Nobody Ever Got Fired for Buying Senior Credit

What you will learn

- The important ways in which senior private credit can afford investors downside protection

- How the returns of senior credit stack up relative to the leveraged loan index

- Ways in which evergreen structures create differentiated access to senior private credit, delivering the potential for safety and yield.

“Nobody ever got fired for buying IBM,” is a saying that’s been floating around investor circles for decades. The now-legendary catchphrase has been used to imply that IBM was the ultimate safe bet for investors. Likewise, if private markets had a catchy sound bite today, it would have to be, “Nobody ever got fired for buying senior credit.” And there are several reasons for this, including:

- Due to its floating rate nature, yields on senior credit increase as interest rates rise

- Private credit has historically demonstrated resilience and consistent performance through up and down markets

- The strategy has become more accessible than ever – and it could be just the answer many investors are looking for today

Senior private credit may be that port in the storm for investors

The Federal Reserve’s crusade against inflation continues to result in interest rate hikes, which is generally encouraging news for senior private credit investors. For perspective, the industry’s reference rate, known as SOFR (or Secured Overnight Financing Rate), began 2022 at 0.05%. This left lenders largely dependent on SOFR floors – which typically ranged from 50-100 basis points (bps) – for pricing protection. In simple terms, a first lien term loan priced at S+500 with a 100bps floor opened 2022 with a 6% annualized yield – i.e., 100bps floor + 500bps. By September 30, 2022, meanwhile, SOFR’s 30-day average increased to approximately 2.5% and the forward curve suggests SOFR could peak to ~4.9% by early 2023. The same S+500 deal will see its annualized yield increase to 9.9% – i.e., 490 bps + 500 bps – in roughly a year. Downside pricing protection and no ceiling are some of the many benefits of floating rate senior private credit and investors are currently experiencing increased yield.

We have all heard the expression, “Nothing in life comes free,” and yields are no exception. The reality is that increased interest expense could trigger rising defaults, which is an issue of concern for investors. Fortunately, the data suggests that credit quality has historically stayed strong during rate hike periods, which leaves private credit investors with plenty of reasons to remain optimistic.

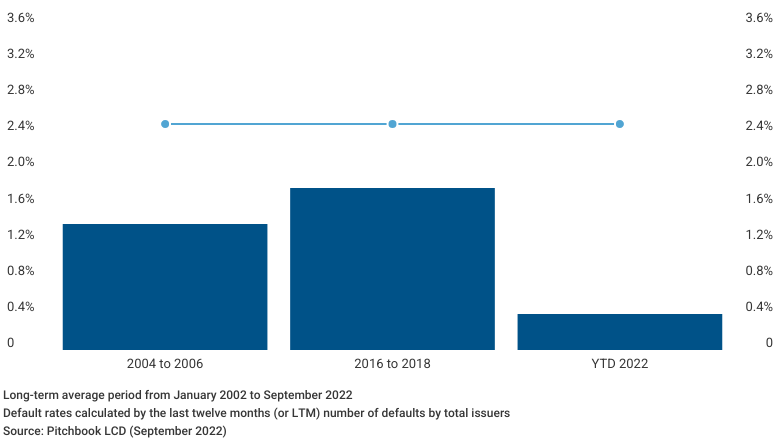

Looking back over the last 20 years, we have experienced three rising interest rate environments 1) 2004 to 2006, 2) 2016 to 2018, and 3) 2022. By deal count, leveraged loans averaged default rates of 1.4%, 1.8% and 0.4%, respectively, which in all cases was below the 20-year average of 2.5%. In the three years that followed the 2004 to 2006 and 2016 to 2018 rate hike periods, default rates averaged 3.2% and 1.9%, nowhere near the 20-year peak of 8.2%. Recognizing that history does not necessarily repeat itself, manager selection is critical to mitigating performance risk. And, as we mentioned previously, GPs with scale, deal access and investment discipline may be better positioned to prevail.

Average LLI Default Rates

Mind the gap: Four ways senior credit can offer downside protection beyond a floating rate hedge

For investors seeking downside protection, risk-adjusted returns and attractive floating cash yield, there are four reasons why senior credit may be the right solution:

- First lien position. Aside from the advantages of largely floating rate instruments, senior credit also has a lot to offer in terms of structural features that can provide stability and enhance the attractiveness of the asset class as an all-weather strategy. Some of these aspects are relatively intuitive: Senior credit sits at the top of the capital structure in a first lien, dollar one position. While equity and junior debt may offer more upside and return potential, this priority means that senior credit is the last security to be impaired if a company underperforms. And with long-term recovery rates on first lien bank term loans averaging 75%, even in a worst-case scenario, the high potential for capital preservation remains strong.

