2026 Infrastructure Outlook: Navigating European Energy Security, AI Demand and the Secondary Market

Executive Summary:

- 2026 marks a year of infrastructure expansion as Europe doubles down on energy security, while the intersection of power and AI-driven digital infrastructure continue to drive global investment.

- While power and data centers have received the most attention, last-mile fiber rings to key data center hubs remains underserved, while fiber-to-the-home enters a period of consolidation.

- Despite policy headwinds, U.S. renewables have proven resilient and power scarcity has continued to support higher PPA prices in the market.

- Public markets have repriced the growth expectations in cold storage, but specialty logistical infrastructure remains attractive in markets with structurally short supply.

- Infrastructure secondaries can be a treasure chest, but scaled platforms with relationship capital are critical to access sought-after assets with upside potential.

2025 was a gravity-defying year for infrastructure investors. While AI drove massive capital investment into specific infrastructure sectors, U.S. policy changes disproportionately hurt others. Despite the pendulum swinging back and forth between market exuberance and regulatory uncertainty, institutional investors returned to the asset class en masse, and old school infrastructure sectors suddenly became cool again. That revival has been especially apparent in Europe, where other tried-and-true themes have been playing out through renewed investments in energy security.

Securing European energy

As 20th century Ukrainian American psychologist Abraham Maslow made famous in his foundational theory, the “Hierarchy of Needs,” security comes before growth. In 2026, we see Europe channeling Maslow’s theory, investing heavily in energy security to grow the continent’s essential infrastructure. And for good reason.

In 2021, both Europe and the U.S. were coming out of Covid at similar growth rates of ~6% gross domestic product (GPD). In the years that followed, energy policy and Russia’s invasion of Ukraine turned Europe’s energy markets upside down. Since 2022, the U.S. has averaged annual GDP growth of ~2.4%, while European growth has only reached 1.4%, most of which was front-loaded in 2022, with the last three years hitting 0.5-1%.

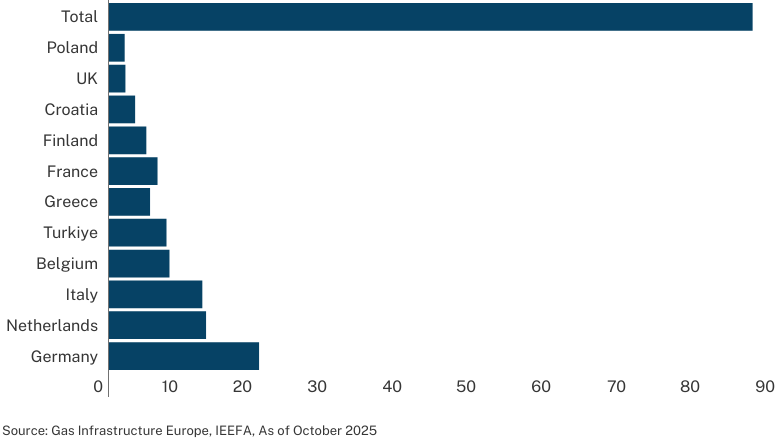

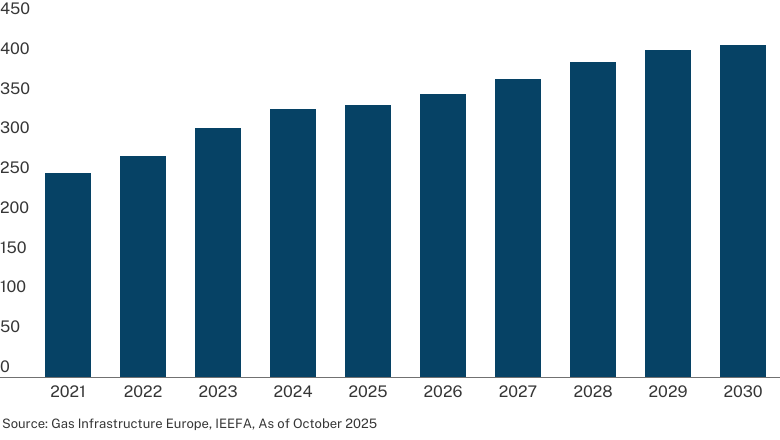

Having recognized that its dependence on Russian gas had become a growth bottleneck, Europe has since invested heavily in energy infrastructure. In total, the EU has added over 85 billion cubic meters (bcm) of liquified natural gas (LNG) capacity in the last three years. Total capacity in Europe now stands at over 400 bcm, up ~75% from 2021 levels, as LNG becomes a key transition fuel.

LNG Capacity Additions Since February 2022 (bcm)

Europe Existing and Planned LNG Regasification Capacity (bcm)

Projected growth this year is expected to hit 1.5%, up from 1% last year, and closer in line with longer-term averages for the region. One sub-sector that we find particularly interesting is floating storage and regassification units (FSRUs). The EU throttling Russian gas supplies has accelerated LNG imports and elevated FSRUs as critical infrastructure for European energy security. Countries like Germany and Lithuania, for example, have pivoted decisively toward LNG to diversify supply.

The global LNG market is experiencing robust growth too, driven by the increasing role of natural gas as a transition fuel. LNG consumption is now projected to grow to ~900+ bcm by 2040, with FSRUs expected to increase in tandem, to meet demand in European regions that lack pipeline infrastructure or which need rapid deployment solutions. With energy infrastructure secured, Europe’s foundational economic needs can be met, and today’s modern equivalent to oil and gas — digital infrastructure — can be built up.

