The Rise of Opportunistic Credit

As even a casual observer of financial news is now well aware, the last decade plus has seen an explosion of fundraising within the private credit asset class. And while much of the current media and investor attention has been focused on the relatively easy-to-define direct lending space, adjacent to this segment is a more ambiguously defined strategy: opportunistic credit.

In the broadest sense, opportunistic credit pursues deals or securities outside the traditional “boxes” of direct lending and private equity, with a focus on capturing enhanced returns while still offering downside protection. While opportunistic strategies can focus on performing “special situations,” or distressed assets, for the purposes of this discussion we’ll focus on the performing sector. Securities within this strategy can range from cash-pay debt (senior or junior) to PIK-only structures (Holdco PIK), as well as preferred equity securities that may provide equity participation upside. As the name suggests, these opportunistic credit investments retain structural characteristics of their senior credit cousins (senior to equity, typically with some portion of contractual return), albeit at higher returns to compensate for typically more subordinated positions.

In the same way these opportunistic securities can vary in structure, so can a manager’s approach to investing in this strategy. Some GPs will focus exclusively on a specific security, such as junior debt, while others may focus more broadly on any security between senior debt and common equity. Increasingly managers are also expanding beyond purely corporate lending structures as well, incorporating credit strategies with similar return profiles, such as asset-backed finance and credit secondaries, under their opportunistic umbrella. These broader strategies emphasize a flexible all-weather approach, allowing managers to dynamically allocate toward attractive risk/return opportunities, with less restriction on underlying security type.

A strategic window for opportunistic credit

Private markets investors are facing a return conundrum. Direct lending yields have tightened due to spread compression and falling SOFR. Equity return expectations have also come under pressure as longer hold periods, elevated borrowing costs and higher equity contribution requirements weigh on returns.

