Weathering the Storm: Navigating Private Equity's New Reality Through the Middle Market

.webp?language=en-US)

Executive Summary:

- Global political and economic uncertainty have created a challenging climate for investment decisions, further exacerbating market volatility.

- Middle-market opportunities provide greater optionality to create value as well as an enhanced ability to find liquidity in the face of many of these headwinds.

- The One Big Beautiful Bill Act (OBBBA) and tariff impacts will continue to fuel growth for select domestic U.S. business profiles.

- Europe and certain APAC geographies continue to gain in attractiveness, especially as global economies decouple.

While we've heard a lot about that magical crystal ball that can foretell the future, we prefer to stick with what we know: historical private market performance, our current policy reality and direct middle-market investment. To start, here are some facts on the current U.S. macro, which like most places globally, still contains a fair bit of uncertainty on the horizon:

- Increased downside risks for labor markets and the economic growth outlook led to the Federal Reserve (the Fed) cutting interest rates by 25 bps in September.

- Inflation remains stubbornly above target and still likely faces upward pressure driven by immigration policies, additional tariff-driven impacts and currency pressure.

- The Fed remains data-dependent, and it now faces increasingly conflicting data points for managing its dual mandate of full employment and price stability.

- The recent U.S. government shutdown will limit the ability to access critical technical economic data at a pivotal juncture for monetary and fiscal policy decisions.

- The OBBBA incentivizes U.S. businesses through new and enhanced fiscal incentives designed to boost domestic jobs and national economic interests.

- The private markets are a long-term-focused asset class that has historically performed well in choppier economic conditions.

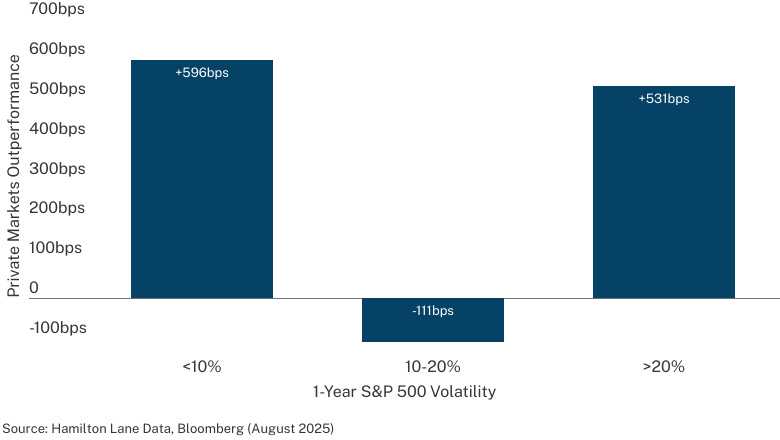

To that last point, the greatest outperformance for private markets historically happens in the years following either very low or very high volatility in the public markets. We are in the right-hand side of the chart below right now, and will likely continue to be for the foreseeable future.

Private Equity 1-Year Forward Outperformance By S&P Volatility

Think global, invest local

While it's a big, scary world out there, now is not the time for investors to run away from risk; it's the time to find the right businesses to lean into like those in the middle market. We believe that the long-term tailwinds already putting wind in the sails of many middle-market companies will be further fueled by the OBBBA, especially for companies focused on servicing North American businesses.

The recent whirlwind of tariff announcements, 90-day pauses, escalations, exclusions and the non-binding deals resulting from all the tumult has left both global and U.S. businesses searching for true north. When the question of whether 'to tariff or not to tariff' is unilaterally decided, business operations must adjust on the fly. North American middle-market businesses are favorably positioned, even in the face of tariffs and the OBBBA.

