.webp?language=en-US)

Where Scale Meets Expertise

Leveraging our substantial primary capital deployment, we believe we are uniquely positioned to capitalize on the attractive long-term growth potential trends of the secondary market through a dedicated continuous evergreen investment vehicle. Supported by a team of 278 investment professionals,1 we aim to deliver topical market insights, robust execution capabilities and the flexibility to invest across all segments

Harnessing the power of secondaries for private wealth investors

- Liquidity: Focuses on funded assets with strong potential for near-term realizations

- Growth Potential: Targets high quality middle market buyout funds at inflection points in the investment life cycle

- Flexibility: Leverages Hamilton Lane’s strong competitive position with LPs and GPs to maintain a flexible approach across transaction types

- Optimized Return Potential: Seeks entry discounts combined with long-term value appreciation

Why invest in secondary investments?

Secondaries have historically generated attractive returns and low volatility versus other private markets strategies

- J-Curve mitigation.2 Investments are purchased farther along in their life cycle, with the potential to reduce the negative impact of management fees and accelerate the pace and timing of distributions.

- Instant diversification. Secondaries may provide investors with the ability to quickly diversify a portfolio by vintage years, investment strategies, industry sectors and fund managers.

- Knowledge of underlying assets. Secondary portfolio companies can be carefully analyzed, reducing the “blind pool” risk3 associated with primary investments.

- Increased pace of capital deployment. Investments are typically at or near the end of their investment periods when purchased.

- Embedded Value. Secondaries are usually sold at a discount to their primary market counterparts, potentially enhancing overall risk-adjusted returns.

Why now?

In recent years the secondary market has presented an opportunity set that is broader than ever before in terms of deal flow, creativity and transaction activity

- Record secondary volumes. Secondary volume has grown 18% annually from 2013 through 20244, with 2024 hitting a record level of volume and more secondary opportunities.

- Supply-demand imbalance. There currently isn’t enough secondary capital to support all the deal volume, thus potentially creating an attractive buyer dynamic5, which may change over time depending on market conditions and investor behavior.

- Potential appreciation. Secondary funds formerly had a reputation for offering quick returns from discounts. However, most returns from secondaries are now coming from go-forward appreciation.6

- Historical performance. Secondaries have historically generated competitive returns and liquidity for investors to date.7

*The share class performance prior to February 27, 2025 reflects the performance of HL PSF Holdings LLC and is not direct past performance of the subsequently formed Hamilton Lane Private Secondary Fund, which became effective on February 27, 2025. Performance is inclusive of annual distribution. Past performance is not a guarantee of future returns. Returns shown net of all fees and expenses. The prospectus contains this and other information about the Fund and is available at www.hamiltonlane.com/psfprospectus or by calling 888-882-8212. Read carefully before investing. Since Inception of HL PSF Holdings LLC is September 4, 2024. Class R shares are subject to a maximum front-end sales charge of 3.50%.

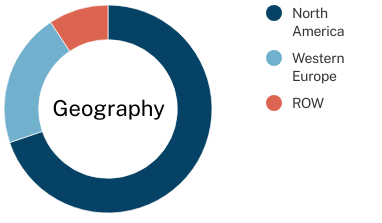

Target Portfolio Construction

For illustrative purposes only. Allocations subject to change without notice.

- Our investment approach targets a broad spectrum of secondary opportunities, from GP-led, structured transactions to the purchase of individual fund interests

- Flexible approach across transaction types given our strong competitive position in both the LP and GP markets

- Primarily focused on developed markets, with more weight towards North America

- Focus on hard to access, high quality mid market buyout funds where our relationship advantage is prioritized

Contact Us

For general inquiries, please reach us at 866-361-1720 or HLEvergreenOps_US@hamiltonlane.com..

2J-curve: A trendline that shows an initial loss immediately followed by a dramatic gain

3Blind pool risk refers” to the potential risks associated with investing in a blind pool investment vehicle where investors contribute funds without knowing the specific investments that will be made on their behalf. Most primary funds are blind-pool. In other words, the investors are “blind” to the specific assets in which their money will be invested. The main risk associated with blind pools is the lack of transparency and control. Since investors do not have detailed information about the specific investments, they are unable to assess the risk and potential returns associated with those investments.