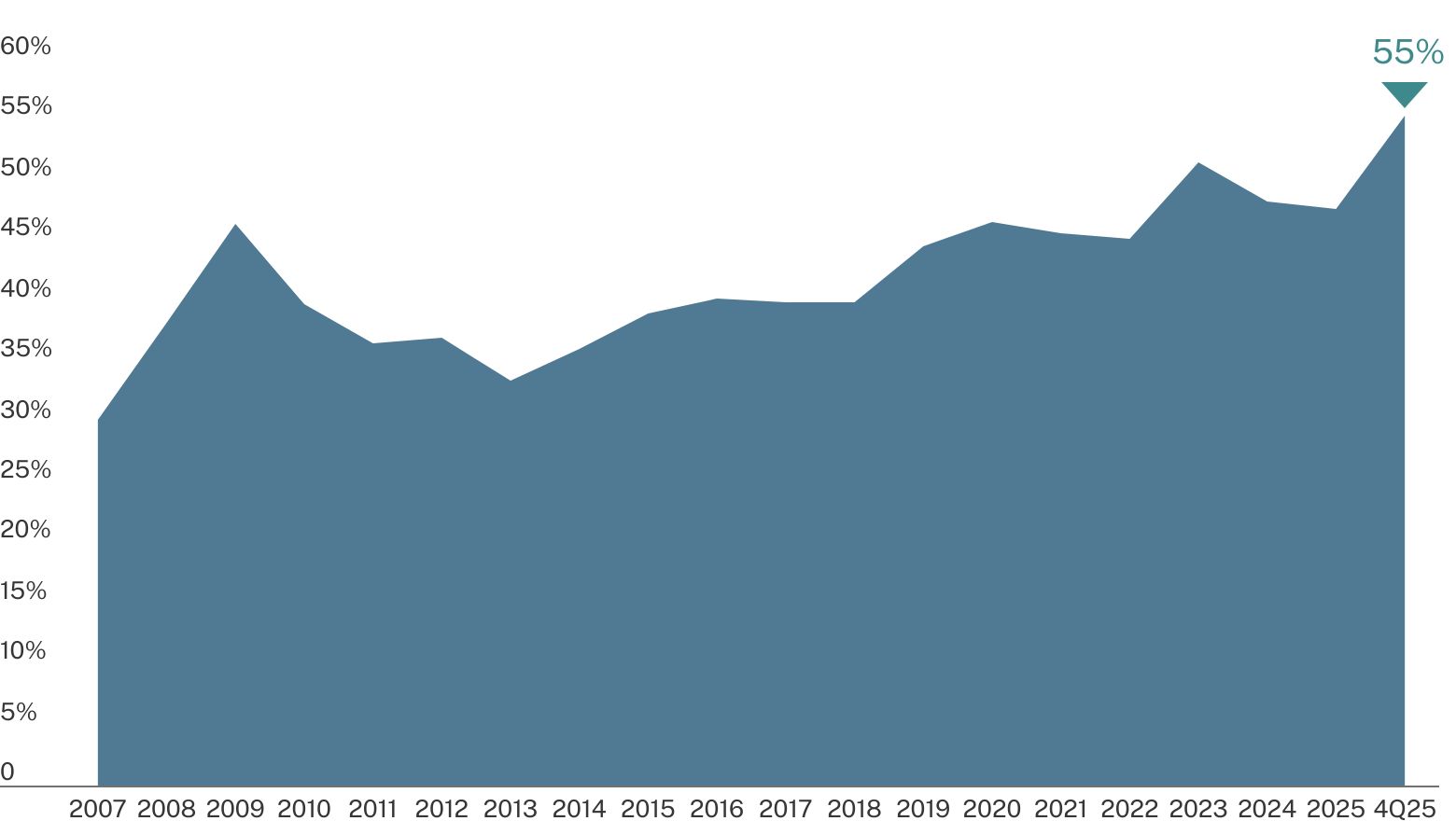

Equity contributions for US LBOs

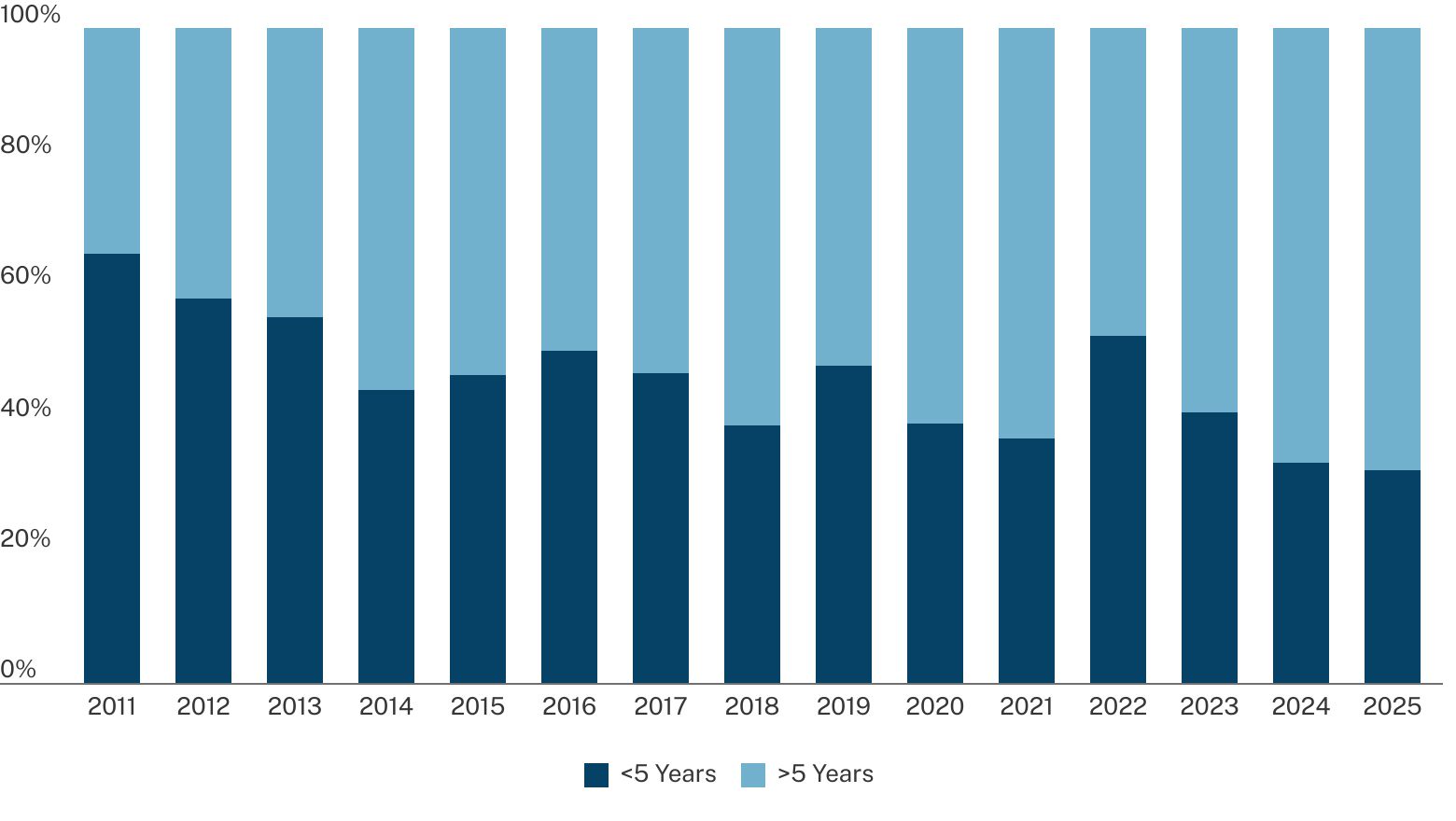

Buyout hold periods for exited deals

Opportunistic credit may help investors solve this problem. Positioned between direct lending and equity, opportunistic credit seeks to deliver equity-like return potential with structural features that may provide downside mitigation. Investors are drawn to the strategy for a few key reasons:

- Contractual returns with upside return potential

- Typically shorter duration than private equity due to contractual maturities

- Structural protections and equity subordination

- Flexible investment approach enables a focus on the most attractive opportunities in evolving markets