- Cash flow. From a cash flow standpoint, senior credit may offer quarterly cash payments and typically provides some level of principal amortization. In addition, as a company pays interest and principal, not only does the company pay down its debt balance – and, by extension, helps reduce its risk exposure – but the lender’s at-risk capital can decrease as it receives cash distributions.

- Governance. While considerable ink has been spilled over the shift in recent years to covenant-lite structures, senior credit still offers a reasonable amount of controls on the business and sponsor’s activities. Financial reporting, distributions out of the business, transfer of assets and incurrence of additional debt are all areas that may be covered under the affirmative and negative covenants in a credit agreement. Granted, even though the devil is still in the details, lenders are nonetheless afforded these important protections.

- Sponsor capital. Senior credit, especially within the private debt landscape, often sits alongside investments from a private equity sponsor. In addition to providing a cash equity infusion into the business, sponsors typically offer a level of oversight, resources and direction that may otherwise be lacking in a non-sponsored, middle-market business. And while it’s challenging to lump sponsor activity into a universally consistent approach, very frequently fresh sponsor capital will be the first line of defense if a company needs additional liquidity.

Show me the money – and returns

The downside protection notwithstanding, we’re commonly asked, “How do the returns of senior credit stack up?” There’s good news: Senior credit has historically shown a considerable degree of outperformance over the last eight years relative to the leveraged loan index.

Senior Credit Pooled IRR vs. PME

| Vintage | Senior Credit IRR | Credit Suisse Leveraged Loan Index PME |

| 2014 - 2015 | 6.9% | 4.2% |

| 2016 | 8.6% | 4.6% |

| 2017 | 8.5% | 4.2% |

| 2018 | 8.7% | 4.2% |

| 2019 | 9.4% | 4.8% |

| 2020 | 16.8% | 7.0% |

| 2021 | 9.0% | 3.3% |

Source: Hamilton Lane Data via Cobalt, Bloomberg (September 2022). Please see definitions in endnotes.

Even measured against the broader index of private credit, senior credit can offer a favorable level of volatility and risk/return measurement as well.

Seven-Year Credit Risk Adjusted Returns

| Asset Class | Annualized Total Return | Annualized Volatility | Sharpe Ratio |

| All Private Credit | 8.1% | 6.0% | 1.03 |

| Senior Credit | 8.4% | 4.0% | 1.63 |

| Bloomberg Aggregate Bond Index | 3.3% | 7.9% | 0.18 |

| Credit Suisse Leveraged Loan Index | 4.1% | 7.2% | 0.30 |

| Credit Suisse High Yield Index | 4.9% | 9.1% | 0.32 |

*As of 3/31/2022

Source: Hamilton Lane Data via Cobalt, Bloomberg. Indices used: Hamilton Lane Private Credit with volatility de-smoothed; Hamilton Lane Private Senior Debt with volatility de-smoothed; Credit Suisse High Yield Index; Barclays Aggregated Bond Index; Credit Suisse Leveraged Loan Index. Geometric mean returns in USD. Assumes risk free rate of 1.9%, representing the average yield of the ten-year treasury over the last seven years. (September 2022)

With these return and structural features in mind, you can see why there is increased investor demand for senior credit investment products.

Evergreen funds allow investors greater access to senior private credit – and the potential for safety – than ever before

The introduction of the private credit evergreen fund can best be characterized as the democratization of private credit. Up until recently, private credit was largely accessed through closed-end funds, which were primarily designed for institutional investors due to their larger minimum investment requirements, among other factors. Structurally, closed-end funds differ from evergreen structures as investors or LPs are required to make a capital commitment, which typically gets called over a three- to five-year period. Timing of liquidity for closed-end structures is typically outside of the LP's control and dictated by exit activity, distributions and the GP's decision to recycle capital.

The evergreen structure changed the structural and access paradigm, and has now opened the door to a broader investor base. Structurally, these vehicles are often designed as private, non-traded business development companies (BDCs) with investment minimums as low as $25,000. Upon subscription to the fund (often through a financial advisor), capital is fully deployed. Bear in mind, this is quite different from a traditional fund structure, which draws capital over the commitment period. Further, from a liquidity standpoint, evergreen structures typically offer investors the ability to redeem up to 5% of their net asset value per quarter, giving investors greater control over liquidity as compared to traditional fund structures. Additionally, these vehicles aim to distribute income on a regular basis.

