and shareholders liquidity options, especially as the market continues to grow.

AI accelerates venture revenue growth

AI’s transformative potential and the expanding secondaries opportunity set, combined with today's exit environment and active shifts around portfolio management, have created a uniquely attractive venture secondary market. In addition to newly formed companies benefitting from building from the ground up with AI, existing companies are leveraging AI to innovate faster and operate more efficiently. In many cases, this yields accelerated revenue growth and improved profit margins.

For example, in 2024, Databricks, a unified platform for data and AI, saw revenue growth reaccelerate to 60%+ year-over-year from 50%+ year-over-year, while simultaneously achieving positive cash flow; the company attributes this reacceleration in growth and improved efficiency to artificial intelligence. Founded in 2013, Databricks has spent more than a decade building its business and, in that time, shareholders have consistently sought paths to liquidity for a variety of reasons. And rightly so. Databricks' most recent tender offer, which occurred in conjunction with its Series J, was the largest-ever VC secondary tender offer.

AI is also unlocking astounding growth outside of pure-play AI providers. Take Intercom, for example. Founded in 2011, Intercom is a venture-backed customer support company that has historically offered customer support tools, including messaging, chatbots, targeted messaging and customer feedback features. At the end of Q3 2022, Intercom experienced its fifth sequential quarter of declining net new annual recurring revenue (ARR). In search of a spark, Intercom launched Fin, an AI agent for customer service. Fin grew from $1M to $12M of ARR in a year and has now surpassed the $100M mark in just two and a half quarters since (hitting a 393% annualized growth rate in Q1 2025). Intercom projects that it will have accelerated its total ARR growth rate by 7x by year-end.

Notice that both Intercom and Databricks were founded over 12 years ago. While this AI phenomenon has gained momentum, exits have stalled in the private markets. Last year, there were 14 technology companies that went public with a median age of 13.5 years; 20 years prior, in 2004, there were 61 technology companies that went public with a median age of 8 years.

The strategic choice to remain private

Beyond challenging exit conditions, many companies are deliberately choosing to stay private longer to maintain strategic flexibility. This autonomy allows founders to prioritize sustainable growth, invest in research and development with longer time horizons and make decisions based on fundamental business value creation rather than under the scrutiny of public markets. As Stripe co-founder Patrick Collison explained in a recent interview, "We want to spend the marginal hour with some customers" rather than managing public market obligations and analyst expectations. His brother and co-founder John echoed this sentiment, emphasizing their focus on long-term value creation over quarterly performance pressures.

However, this independence creates a natural misalignment for employees and investors with varying investment horizons and liquidity needs. Just as venture investors enter at different stages, they also need to exit at different stages based on fund lifecycles and strategic priorities. A functioning and maturing secondary market addresses this mismatch by enabling liquidity for stakeholders while supporting companies' decisions to remain private longer.

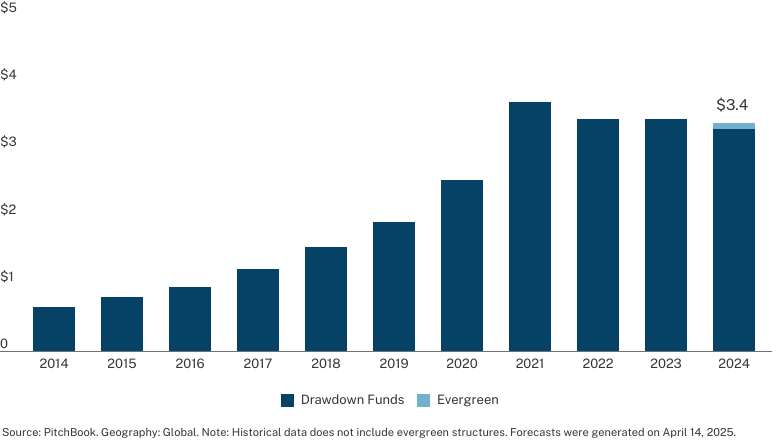

$3.4T in venture capital

Venture Capital AUM by Trillions

Today, there is approximately $3.4T of global venture AUM and we estimate the penetration rate of venture secondaries to be less than 0.5%, while the penetration rate of buyout secondaries is between 2.5 - 3.0%. As penetration increases across both markets, applying a similar penetration rate to the venture secondaries market implies a venture secondaries TAM of over $100B of which currently less than 20% has been penetrated.

Furthermore, given the backlog of companies that have yet to exit and the requirements of companies to IPO in today’s market, we agree with NewView Capital’s Ravi Viswanathan that the venture secondaries opportunity is not simply “going to be a moment-in-time thing.” Additionally, according to Jefferies, venture secondaries volume has grown significantly, representing 22% of total LP-led secondary market volume in H1 2025; it has fluctuated around 8 – 12% of total LP-led volume over the past three years. Active portfolio management is here to stay.

LP Transaction Volume by Strategy

Given the innovation that AI enables for both new and existing venture-backed companies, as well as the continued structural evolution of venture secondaries, we believe that firms with the proper tools, expertise and requisite capital will play a critical role in creating liquidity in this ecosystem. We are excited about the opportunity ahead.

Credit: This strategy focuses on providing debt capital.

Fund-of-Funds (FoF): A fund that manages a portfolio of investments in other private equity funds.

Infrastructure: An investment strategy that invests in physical systems involved in the distribution of people,

goods, and resources.

Late-Stage VC: A venture capital strategy that provides funding to developed startups.

Multi-Stage VC: A venture capital strategy that provides funding to startups across many investment stages.

Secondary FoF: A fund that purchases existing stakes in private equity funds on the secondary market.

Seed/Early VC: A venture capital strategy that provides funding to early-stage startups.

VC/Growth: Includes all funds with a strategy of venture capital or growth equity.

Venture Capital: Venture Capital incudes any PM fund focused on any stages of venture capital investing, including seed, early-stage, mid-stage, and late-stage investments.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which is affecting markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot

be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of December 12, 2024