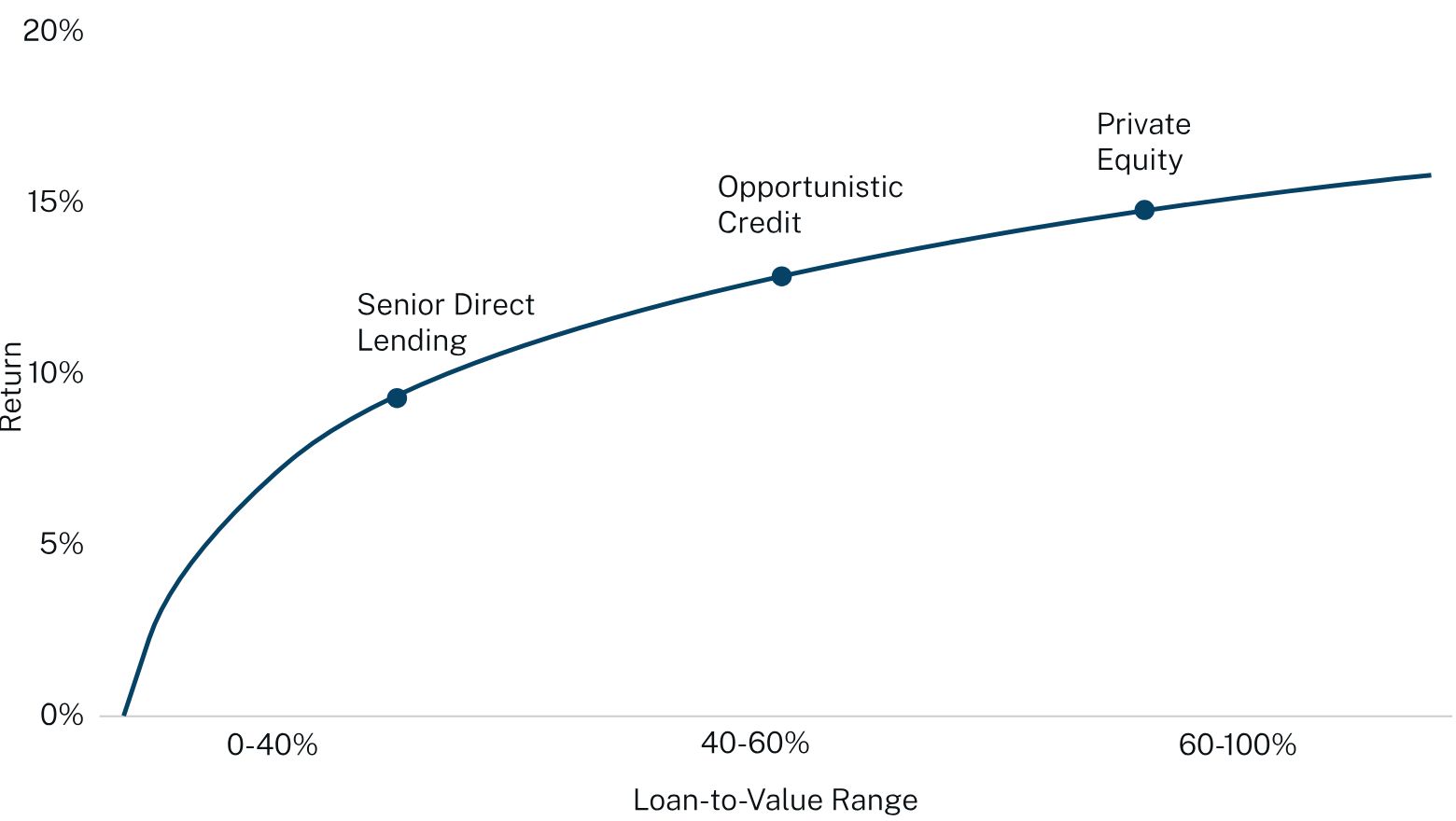

Risk-Return Spectrum Across Private Credit and Private Equity

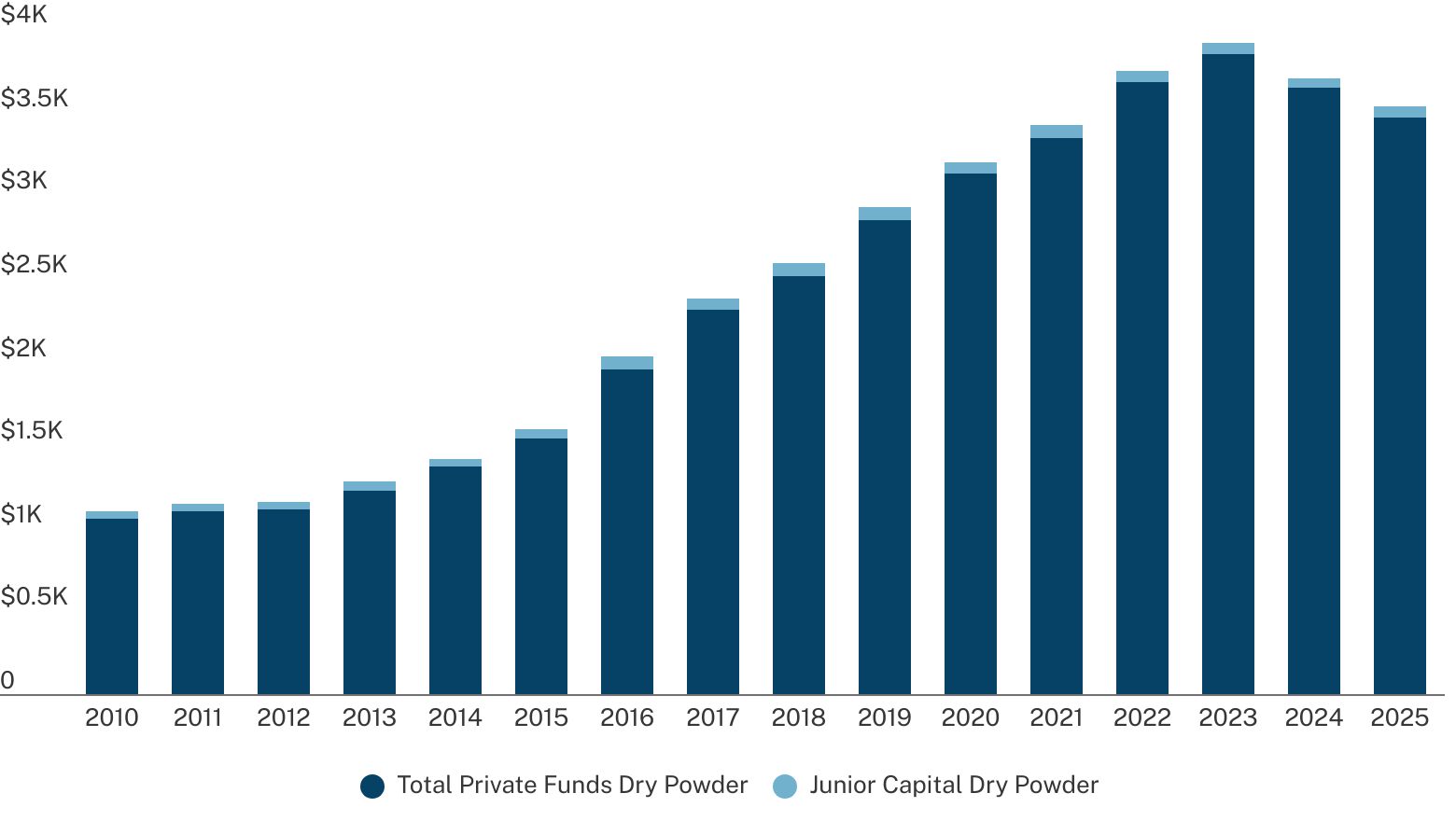

Junior capital represents only 1.5% of total private markets dry powder today

A key driver of the current opportunity is the relative undersupply of flexible capital in the private markets.

Despite continued growth in private markets dry powder, junior capital — or flexible capital — dry powder has remained relatively low at 1.5%, even as a growing need has emerged, fueled by a few key market factors.

First, the industry is facing a large and growing maturity wall of loans, many of which were issued in a low interest rate environment. Over $1.5 trillion of leveraged loans are maturing in the U.S. over the next eight years. Flexible capital solutions will become increasingly important in refinancing these loans where senior direct lending alone will be unable to.

U.S. Leveraged Loan Maturities by Year

Second, a sluggish M&A environment and increasing LP demand for liquidity are driving the need for more flexible capital solutions, including structured capital for minority recapitalizations and dividends. Over the past four years, private equity distributions have been well below both the PE and total private markets average.

Distributions

By Asset Class

Finally, availability of bank-led capital for junior or flexible solutions is limited, creating ample runway for private credit. Senior debt is estimated to account for up to 95% of the leveraged loan market, where banks tend to focus.

Integrating opportunistic credit into portfolios

Opportunistic credit is an all-weather strategy that bridges the gap between direct lending and private equity. It has historically outperformed traditional fixed income and direct lending, while offering lower volatility and better downside protection than private equity for a comparable return.

Within investor portfolios, private credit remains a newer allocation relative to fixed income. And while many sophisticated allocators have dedicated room for direct lending, fewer have expanded credit allocation to adjacent strategies like opportunistic credit.

