Executive Summary

- Policy shifts, tariffs and deregulation are influencing the investment landscape for investors, but don’t let them become a distraction.

- Private market-based solutions incorporating technology, innovation and information access are the true drivers of value creation, change and impactful solutions.

- Software, AI and companies leveraging new digital technology and regional, small-to-mid-sized businesses can capitalize on this disruption.

- Investors with strategic allocations to these companies seeking smarter, faster and more efficient solutions to today’s challenges have the potential to thrive and generate outsized returns within their portfolios while creating meaningful impact.

The changing political and economic landscape has everyone’s head spinning. But how much of this is really impacting private markets investments and their direction of travel? Recent U.S. policy shifts, including the One Big Beautiful Bill Act (OBBBA), Inflation Reduction Act (IRA) rollbacks and continually evolving tariffs, have consumed a fair amount of market attention and indigestion. However, tech-driven innovation and decreases in regulation have also unlocked significant investment opportunities.

After a brief capital markets reset in 1H 2025, reduced regulatory overhang is beginning to open access to projects with strong commercial fundamentals and resilient business models. In some areas, these changes are causing a reassessment of those businesses reliant on transient policy support, which can fluctuate in the short-to-medium term. As the existing investment landscape continues to shift, we believe the next cycle of impact innovation and value creation is rich with opportunities across disruptive software tools, tech-enabled industrials, energy services and regional, small-to-mid-sized (SMID) growth companies.

These innovation- and tech-driven opportunities are creating a new wave of impact opportunities in the cycle ahead that we need to adapt and embrace. As lyrical prophet Bob Dylan said:

Your old Road is rapidly agin'

Please get out of the new one

If you can't lend a hand

For the times they are a -changin'.

AI, data centers and digital platforms at the heart of tech innovation

Today, technology advances and AI go hand in hand. These initiatives are driving the next era of growth, efficiency, resilience and productivity – the outcome of which can propel significant economic and social impact across regional communities and on investors' portfolios. Rapid advances in AI and the proliferation of data across industries continue to increase energy demands, while rewiring the competitive landscape and increasing investment efficiency. This is happening across the industrial landscape as companies seek faster, cheaper and more efficient methods of doing business and solving problems.

We believe that companies leveraging AI, data and analytics in new and unique ways to deliver positive economic and social outcomes are well-positioned to benefit from this growth over the next decade. And companies across sectors do too. Recent forecasts show AI adoption becoming increasingly critical to business sectors, including IT, supply chain and manufacturing, marketing, sales, finance, product development and HR. AI allows businesses to track the benefits that they deliver to customers more effectively. In impact investing parlance, we think of this as tracking the KPIs that demonstrate how a business is addressing an environmental or social challenge – from reducing energy use in buildings to using software tools that provide patients with better access to healthcare solutions. These KPIs can demonstrate how and where businesses bring the most value to their customer base and spur growth.

The AI revolution is delivering market-driven impact solutions that are truly next generation concepts. Recently, we visited the European production plant developing a humanoid robot that uses AI to learn basic tasks in the home that can help with household chores and even caring for the elderly or people with disabilities. This company expects to support household customers and create new opportunities for human productivity with multiple applications of this type of safe, low-cost robotic labor in the years ahead.

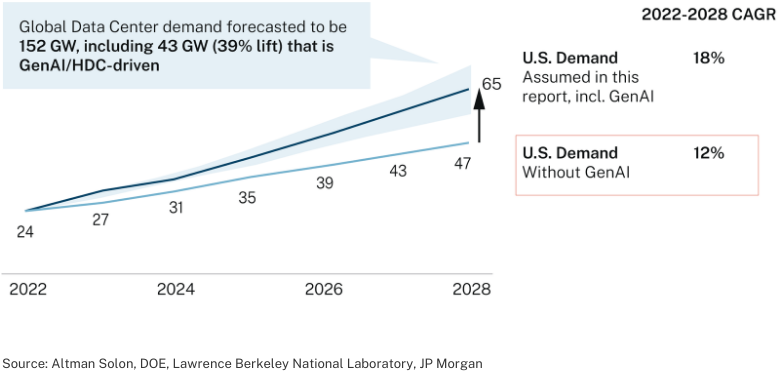

AI demands more power

U.S. Data Center Demand Forecast

2022-2028 CAGR

The increasing computing power requirements from the rapid proliferation of AI are driving more capital towards supporting data center expansion, which requires an efficient and cost-effective approach to energy generation. Distributed computing will drive energy consumption higher over the coming years, and the ability to meet this demand (or not) will separate the winners from the losers. Companies leveraging emerging and disruptive technologies to address these needs can stand out from the competition and deliver impactful outcomes. SaaS platforms and other digital innovations that streamline project structuring can help private companies adapt and win.

