2026 Credit Focus: Keeping Calm and Carrying On

Executive Summary:

- Private credit remains resilient despite geopolitical risk, AI disruption and late‑cycle uncertainty, with stress largely idiosyncratic and defaults contained.

- Volatility is creating opportunity. Wider spreads, higher‑for‑longer rates and bank retrenchment are improving pricing and terms for disciplined lenders.

- Selectivity matters more than ever. Strong underwriting, lower leverage and durable cash flows will be key to delivering income and downside protection.

A world on edge: The start of 2026

It’s safe to say there has been an increasingly critical eye on private credit in recent months. We entered 2026 still grappling with lingering market anxiety from 2025 fueled by headlines related to a series of high-profile bankruptcies and building redemption queues for select private credit vehicles. It seemed this backdrop was being used to manufacture the dawn of a credit crisis driven by late-cycle excesses. The chatter grew louder, but the assumptions were off: Headline issues were company-specific, not systemic.

February 2026 marked two developments with meaningful market implications. First, the USS Gerald R. Ford was deployed to the Middle East where a strike on Iran followed. Subsequently, the stock market dipped and the price of oil and gas rose, triggering fears of renewed inflation and damping the prospect for interest rate cuts.

For private credit, the implications are twofold:

- First, volatility may nudge investors to safety, benefitting senior direct lending. It may also instigate a yield premium, and we are already seeing spreads in private credit in the S+500 context once again, up from the mid-400 bps level prior to the strike on Iran.1

- Second, sustained inflation may stunt interest rate cuts, supporting investor yield.

The second significant event was Anthropic’s announcement of its Claude AI agents, which triggered a widespread sell-off of traditional software stocks amid concerns about disruption to enterprise software models. Stocks with significant private credit holdings were also victims of concerns that software disruption would lead to increased redemptions and defaults. Our view is that the software risk is overstated; however, it is not something to be ignored.

While the impact of AI on software has yet to materialize in the form of bankruptcies, there will inevitably be winners and losers. Outcomes are likely to be company-specific versus sector-wide. Cash flow-based lenders focused on deeply entrenched, mission-critical offerings with long-term contracts and lower loan-to-values will be better positioned. Customer churn will be something to pay close attention to as well as seat-based models in evaluating the continued health of software investments.

On the other hand, general software models are at risk. Agentic AI is transforming the landscape from user-driven applications to autonomous, goal-oriented systems. This disruption will also create opportunities. Valuations are resetting, and knowledgeable software-focused lenders are likely to obtain more lender-friendly terms. Access to leverage, though, could tighten. In early March, we saw JP Morgan announce it was tightening advance rates to non-bank lenders, particularly in relation to software. It will be interesting to see if others follow or use this as an opportunity to lean in.

Looking ahead: Areas of focus

War: The duration and intensity of the war in Iran is likely to determine the impact on the U.S. economy, which until now, has been performing. A prolonged conflict threatens to drive up consumer prices and slow growth. Oil and gas prices are at the heart of this as approximately one-fifth of global supply flows through the Strait of Hormuz. Elevated prices at the pump and increased transportation costs will put upward pressure on consumer prices. Higher inflation and slower growth will place pressure on both sides of the Fed’s dual mandate to maximize employment and minimize inflation. With the Fed already focused on inflation, war is less likely to nudge the Fed to cut rates, supporting a higher-for-longer rate environment. Private credit spreads are also likely to remain wider if the conflict endures, and this should benefit yields.

The consumer: The U.S. unemployment rate rose to 4.4% in February, up from 4.3% in January.2 While the unemployment level remains within a healthy range, a softening labor market can pressure consumer spending and threaten company EBITDA, which could ultimately influence default activity. As of February, the Morningstar LSTA U.S. Leveraged Loan Index payment default rate (trailing 12-month) by issuer count was 1.36%, well inside the long-term average.3 Despite calls for elevated defaults following the Fed rate hike cycle, which began in 2022, defaults have remained muted. While our base-case outlook does not anticipate broadly elevated defaults, our expectation is that those credits that do experience stress are more likely to do so because of structural issues such as leverage, heavy PIK usage and disruption.