Opportunistic credit exposure can complement direct lending by delivering enhanced multiple on invested capital (MOIC). Historical data shows that opportunistic credit has delivered approximately 15% and 22% higher MOIC than senior direct lending over five- and 10-year periods, respectively, based on average top-half performance for both strategies.* Blending exposure to these strategies can help enhance overall return potential. As a form of flexible capital, opportunistic strategies can pivot to take advantage of the best risk-adjusted opportunities versus being confined to a single focus. This flexibility can lead to greater diversification and lower correlation due to opportunistic credit’s ability to lean into areas such as asset-backed finance with collateral support.

Unlocking value in today’s market environment

With direct lending yields tightening and private equity return expectations under pressure, opportunistic credit offers investors a timely way to pursue equity-like returns with credit downside protection. That opportunity is strengthened by scarce flexible capital and growing demand for structured solutions driven by refinancing needs, slower M&A activity and LP liquidity demands. For portfolios anchored in direct lending, opportunistic credit can complement that exposure with the potential for enhanced MOIC, diversification, and offer differentiated risk-return characteristics, depending on market conditions, based on its flexible nature.

*Based on Hamilton Lane data as of June 2026. Figures reflect aggregated fund performance and include higher-performing cohorts, which are not representative of all results. Performance varies by vintage year, manager, and market conditions, and results for other funds may be materially lower. Past performance is not indicative of future results.

Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.

Credit: This strategy focuses on providing debt capital.

Growth Equity: Any PM fund that focuses on providing growth capital through an equity investment.

Mega/Large Buyout: Any buyout fund larger than a certain fund size that depends on the vintage year.

Private Equity: A broad term used to describe any fund that offers equity capital to private companies.

SMID Buyout: Any buyout fund smaller than a certain fund size, dependent on vintage year.

Venture Capital: Venture Capital includes any PM fund focused on any stages of venture capital investing, including seed, early-stage, mid-stage, and late-stage investments.

Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates.