What Are Secondaries?

Secondary investments represent the transfer of a private equity interest from one investor to another. Secondary buyers purchase an investor’s commitment to a fund and effectively become a replacement investor as a limited partner (LP).

The Anatomy of a Secondary Transaction

Primaries vs. Secondaries

A private equity primary fund commitment refers to an LP’s commitment of capital in a fund. This commitment provides the fund with the necessary capital to make investments in various companies.

In a private equity secondary fund commitment, a secondary buyer purchases a commitment to an existing private equity fund from the primary buyer or secondary seller — effectively becoming a replacement investor.

Secondary buyers gain immediate exposure to an existing, mature portfolio which may generate cash flow sooner than primary investments and which may help reduce risk by offering a diversified portfolio across various vintage years, industries, geographies or even general partners (GPs).

| Primary Fund Commitment | Secondary Fund Commitment |

|

|

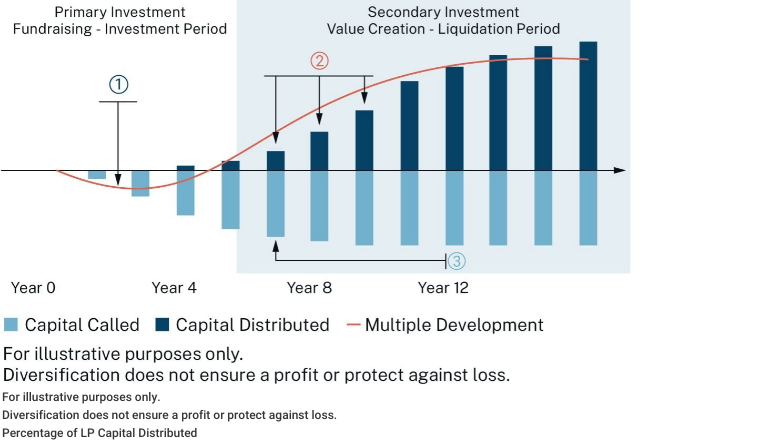

An Investor's Journey Across the J-Curve

A capital call, also known as a draw-down, is where the GP of a fund calls on LPs to supply a portion of the amount of capital that they committed at the beginning of the investment. The timing and amount are at the GP’s discretion and, once capital has been called, it is considered “paid-in capital.”

A capital distribution is cash (or securities) paid to an investor when the fund managers realize their investments in underlying companies. In the above graph, the capital distributed (starting in year four) shows the amount of cash or securities paid to investors. As the fund continues to perform, capital distributions tend to increase.

Quantifying the Benefits of Secondaries

Portfolio Benefits

For investors looking to optimize their portfolio strategy, secondaries may be attractive for several reasons.

| J-Curve Mitigation | Portfolio/Vintage Diversification | Risk Reduction From Knowledge of Underlying Assets |

| Investments are purchased farther along in their life cycle, with the potential to reduce the negative impact of management fees and accelerating the pace and timing of distributions. | Secondaries may provide investors with the ability to quickly diversify a portfolio by vintage year, investment strategy. industry sector and fund manager. | When evaluating a secondary transaction, the portfolio companies can be carefully analyzed, reducing the "blind pool" risk associated with primary investments. |