Semi-liquid structures: Private credit is being tested, perhaps unfairly. Redemption requests for semi-liquid credit structures, particularly for some of the larger managers, have, in recent periods, exceeded the typical 5% quarterly limit. General Partners (GPs) are each behaving differently. Some have put up gates while others are stretching beyond their quarterly limits to provide liquidity. GP actions during this period will set precedents, which will influence investor confidence in these structures and their ability to deliver partial liquidity. Make no mistake, evergreen private credit structures are here to stay. As of 2024, total private credit AUM was over $500 billion, most of which was raised in the prior five years. Some believe closed-end structures may disappear in favor of evergreen structures in the not-too-distant future. Regardless, redemption requests will be something to pay attention to this year.

Defaults: Software disruption ultimately points to credit defaults. One bank recently forecasted that draconian case defaults could reach as high as 14-15% in a software disruption scenario. Others have pointed to 8% as their downside case. This dispersion highlights the uncertainty surrounding potential software disruption. If we look at where defaults in the leveraged loan market sit today, as of February 2026, the LTM default rate by issuer count was 1.36%, which remains inside of the 10-, 20-, and 25-year averages of 1.71%, 1.95% and 2.24%, respectively.4 When accounting for distressed exchanges, the LTM February 2026 default rate was 3.54%, down from an average of 4.24% in 2025 and 4.30% in 2024, another healthy trend line.5 However, one metric that did not shift in a favorable direction was the distressed ratio, which is an indicator of future default activity. After hovering in the 4-5% context for much of 2025, the distressed ratio gradually increased in the fourth quarter of 2025 and reached 8.89% in February of 2026.6 While this ratio is in line with peak months since interest rates started rising in 2022, it is a trend line worth keeping an eye on.

An unbroken strategy: Why should this time be any different?

For nearly 25 years, private credit has demonstrated positive performance in every vintage year and benchmark outperformance in every vintage year. It’s worth noting that over this period, the market experienced three recessions and two notable periods of sector-specific dislocation related to telecom in 2001 and energy in 2016. Despite some of the signal distortion in private credit, the strategy has remained undeniably consistent over long periods.

Private Credit IRR vs. PME

.webp?language=en-US)

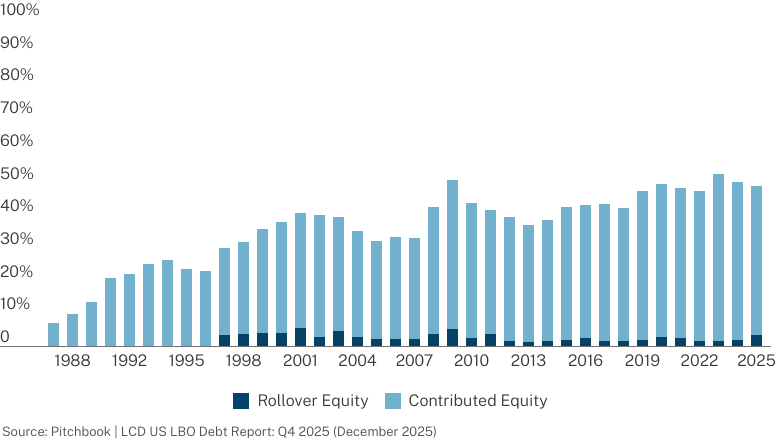

There is also something structurally different in today’s environment relative to pre-GFC era financing. Equity contributions as a percentage of total capitalization are higher today versus the period leading up to the GFC. Equity contributions in leveraged buyouts in 2007 were around 33% versus 49% in 2025, so as purchase price multiples have increased, leverage levels have not followed.7 This supports the view that credit may be structurally safer today than in prior cycles.