In the current macro environment where significant monetary, fiscal and tariff-related changes have increased volatility, agility is an LP's friend, and it can be found in spades across the middle market. Middle-market companies (e.g., businesses with <$3B in TEV), particularly those in more service-oriented segments, are more insulated from many of these broader global trade policy issues in terms of a revenue-and customer-demand profile that is much more localized. At the same time, these businesses have historically provided greater exit optionality for LPs compared to companies at the larger end of the market (e.g., businesses with $3 - $10B+ in TEV). Why? Because there are simply more ways to win, both in terms of operating performance, growth and the ability to exit. From exiting via strategic M&A to sponsor-to-sponsor deals and, notably, the recent uptick in continuation vehicles and GP-led liquidity solutions (higher velocity for mid-sized businesses), exposure to middle-market assets can help LPs stay agile, instead of waiting in line.

Middle-market companies also have a different risk profile. They're nimbler from a capital structure perspective because GPs typically don't pay as much for middle-market assets and there is typically less leverage in these businesses, which is a good recipe for navigating uncertainty.

"Sorry, ATM broken, come back tomorrow"

While investors contend with a lack of liquidity, the potential ripple effects of the OBBBA and tariff-driven uncertainty, opportunities may emerge for those prepared to adapt, particularly in key sectors of the economy benefiting from tailwinds such as businesses servicing private infrastructure and – perhaps surprisingly – healthcare.

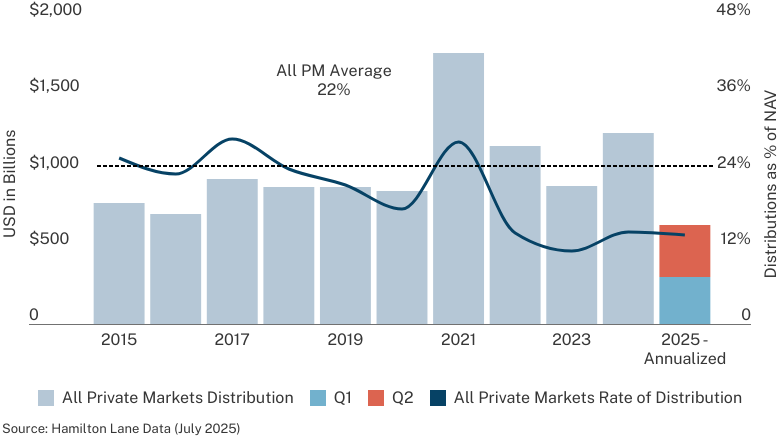

All Private Markets Rate of Distribution

What may not be a surprise is that overall private markets distribution rates are down, and LPs want to know when exits are going to pick up. But – like an ATM that's out of service – the window for accessing liquidity largely remains shut, particularly at the large/mega end of the market where IPOs are the main way to realize return potential. Fortunately, it's not 1999 anymore and there are more opportunities for LPs to access liquidity from private markets assets than IPOs alone, even as uncertainty abounds.

Middle-Market Buyout Exit Types

Deal Vintages 2004-2024

While the IPO market may be beginning to open again for large/mega funds, that's really the only practical exit strategy these funds have by nature of their scale. In contrast, over the last 20 years, middle-market deals have only exited via IPO 12% of the time. Even as the IPO market thaws, potential returns can remain locked up for the next 18 months – or longer depending on when the GP decides to sell shares – taking on public market risk without the benefit of liquidity access. That's like seeing the broken ATM come back to life and needing to wait in line because your card won't work. Will the window of opportunity close again before you can get your money out? Will your returns be worth less by the time your card works with the ATM?

Key sectoral themes

We like North American business services that cater to mid-sized businesses, particularly those in legal, accounting, consulting, tech, infrastructure and healthcare services sectors. These segments have historically generated consistent revenue streams across varying economic cycles. These businesses are defensible, typically fragmented across different states and service niche, local markets with their own jurisdictional legal and permitting rules. Good companies are not going to cut contracts with the legal, accounting or tech services that have a true value proposition and make their jobs easier (dare we say possible?) in the face of macroeconomic uncertainty just to cut costs. In the middle market, these business services are perennially needed and are not going anywhere anytime soon. What other types of businesses can continue flourishing and, better yet, accelerate because of the OBBBA?

