Smart Capital, Strategic Returns: The Case for Middle Market Private Equity

Key Points

Private equity middle market deals offer distinct advantages:

- Compelling risk/return profile: Companies with a total enterprise value (TEV) of $1–3 billion USD often maintain low leverage and offer multiple avenues for value creation, contributing to consistent performance across market cycles¹.

- Flexible liquidity options: Middle market investments provide fund managers with a broad range of exit strategies, enhancing overall fund flexibility.

- Robust, diversified deal flow: A high-volume middle market strategy reduces concentration risk and enables agile, opportunistic investing.

Private Equity Deal Size

| Size | Total Enterprise Value (TEV) | Characteristics |

| Mega/Large | $3-10 billion USD | Involves the largest companies and most established sponsors, often relying on strategic buyers or IPOs as exit paths. |

| Middle Market | $1-3 billion USD | Serves as a “sweet spot” for diversification, moderate risk, and upside potential. |

| Small | $1 billion USD | Associated with higher growth potential, but less scale and greater dispersion in performance. |

Source: Hamilton Lane Data, January 2025. Note: Other data providers use slightly different segment bands, such as a broader “middle market” up to $5 billion EV. This is Hamilton Lane’s standard.

Unlike public markets dominated by a few headline-grabbing tech giants, private equity is not shaped by a handful of outsized players. Private equity deals tend to be smaller than large-cap public stocks, but they span a broad spectrum of sizes. These deals are typically classified as small, middle, large, or mega, with each category offering its own unique opportunities, risks, and return profiles.

At Hamilton Lane, we believe deal size is a critical factor in shaping a fund’s risk, performance, and liquidity. While our fund portfolios span all market sizes, our primary focus is on the middle market: deals with TEV of $1–3 billion USD. We view this smaller middle market range as the “sweet spot” for balancing growth potential, stability, and diverse deal flow.

Here are the benefits of vetting deals with a focus on the middle market:

1. Attractive risk/return profile

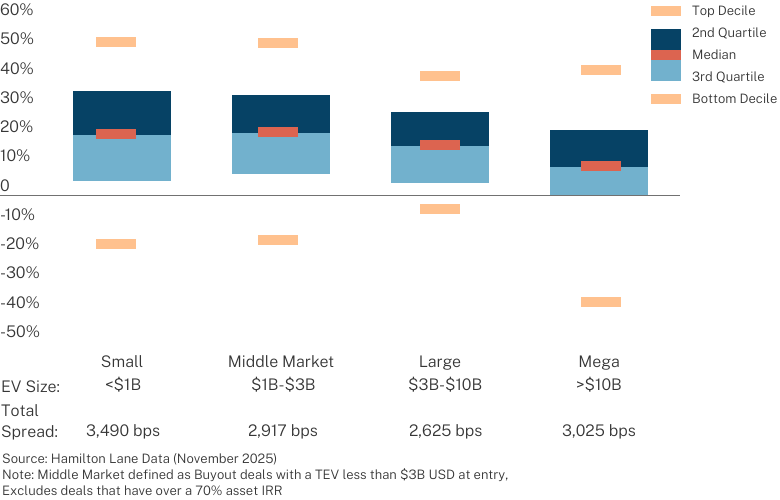

Historical data suggests that middle market private equity can demonstrate attractive performance characteristics relative to large and mega deals, with some top-quartile managers achieving notable upside potential and consistent performance across varying market cycles.

Deal Size and Performance

Buyout Spread of Gross IRR by EV

Deal Vintages: 2003-2024

Here’s what’s behind this attractive risk/return profile:

- Operational agility: Middle market companies are often more nimble than mega or large companies. As a result, they’re able to quickly implement strategic initiatives.

- Lower leverage: Middle market businesses typically favor balanced capital structures and organic growth, providing greater flexibility in uncertain markets.

- Varied growth levers: Middle market companies can drive expansion through product innovation, geographic reach, and operational efficiency.

2. Liquidity opportunities

“Is quarterly liquidity guaranteed?” It’s a common question, especially from investors new to private markets. Semi-liquid evergreen funds are built to offer regular access to capital, but this access is generally not guaranteed. Liquidity depends on both the fund’s design and the nature of its underlying assets—and middle market deals can play a key role in enhancing that liquidity2.

That’s because middle market investments give fund managers access to a wider range of exit options, not available to mega deals that often depend on IPOs and a limited number of strategic buyers. Potential exits in the middle market include a much larger set of strategic and financial buyers, including sales to larger GPs, yet these investments are still sizable enough to consider IPOs as well.

3. Diverse deal flow

The middle market encompasses a significantly larger universe of companies compared to the large-cap space. This allows fund managers to be selective in choosing deals. For example, Hamilton Lane sources deals from an active universe of over 500 general partners, creating a broad and dynamic deal funnel3. In contrast, mega or large platforms often focus on a smaller pool of proprietary, large-cap deals, which can limit opportunities and increase concentration risk.

The benefits of this diverse deal flow include:

- Robust portfolio diversification: High deal volume in the middle market allows fund managers to build portfolios diversified across sectors, geographies, and investment strategies, reducing reliance on any single market or trend.

- Reduced concentration risk: High deal volume in the middle market allows allocators to diversify across transactions, limiting exposure to any single deal—unlike large funds with fewer, high-stakes deals.

- Strategic and opportunistic investment approaches: Diverse deal flow allows allocators to pivot quickly to high-potential sectors or niches, offering flexibility that a large, highly-focused strategy cannot match.

The Hamilton Lane Approach

For over 30 years, Hamilton Lane has invested in the middle market. Our expansive multi-manager platform complements this focus, providing access and visibility across a wide range of opportunities. Over time, we’ve built deep expertise and strong relationships, enabling informed investment decisions and access to high-potential deals spanning sectors and geographies.

While many private markets firms claim to target middle market deals, few possess the capabilities or relationships required to access this segment effectively.

Hamilton Lane leverages its unique access to construct portfolios that are well-balanced, provide liquidity, and aim to deliver compelling risk-adjusted returns.

2JP Morgan Private Equity Insights, A big role for small and middle-market private equity investments, July 2024

3As of August 2025

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable, but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

Certain of the performance results included herein do not reflect the deduction of any applicable advisory or management fees, since it is not possible to allocate such fees accurately in a vintage year presentation or in a composite measured at different points in time. A client’s rate of return will be reduced by any applicable advisory or management fees, carried interest and any expenses incurred. Hamilton Lane’s fees are described in Part 2 of our Form ADV, a copy of which is available upon request.

Any tables, graphs or charts relating to past performance included in this presentation are intended only to illustrate the performance of the indices, composites, specific accounts or funds referred to for the historical periods shown. Such tables, graphs and charts are not intended to predict future performance and should not be used as the basis for an investment decision.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.