AI, data center and digital platform disruption are already changing pricing models and cost structures across industries, shifting the competitive balance and putting pressure on companies with fixed costs that may not be able to adapt in time. With the AI revolution moving towards us like a freight train, active portfolio management matters more than ever.

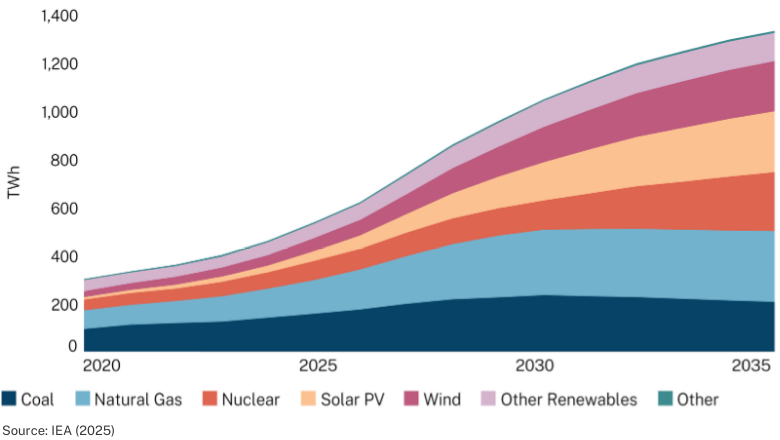

Energy growth, diversification and transition

With the AI locomotive gathering the need for more steam, projections for U.S. and global energy demand also show sustained growth across all major power sources. Critically, renewable energy generation is forecasted to increase market share in the long term, propelled by lower costs and more efficient technology, while natural gas will remain crucial for system reliability and peak capacity in the medium-term. The speed to market and lower cost curves allow some renewable energy sources like solar to deliver generation advantages and much-needed power to the grid. This is one reason that in the first three quarters of 2024, 90% of new power generation in the U.S came from renewables, with solar contributing over 70% of this new electricity.1

Sources of global electricity generation for data centers

Base Case 2020-2035

In addition to these growth-oriented real assets supporting high-demand needs, industrial companies like energy infrastructure services can provide economic and social benefits to both local communities and investors alike. Investors who are coming off the sidelines in search of the most compelling opportunities in 2025 and beyond can take advantage of these energy trends. In our view, these are some of the most attractive investments on a risk/return basis and represent the “picks and shovels” approach to investing in infrastructure. We see businesses ranging from software tools and engineering services to landscaping and construction companies all playing a role in developing and benefiting from these trends.

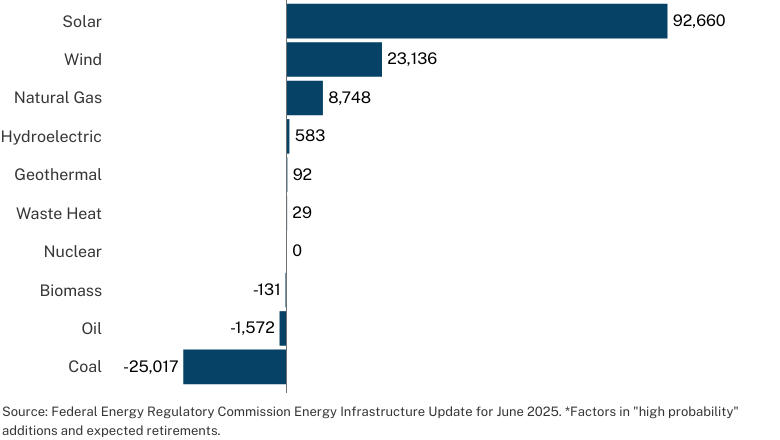

Net new U.S. electricity generation capacity

(July 2025-July 2028)*

Renewable energy sources and services are needed to support this continuously evolving market. More recently, tighter lending conditions, increased policy risk and slower permitting have created volatility and delayed wind development in the U.S. and have changed supply chain calculations across the solar marketplace. However, the cost curve for utility-scale solar continues to drop and estimates show that solar will generate the vast majority of new U.S. electricity by 2028, making it one of the fastest and most cost-effective deployment options to meet spiking energy demands today. Other renewable energy sources such as nuclear and geothermal energy are receiving significant investor attention and will add a diversified load of low-emission sources to help meet the demand.

As we consider where to lean in to support this increased energy demand, we believe renewables will continue to play an important role, but it's important to assess these market opportunities carefully to avoid unneeded regulatory risk.