Everybody needs healthcare (services)

Perhaps an unexpected result of the OBBBA becoming law is that companies servicing the healthcare industry stand to benefit. The OBBBA created new tax deduction opportunities for this sector, so any capital invested across domestic R&D, pharmaceuticals and supply chain development can lower capital expenses and make a big impact for small-to-mid-sized companies.

While U.S. healthcare policy may seem volatile today, there are corners of the market which we believe will continue to be needed and continue to generate revenue, regardless of the administration or economic cycle. For example, there are behavioral and mental healthcare companies, which provide essential services to underserved portions of the population, helping people with sub-acute eating disorders recover and prevent expensive, potentially recurrent hospital visits. These are important healthcare services – for patients, insurance companies and the broader U.S. economy. With what we believe to be only 15% of this demographic served today, providing services to support underserved patients can lead to better overall outcomes.

Other healthcare services companies, such as those that provide hospice care, can also help support our growing, aging population. While the OBBBA rolled back Medicaid support, which may impact insurance providers including Medicare down the line, everybody ages, and we don't think Medicare reimbursements are currently at risk. Hospice care has been a mainstay of Medicare insurance for a very long time. Over the last 20 years, reimbursement rates have increased ~1-3% per annum and are expected to be highly stable given bipartisan congressional support. Is this a risk worth underwriting? Maybe. Is the assumption that OBBBA policy changes will slash Medicare's hospice care business model by 10% reasonable? We don't think so. What about other essential components of the healthcare picture like pharmaceuticals?

Larger international pharmaceutical companies manufacturing medicine offshore may run into global supply chain issues, unfavorable market dynamics resulting from the OBBBA and longer-term tariff costs. However, small-to-mid-sized domestic pharmaceutical companies are positioned to pick up some of that loss. In addition to new tax incentives legislated through the OBBBA, Trump signed Executive Orders in April and August focused on the domestic manufacturing of pharmaceutical ingredients and more resilient domestic supply chains. In September, he issued 100% tariffs on foreign pharmaceuticals. That's quite the flurry of healthcare services activity. But the takeaway from all of it is that healthcare is essential and the companies servicing this sector have historically been all-weather investments. Partnering with asset managers who have access and the ability to be selective can help LPs construct portfolios with exposure to the right healthcare services for them, even when uncertainty seems to take a new form every day.

The ripple effect of America’s electrification and the AI boom

Okay, we couldn’t resist using the terms ‘electrification’ or ‘AI boom.’ Nevertheless, domestic energy, utilities, telecom and next-generation technology services are well-positioned to capture the OBBBA's tailwinds and ride existing macro trends. One of the many things that the nearly 1,000-page OBBBA did was prioritize domestic infrastructure and onshoring, with a key focus on bigger and better North American energy independence – both from a national security standpoint and to incentivize greater future capacity – so that U.S. chip manufacturing, data center and hyperscaler development can accelerate.

While the domestic oil and gas industry is poised to benefit from the OBBBA's deductibility expansion in the short term, our long-term outlook remains unchanged. The sector remains exposed to geopolitical and commodity risks because administrations change, and so does the price of oil and gas. However, the U.S.'s increased focus on the data centers powering AI and our digital economy demands a more efficient and resilient electrical grid, along with significantly more power than we can currently supply. Both brand new energy grid infrastructure and the continued maintenance of what we already have will be needed. Enter grid-servicing companies.

Companies that provide consulting, engineering or service to the electric grid can help balance both sides of this supply-demand equation. In addition to facilitating new infrastructure builds that generate more supply from the outset, infrastructure services companies can optimize and maintain existing grid performance and alleviate current capacity constraints. We have seen attractive companies specializing in this across the (power) spectrum - those which provide the highly skilled technicians needed to service, maintain and repair outdated North American transformers, substations, switchgears and other power distribution equipment and those which manage services and counsel businesses, utilities and state authorities to achieve energy transition and efficiency goals. These types of businesses are well-positioned to capture growth from current and foreseeable infrastructure tailwinds as well as the inherent downside protection that comes along with the sector.