Equity Contribution in Leveraged Buyouts

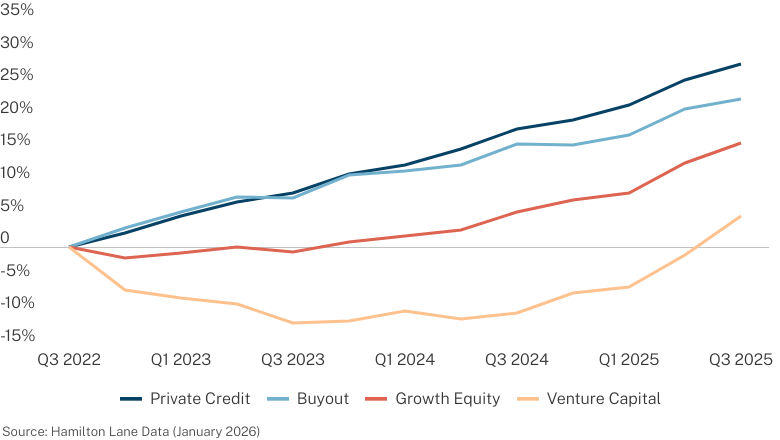

Relative performance for credit has also been strong, particularly on a 3-year cumulative basis when compared to other private markets strategies. Cumulative performance for credit has outperformed other equity-oriented strategies. Some of the challenges equity returns have faced relate to elevated borrowing costs and a challenging exit environment extending hold periods.

3-Year Cumulative Return

Cumulative Time-Weighted Returns Q3 2022 - Q3 2025

Periods of volatility often present compelling opportunities for private credit. Banks tend to retrench, making way for better pricing and structure for private credit lenders. While the broadly syndicated markets are holding up outside of technology-related sectors, the tone has shifted to more ‘risk-off’ following the strikes on Iran. Yields have widened in the BSL market and as noted earlier, we are seeing private credit spreads in the 500 context again, which will be yield-enhancing. Investors also tend to rotate into safer assets during periods of volatility and private credit is able to offer them downside protection and yield.

For investors, the data continues to support maintaining a dedicated allocation to private credit, particularly for those seeking income and downside protection through cycles. Volatility and mixed macro signals can be unsettling, but they are precisely the moments when a disciplined, long-term approach to the asset class has historically been rewarded. For private credit investors wondering what to do now: Stay the course; keep calm and carry on.

1,3,5,6PitchBook | LCD, US Leveraged Loan & Private Credit Market Commentary (March 2026)

2U.S. Bureau of Labor Statistics (February 2026)

4PitchBook | LCD, Monthly Default Report (February 2026)

7Federal Reserve Board (May 2025)

Strategy Definitions

Corporate Finance/Buyout – Any PM fund that generally takes control position by buying a company

Credit – This strategy focuses on providing debt capital.

Growth Equity – Any PM fund that focuses on providing growth capital through an equity investment.

Venture Capital – Venture Capital incudes any PM fund focused on financing startups, early-stage, late stage, and emerging companies or a combination of multiple investment stages of startups.

Index Definitions

S&P UBS Leveraged Loan Index – The S&P UBS Leveraged Loan Index represents tradable, senior-secured, U.S. dollar-denominated non-investment grade loans.

Other

PME (Public Market Equivalent) – Calculated by taking the fund cash flows and investing them in a relevant index. The fund cash flows are pooled such that capital calls are simulated as index share purchases and distributions as index share sales. Contributions are scaled by a factor such that the ending portfolio balance is equal to the private equity net asset value (equal ending exposures for both portfolios). This seeks to prevent shorting of the public market equivalent portfolio. Distributions are not scaled by this factor. The IRR is calculated based off of these adjusted cash flows.

Time-weighted Return – Time-weighted return is a measure of compound rate of growth in a portfolio

This document has been prepared solely for informational purposes and contains proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this document are requested to maintain the confidentiality of the information contained herein. This document may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which affected markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of 2/18/2026