Retail access to credit, however, is not an entirely new construct. While private BDCs are credited with democratizing access, public BDCs have been available on exchanges such as the NYSE or NASDAQ dating as far back as the 1990s. The key differentiators between the private and public BDCs are two-fold: 1) use of leverage and 2) exposure to public markets fluctuations. Private BDCs, or evergreen funds, typically target up to 1.0x leverage, whereas publicly traded BDCs are permitted up to 2.0x leverage based on the Small Business Credit Availability Act. This higher threshold for leverage creates the perception that publicly traded BDCs are riskier. As an example, one dollar lent to a company from a private BDC with 1.0x leverage will include $0.50 of investor equity and $0.50 of leverage. By contrast, a public BDC with 2.0x leverage lending the same dollar will be made up of approximately $0.33 of investor equity and $0.67 of leverage.

Market volatility tends to have a greater impact on public BDCs versus private ones, as market downturns can impact public BDC share prices. This can lead to challenges in raising capital, particularly in environments where a BDC’s price is trading below book value. Non-traded evergreen funds, on the other hand, are not as susceptible to public markets volatility. As a result, raising capital involves less volatility – assuming both portfolios are equal. One of the investor trade-offs between a public versus non-public BDC is the ability to seek full and immediate liquidity through a public structure as public BDCs can be sold almost immediately, much like any over-the-counter stock.

Ultimately, each structure (i.e., traditional closed-end fund, evergreen structure or public BDC) is designed to accommodate different investor types and considerations. What is consistent across vehicles is their ability to create access to middle-market, senior lending transactions. The bottom line is that investors have more choice than ever with lower access friction, which encourages greater participation and growth opportunities for senior private lending.

The Wrap: Amid the recent market volatility, investors deserve a break

So where does that leave us? Investors already had a challenging job navigating the increasingly complex assortment of investment strategies and vehicles, even before the macroeconomic uncertainties of the last several months. The volatility concerns and rising interest rates, notwithstanding, investors may find a friend in private credit because of its floating rate nature and the potential for consistency of performance through up and down markets. And if your personal risk tolerance is to avoid getting fired, senior credit may be the right choice for you as well.

All Private Markets – Hamilton Lane’s definition of “All Private Markets” includes all private commingled funds excluding fund-of-funds, and secondary fund-of-funds.

Corporate Finance/Buyout – Any PM fund that generally takes control position by buying a company.

Credit – This strategy focuses on providing debt capital.

Infrastructure – An investment strategy that invests in physical systems involved in the distribution of people, goods, and resources.

Mega/Large Buyout – Any buyout fund larger than a certain fund size that depends on the vintage year.

Natural Resources – An investment strategy that invests in companies involved in the extraction, refinement, or distribution of natural resources.

Origination – Includes any PM fund that focuses primarily on providing debt capital directly to private companies, often using the company’s assets as collateral.

Private Equity – A broad term used to describe any fund that offers equity capital to private companies.

Real Assets – Real Assets includes any PM fund with a strategy of Infrastructure, Natural Resources, or Real Estate.

Real Estate – Any closed-end fund that primarily invests in non-core real estate, excluding separate accounts and joint ventures.

SMID Buyout – Any buyout fund smaller than a certain fund size, dependent on vintage year.

U.S. Mega/Large – Any buyout fund larger than a certain fund size that depends on the vintage year and is primarily investing in the United States.

U.S. SMID – Any buyout fund smaller than a certain fund size that depends on the vintage year and is primarily investing in the United States.

VC/Growth – Includes all funds with a strategy of venture capital or growth equity.

Index Definitions

Bloomberg Aggregate Bond Index - The Bloomberg Aggregate Bond Index,is a benchmark used to measure a bond fund’s relative performance.

BofAML High Yield Index – The BofAML High Yield index tracks the performance of below investment grade U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market.

Credit Suisse High Yield Index – The Credit Suisse High Yield index tracks the performance of U.S. sub-investment grade bonds.

Credit Suisse Leveraged Loan Index – The CS Leveraged Loan Index represents tradable, senior-secured, U.S. dollar-denominated non-investment grade loans.

FTSE/NAREIR Equity REIT Index – The FTSE/NAREIT All Equity REIT Index tracks the performance of U.S. equity REITs.

MSCI World Energy Sector Index – The MSCI World Energy Sector Index measures the performance of securities classified in the GICS Energy sector.

MSCI World Index – The MSCI World Index tracks large and mid-cap equity performance in developed market countries.

S&P Global Infrastructure Index – The S&P Global Infrastructure Index tracks the performance of 75 companies from around the world that represent the infrastructure industry.

Other

PME (Public Market Equivalent) – Calculated by taking the fund cash flows and investing them in a relevant index. The fund cash flows are pooled such that capital calls are simulated as index share purchases and distributions as index share sales. Contributions are scaled by a factor such that the ending portfolio balance is equal to the private equity net asset value (equal ending exposures for both portfolios). This seeks to prevent shorting of the public market equivalent portfolio. Distributions are not scaled by this factor. The IRR is calculated based on these adjusted cash flows.