While the OBBBA rolled back some tax credit incentives for wind and solar projects which the Inflation Reduction Act (IRA) initially expanded, it also created new incentives for fuel center, nuclear facilities and utility companies, which will be needed to meet our rapidly expanding energy demand. Utility service providers advising data center and hyperscaler developers on how to bolster electricity and interconnect capacity are already in high demand. And the OBBBA's domestic utility incentives make the case for their bullish momentum to continue, especially in the middle market where companies can adapt to state and national infrastructure needs through roll-ups and strategic M&A. With data centers projected to consume between 6.7% and 12% of all electricity generated in the U.S. by 2028, up from ~4.4% in 20231 and an archaic existing electric grid across the U.S., we believe that these specialized infrastructure services can drive further economic growth and upside potential for LPs.

Love letters to Europe and APAC

Despite tariffs, most U.S. middle-market services are not subject to international supply chain risk. Similarly, country-specific or regionally focused middle-market companies in Europe and APAC present attractive opportunities because, in many cases, they are not exposed to global supply chain risks, given the domestic nature of the goods or services offered. As countries are forced to look and grow inward, certain industries will be beneficiaries. We believe country-specific and regional middle-market companies, particularly those in Europe and APAC, are favorably positioned.

The new tariff regime is increasingly making the case for European direct equity. Not just because the OBBBA's prioritization of domestic production opens up European markets to trade with other countries, but also because many middle-market European businesses are shielded from tariffs, in a similar manner that other mid-sized, domestically focused companies can generate revenue. Local customers, local revenue and local currency generate resiliency in the face of greater global trade uncertainty.

Middle-market services companies across Spain, Germany, France, Italy and other European countries can more easily pivot than large/mega companies because they are not as dependent on global supply chains and they have the local expertise needed to adapt to an evolving trade environment. As the U.S. looks to facilitate more goods trade to Europe, we believe that – provided a healthy macroeconomic backdrop – more country-specific, service-oriented businesses can thrive, regardless of what the geopolitical reshuffling looks like. Managers with local expertise are poised to take advantage of these regional opportunities and others, including…

Regionally Focused Buyout Funds in Europe

By All GPs

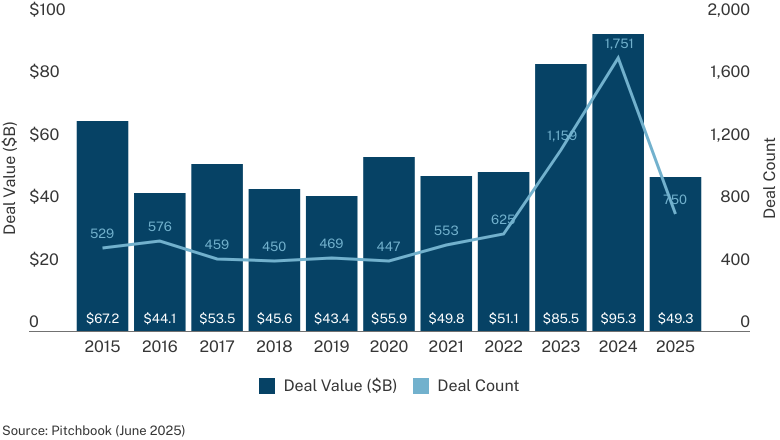

Tactical geographic selection across APAC, which will remain paramount. A similar dynamic will reward asset selection and overall company quality. The global trade reshuffling has opened up more investment opportunities across Japan, Korea, Australia and South East Asia, which have traditionally been consumer- and service-oriented geographies. Pharmaceuticals, technology and business services, which have typically done well here, can continue to do well, especially in the middle market where investor appetite is growing. These geographies are poised to experience modest economic growth, amidst declining inflation and more accommodating monetary policies, creating added tailwinds. As shown below, the M&A market is taking note of these dynamics.