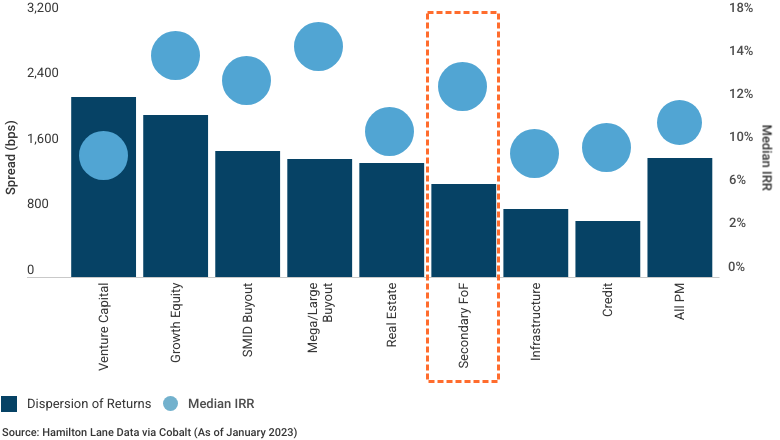

Secondary Resilience & Risk-Adjusted Returns

Secondaries have historically generated attractive returns and low volatility versus other private market strategies. They have the ability to benefit from growth while capitalizing on wider discounts in volatile or distressed markets.

Dispersion Returns by Strategy

Vintage Years: 1979-2018, Ordered by Spread of Returns

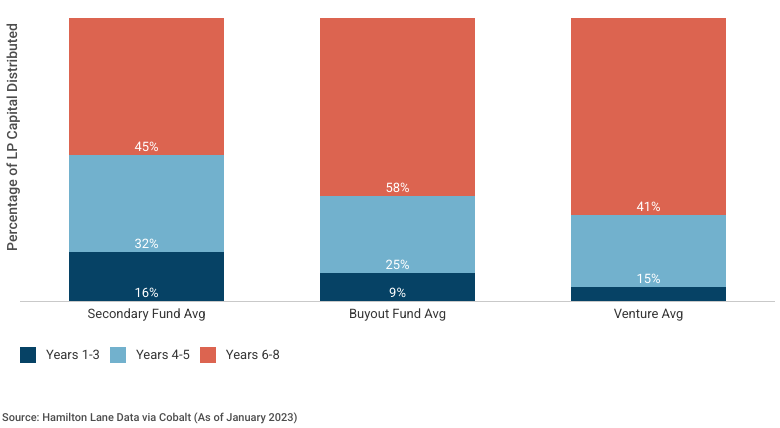

Capital Is Distributed Earlier

Secondary funds tend to hold more mature investments than traditional private equity funds. Since private equity investments typically exhibit negative returns in the initial years due to management fees and other expenses, secondaries help investors avoid this stage of the private equity life cycle. And, because secondary funds usually come later in the investment cycle, distributions from exits may be sooner than primary funds.

Percentage of LP Capital Distributed

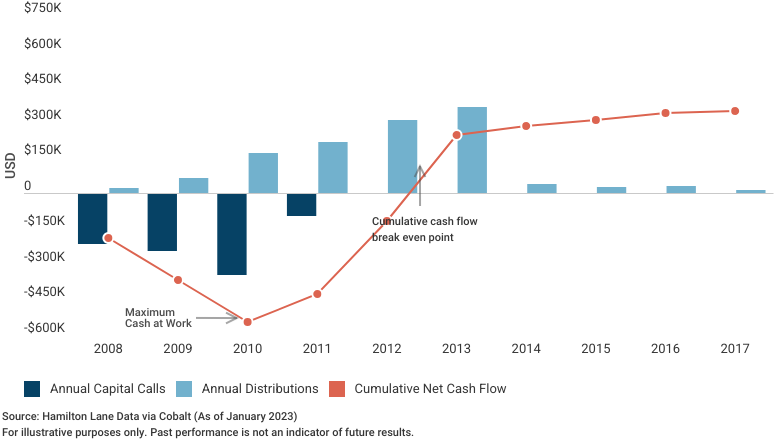

Hamilton Lane Case Study

Life Cycle of a Secondary Fund

The following scenario illustrates a $1M commitment to Hamilton Lane’s 2008 vintage Secondary Fund (HLSF II).

Expected Cash Experience for Investors

- Investors’ capital may be called down periodically during the investment period and should expect to have 80-90% of their commitment invested by years 3-4.

- The value of investors’ capital should grow over time and that value will be sent back to investors in the form of distributions, also known as realizations.

