Built To Last: Private Credit’s $1.7 Trillion Opportunity

Executive Summary:

- Although not perfect, 2025 largely validated our "Golden Age of Private Credit" thesis, with persistent supply-demand gaps, muted defaults and a continued higher-for-longer rate environment.

- The fundamentals that carried the asset class forward through 2025 are poised to continue into 2026.

- Private credit continues to be the favored financing option for borrowers with significant deployment runway going forward.

Reflection is a powerful tool. In April 2025, we published a piece in response to global investor questions regarding the potential end of the "Golden Age of Private Credit." Our conclusion was that the golden age had further room to run, rooted in the following fundamentals:

- A higher-for-longer rate environment leading to higher absolute yields.

- Private credit demand exceeding supply would create sector tailwinds.

- Consistent historical performance and public market benchmark outperformance.

- A muted default backdrop.

We begrudgingly wrapped the piece with a ‘looking ahead’ section amidst volatile policy pivots that required numerous pre-publication changes. We got most, but not all, of our predictions right. We were wrong in predicting that macroeconomic uncertainty would likely be accompanied by widening spreads. The opposite happened. Macroeconomic data related to employment, consumer spending, U.S. GDP, inflation and corporate earnings nudged market confidence upward, creating a risk-on and tightening-spread environment. This year, we explore whether the fundamentals that carried the golden age of private credit forward through 2025 will remain intact.

2025's private credit fundamentals

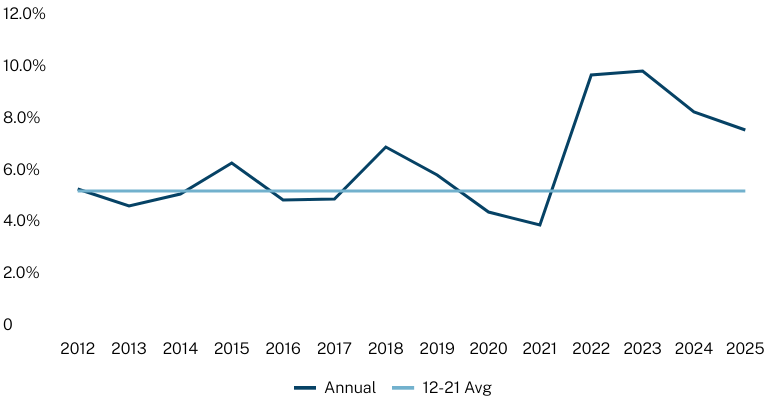

Higher for longer: While today's 3-month term SOFR is 65 bps lower than where we were at publication time in March 2025, the forward SOFR curve suggests investors are still poised to earn +200 bps of floating rate premium. Despite recent spread tightening, absolute all-in yields through 2036 should remain attractive relative to all-in yields in the decade leading up to 2022’s rising rate environment.

The leveraged loan market is healthy evidence of this. The yield-to-maturity (YTM) following 2022 has been +200 bps above the 2011 to 2022 average and is estimated to remain elevated based on the forward SOFR curve.

Leveraged Loan Market YTM

Source: Source: PitchBook | LCD, Data through December 31, 2025, unless otherwise noted.

We would be remiss if we didn’t point out that private credit spreads tightened in 2025 to approximately 450–500 bps for middle-market senior loans, creating pressure on absolute returns. Despite that, we expect higher returns over the next decade relative to the one leading up to 2022’s rising rate environment, making private credit an attractive place to find yield.