Japan M&A activity

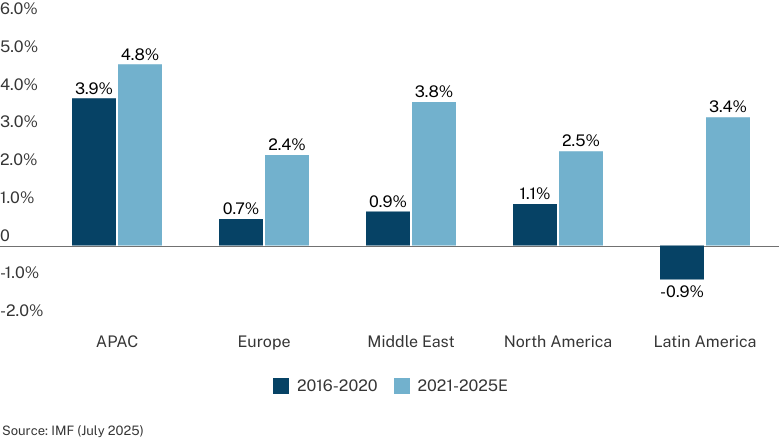

Additionally, Asia has been a principal driver of global growth, with annual growth in real GDP increasing since 2016 and buyout deals with entry valuations moving lower in recent years.

Annual Growth in Real GDP

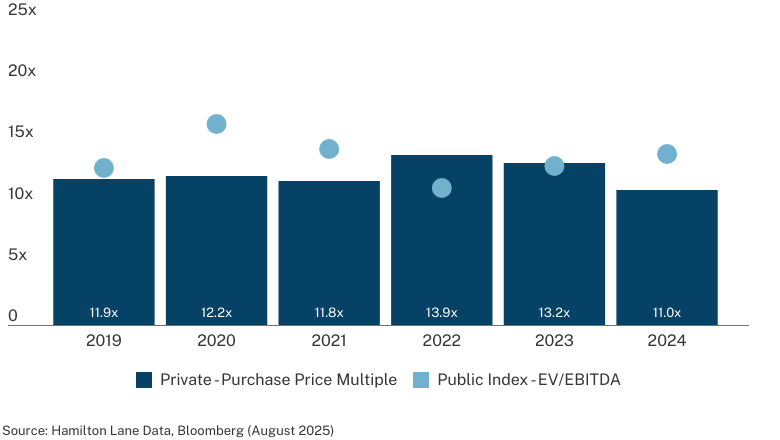

APAC Buyout Purchase Prices

Median EV/EBITDA by Deal Year

The tariff impact on APAC countries has been muted so far and, given the region's growing value to the global supply chain, it would be prudent for LPs to keep a close eye on its increasingly critical pharmaceutical, technology and business services sectors. As supply chains become less reliant on the U.S., we believe that suppliers will continue to negotiate on margins in the short-term and create new trade partnerships in the long-term. That's not an opportunity to sleep on.

Turn the ATM back on

Nobody likes uncertainty, but it's not all doom and gloom. Middle-market companies offering essential services across bellwether sectors like infrastructure and healthcare have a long history of generating attractive returns for investors with solid downside protection. We like these businesses because they can provide LPs with more opportunities akin to a private bank: greater access to a wider array of global investments and the flexibility to generate liquidity without waiting for what can seem like an eternity. In an ever-changing and volatile macro environment, finding managers with the requisite expertise to access, diligence and invest in these deals can help LPs reboot that ATM and gain access to the cash and returns that they have been seeking.

All Private Markets – Hamilton Lane’s definition of “All Private Markets” includes all private commingled funds excluding fund-of-funds, and secondary fund-of-funds.

Private Equity – A broad term used to describe any fund that offers equity capital to private companies.

S&P 500 Index – The S&P 500 Index tracks 500 largest companies based on market capitalization of companies listed on NYSE or NASDAQ.

SMID Buyout – Any buyout fund smaller than a certain fund size, dependent on vintage year.

Mega/Large Buyout – Any buyout fund larger than a certain fund size that depends on the vintage year.

EU Buyout – Any buyout fund primarily investing in the European Union.

DM Buyout – Includes any buyout fund that is primarily investing in developed markets of North America, Western Europe and Global.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which is affecting markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot

be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of 10/16/2025