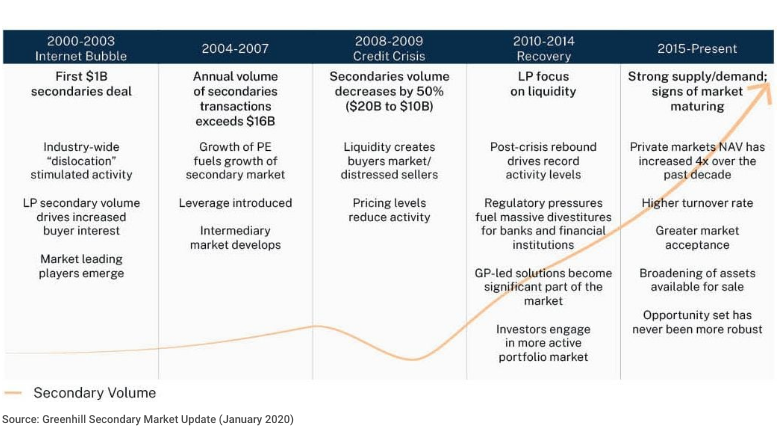

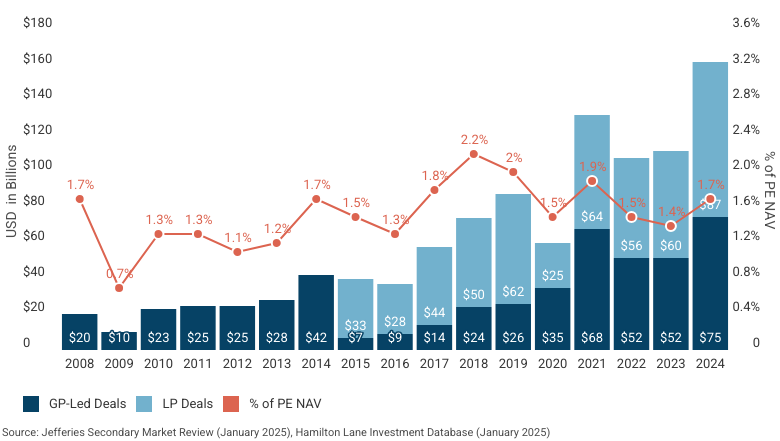

Secondary Market Overview

Secondary Market Evolution

Initially a niche strategy, secondary investments have become mainstream.

Secondary Market Volume by Deal Type

The secondary turnover ratio has consistently ranged from 1.0% - 2.0% for more than a decade

Transaction Landscape

| LP Deals | GP Deals | |

| Market Dynamics |

|

|

| Supply Catalysts |

|

|

| Key Takeaways |

|

|

Why Do Limited Partners Sell in the Secondary Market?

| Liquidity | Allocation Issues | Portfolio Management |

|

|

|

*Source: Greenhill Secondary Market Update (January 2020)

Hamilton Lane Case Study

In this case study, you can see how Hamilton Lane manages relationships to execute deals and provide downside cushion through the strategic use of secondaries.

Background

- An LP wanted to sell a mature investment totaling $15.8M. In secondary transactions, pricing is expressed as a percentage of recent net asset value (NAV).

- The LP restricted the offer to secondary investors with strong primary relationships with the GP, which limited competition among buyers.

Transaction

- Hamilton Lane’s GP relationship allowed us to purchase, as the secondary buyer, the fund position from the LP, or secondary seller.

- Secondaries are often purchased at a discount to NAV, in this case 24%. This discount allowed us to buy $13M in NAV at $9.9M.

Hamilton Lane’s Position

- We received an immediate return of $3.1M, which also provided downside cushion.

- Hamilton Lane will fund all future capital calls and receive future distributions.

This document has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this document are requested to maintain the confidentiality of the information contained herein. This document may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this

presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent

public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or

any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Secondary Funds Strategy: Access Private Markets Liquidity

Discover how secondary buyers can gain immediate exposure to an existing, mature portfolio to potentially generate cash flow sooner than primary funds.