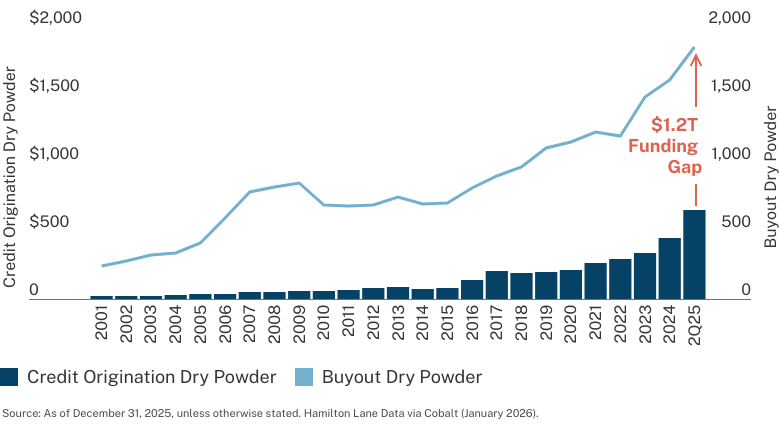

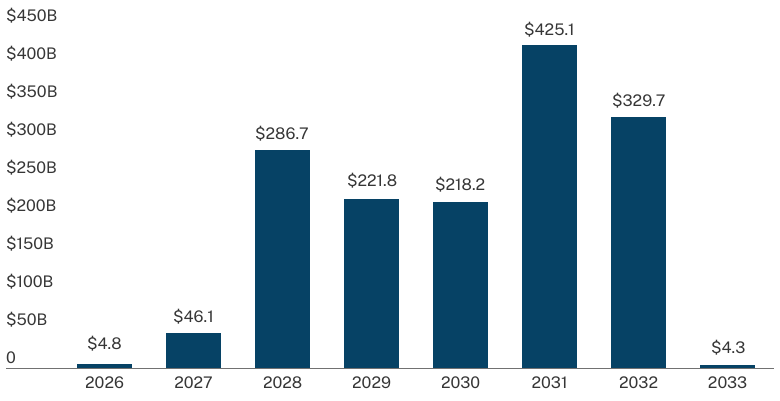

Demand exceeding supply: The funding gap between available private equity (PE) capital and credit origination dry powder persists. As of Q2 2025, there was a $1.2T funding gap between the amount of private equity buyout dry powder raised and the amount of credit origination raised. That gap declined from Q3 2024 to Q2 2025 by +$250B, largely due to an increase in the amount of credit origination dry powder. Despite that decline, when we marry the current funding gap with upcoming loan maturities, we estimate there is close to a $1.7T need over the next four years, suggesting private credit has ample deployment runway.

Buyout Credit Financing Demand

USD in Billions

Leveraged Loan Maturities

Source: PitchBook LCD. Data as of January 1, 2026.

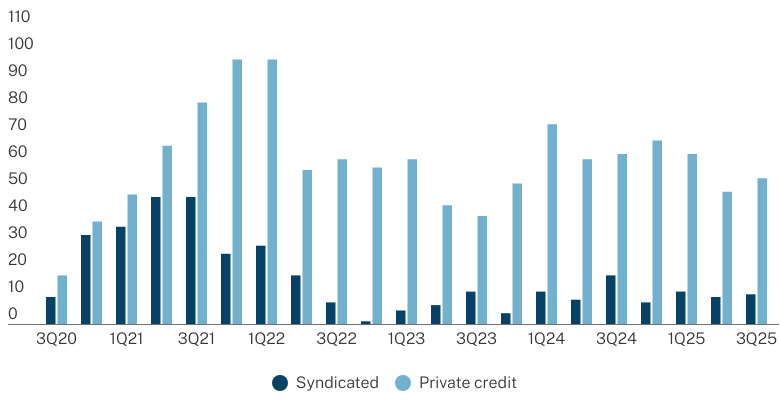

And consistent with last year’s article, our view is that it is unlikely the banks will close that funding gap. PE borrowers in particular tend to favor relationships, confidentiality and certainty of execution, which private credit can offer over bank-led financing. Just look at the count of leveraged buyouts (LBOs) in recent years financed by private credit versus the syndicated markets.

Count of LBOs Financed in BSL vs Private Credit Markets

Source: Pitchbook, LCD (9/30/2025, unless otherwise stated). Private credit count is based on transactions covered by LCD news.

Consistency of performance: Private credit continues to demonstrate positive vintage year IRR and benchmark outperformance, and the data speaks for itself.

Private Credit IRR vs PME

.webp?language=en-US)

Defaults: A resilient labor market and continued consumer spending continued to fuel growth in 2025. Through the end of 2025, the default rate remained muted yet again. In the leveraged loan market, the default rate was 1.18% by issuer count, which remained below the 25-year average of 2.15% and below average annual default levels following 2022’s rising rate environment of 1.34%.

Turning to the distressed ratio, a leading indicator of future default activity, December 2025 levels of 7.24% are in-line with the 25-year average of 7.2%. 2025 overall saw the distressed ratio ocellate between 4 and 7% throughout the year, which was generally lower than the 9-10% peaks seen in the 2022 and 2023 periods.

Closing thoughts

Our perspective is that the fundamentals remain intact. Today, senior-secured lending is well-positioned to stay the course and weather any potential macroeconomic or geopolitical headwinds. With a $1.7 trillion runway, private credit can offer investors the opportunity for continued yield and stability. This asset class is built to last.

Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.

Credit: This strategy focuses on providing debt capital.

Distressed Debt: Includes any PM fund that primarily invests in the debt of distressed companies.

S&P UBS Leveraged Loan Index: The S&P UBS Leveraged Loan Index represents tradable, senior-secured, U.S. dollar-denominated non-investment grade loans.

PME (Public Market Equivalent): Calculated by taking the fund cash flows and investing them in a relevant index. The fund cash flows are pooled such that capital calls are simulated as index share purchases and distributions as index share sales. Contributions are scaled by a factor such that the ending portfolio balance is equal to the private equity net asset value (equal ending exposures for both portfolios). This seeks to prevent shorting of the public market equivalent portfolio. Distributions are not scaled by this factor. The IRR is calculated based off of these adjusted cash flows.

This document has been prepared solely for informational purposes and contains proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this document are requested to maintain the confidentiality of the information contained herein. This document may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which affected markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of 2/18/2026