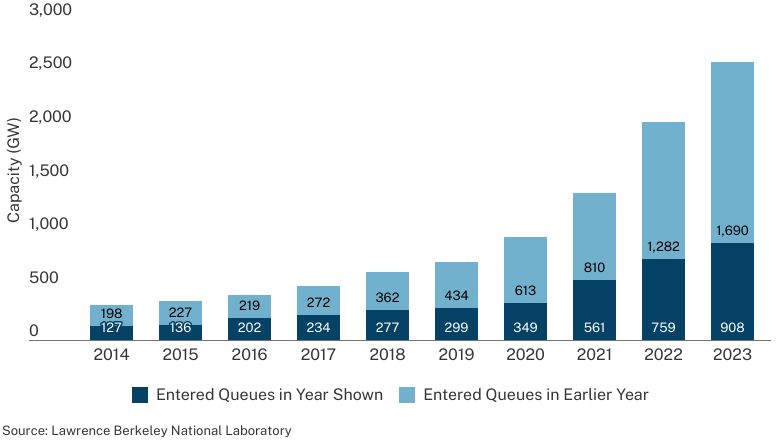

Interconnection Queues

By Capacity (GW)

Finally, all this energy demand change, transition and transformation is putting added stress on the existing grid. The rise in queued projects for grid connection underscores the importance of investing in transmission, storage and flexible supply solutions. While many investors may immediately turn towards their infrastructure portfolio to act on this change, the operating companies that are already deploying new technologies and sophisticated analytics solutions to improve interconnection efficiency can capitalize on this moment – all with an equity-like return. We believe there is room to run, and that many of the most effective energy solutions will manifest through new AI, SaaS and digital platforms that help manage these complexities.

It would be a mistake to underestimate the growth in renewable and low-emission energy sources ahead. Most forecasts continue to project that fossil fuels will see their market share decrease over time. Importantly, the transition to cleaner energy is not linear. A mix of renewable, natural gas, nuclear and other emerging technologies will be required to satisfy growing energy demand and ensure resilience. We believe investments that efficiently manage decentralized energy sources to support greater grid demand will increasingly become more attractive to long-term investors, as well as governments seeking energy independence and the regional communities they support.

Regionalization and the role of SMIDs

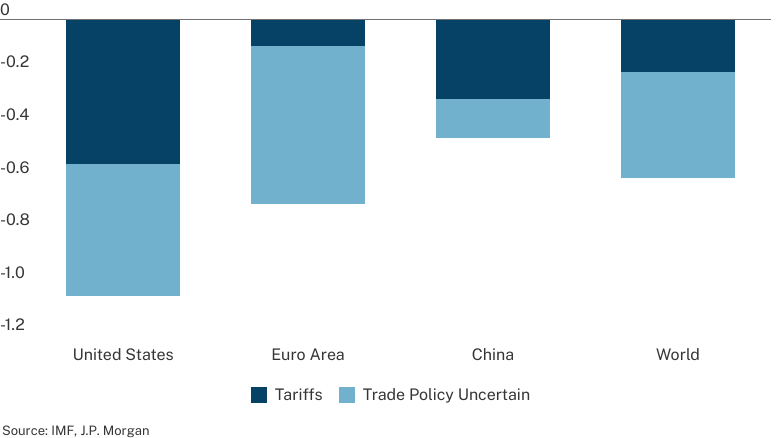

Tarrifs and trade policy uncertainty could weigh on both U.S. and global GDP

%-pt change in GDP through 2026

Shifting geopolitical relations and continually evolving tariffs have upended the global supply chain, but it's not all bad news. Smaller, more nimble private companies that maintain an emphasis on domestic, rather than global supply chains can drive innovation in the marketplace. We believe that today's disruption is already creating attractive investment opportunities, specifically for companies with robust U.S.-based manufacturing, regional supply chains and mission-critical services supporting vital industries like energy and healthcare. Why?

The globalization trend of the past 25 years is reversing. Increasingly, regionally focused SMID businesses are gaining a relative advantage over those in the large/mega end of the market. Their ability to move quickly, navigate local environments, efficiently manage risk and effectively maintain domestic supply chains is becoming a distinct edge and helping to insulate them against global market shocks.

Turning disruption into opportunity

Looking forward, breakthrough technologies, demand shifts and efficiency gains will drive market-based solutions and impactful outcomes more decisively and sustainably than government policy. The economic trends driving energy demand, lowering cost curves and enabling efficiency will continue. They are unstoppable and will render today’s 15% tariffs and many of the OBBBA policy shifts as yesterday's news.

With such significant market change, seeking out investment partners with strong balance sheets, deal flow and the resources to assess and manage the disruptions ahead can help investors adapt and thrive to this new landscape. Among these key partner resources are the right data sets and the ability to harness them with the right technology to make the most informed decisions. Investors who are prepared to leverage data-driven diligence, technical expertise and operational flexibility stand to capture long-term outperformance.

The technology changes underway today have moved us into a new era and accelerated the growth curve, whether we like it or not. This creates multiple paths for impact innovation and opportunities for smaller, high-growth private companies to deliver critical solutions that customers and societies around the world are seeking. We all need to be thinking about the changes coming ahead, not ruminating on the winners, losers or the political labels of the last decade.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which is affecting markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot

be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of December 12, 2024