4Source: Evercore FY 2024 Secondary Market Review (January 2025)

5Source: Hamilton Lane Diligence (January 2025)

6Hamilton Lane Data (August 2025)

7Source: Hamilton Lane Data via Cobalt (July 2025)

IMPORTANT RISK INFORMATION

Investors should carefully consider the investment objectives, risks, charges and expenses of the Hamilton Lane Private Secondary Fund before investing. The prospectus and, if available, the summary prospectus contain this and other information about the Fund. You may obtain a prospectus and, if available, a summary prospectus by downloading the prospectus or by calling 1 (888) 882-8212. Please read the prospectus carefully before investing.

The Fund operates as a continuously offered non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended.

Shares are speculative and illiquid securities involving substantial risk of loss. Shares are not listed on any securities exchange and it is not anticipated that a secondary market for Shares will develop. Shares are subject to substantial restrictions on transferability and resale and may not be transferred or resold except as permitted under the Agreement and Declaration of Trust. Although the Fund may offer to repurchase a limited amount of Shares from time to time, Shares will not be redeemable at a Shareholder’s option nor will they be exchangeable for Shares or shares of any other fund. As a result, an investor may not be able to sell or otherwise liquidate Shares. Shares are appropriate only for those investors who can tolerate a high degree of risk and do not require a liquid investment and for whom an investment in the Fund does not constitute a complete investment program. The Fund has no operating history. The Board may elect to repurchase less than the full amount that a Shareholder requests to be repurchased and may under certain circumstances elect to postpone, suspend or terminate an offer to repurchase Shares. An investment in the Fund is considered illiquid.

The Fund may engage in the use of leverage, derivative instruments, hedging, and other speculative investment practices that may accelerate losses.

An investment in the Fund is generally subject to market risk, including the loss of the entire principal amount invested. An investment in the Fund represents an indirect investment in the securities owned by the Fund. No guarantee or representation is made that the investment program of the Fund will be successful, that the various Private Equity Investments selected will produce positive returns, or that the Fund will achieve its investment objective.

Some of the principal risks of the Fund include, risks in investments in portfolio funds, taxation, failure to qualify as a regulated investment company, prepayment risk, inflation and interest risks, business and structure related risks, management related risks, closed-end fund, temporary investments, cybersecurity risk, and potential future conversion to an interval fund. For a complete description of the Fund’s principal investment risks, please refer to the prospectus.

The amount of distributions that the Fund may pay, if any, is uncertain. The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors.

Valuation of the Fund’s Interests in Portfolio Funds:

There is no established market for privately-held portfolio companies or for Secondary Investments, and there are not likely to be any comparable companies for which public market valuations exist. Purchasing interests at what may appear to be "undervalued" or "discounted" levels is no guarantee that these investments will generate attractive risk-adjusted returns to the Fund, and such investments may be subject to further reductions in value. No assurance can be given that investments can be acquired at favorable prices or that the market for such interests will continue to improve. In addition, the Fund's Incentive Fee structure could create an incentive to buy assets with steep discounts compared to their sponsor's valuation of such assets.

Non-Diversified Status Risk:

Although the Fund is allocated across sectors and asset classes, it is a non-diversified fund and subject to risks associated with concentrated investments in a specific industry or sector and therefore may be subject to greater volatility than a more diversified investment.

General Risks of Secondary Investments:

The overall performance of the Fund's Secondary Investments depends in large part on the acquisition price paid, which may be negotiated based on incomplete or imperfect information. Certain secondary investments may be purchased as a portfolio, and in such cases the Fund may not be able to exclude from such purchases those investments that the Adviser considers (for commercial, tax, legal or other reasons) less attractive. The secondary interests in which the Fund may invest are highly illiquid, long-term in nature and typically subject to significant restrictions on transfer, including a requirement for approval of the transfer by the general partner or the investment manager of the Portfolio Fund, and often rights of first refusal in favor of other investors.

Diversification does not guarantee a profit or protect against a loss in a declining market.

Distribution Services Inc, LLC is the distributor of the Hamilton Lane Private Secondary Fund. Hamilton Lane Advisors, LLC is the investment adviser to the Hamilton Lane Private Secondary Fund. Distribution Services Inc, LLC is not affiliated with Hamilton Lane Advisors, LLC. Learn more about Distribution Services Inc, LLC at FINRA's BrokerCheck.

HMLAN-4790875-09/25