Scaling fiber for AI demand

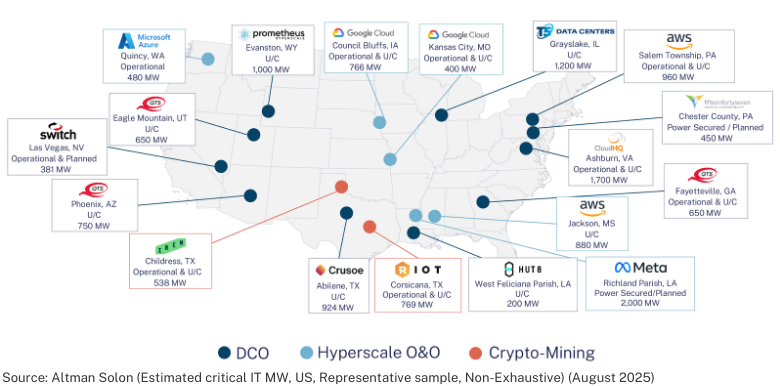

While data center opportunities have been front and center, the digital highways connecting them to each other and downstream users have been underserved. New-build fiber capacity needed to connect emerging data center hubs will be required as fiber-to-the-home improvements are entering a period of consolidation. Below is a map showing the announced data center mega-campuses in the U.S. that are expected to power large-scale AI training and inference models.

National Announced Mega-Campus Deployments

These announcements represent over 12 GW of new build data center capacity, which will require significant fiber buildout in denser and longer fiber networks.

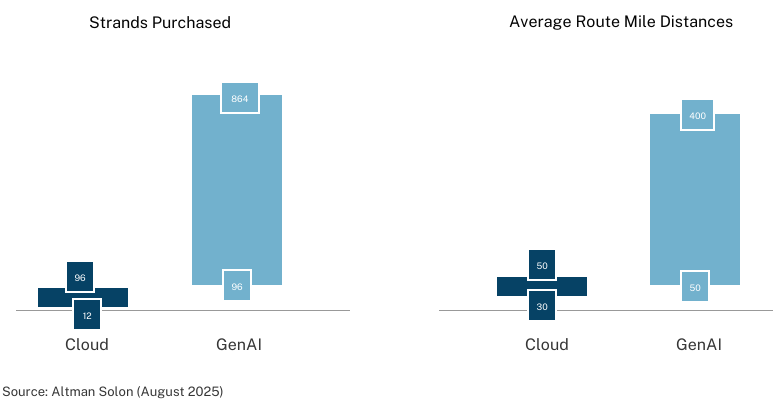

Traditional Cloud vs. GenAI Network Requirements

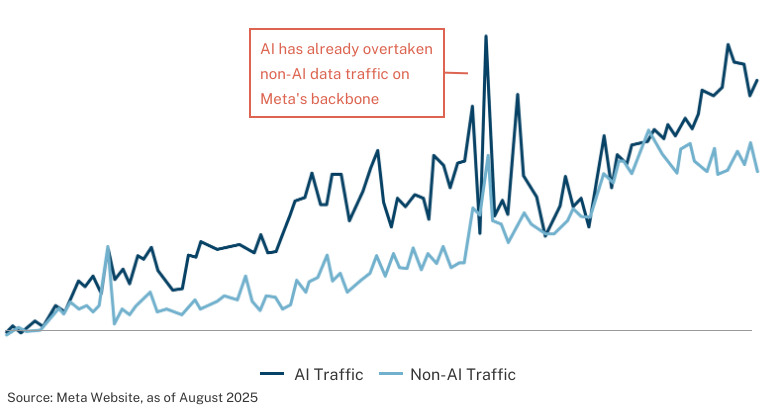

Meta Backbone Traffic by Source

Unitless chart from Meta's Scale presentation

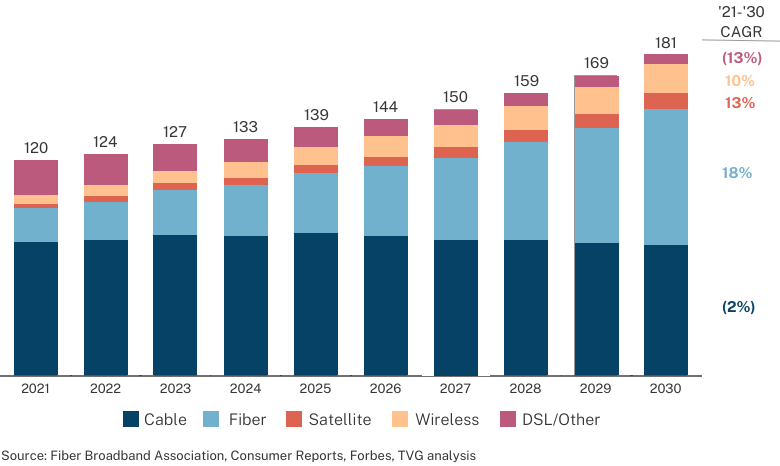

Looking at fiber-to-the-home investments, growth opportunities remain strong, while market fragmentation represents a compelling consolidation play for the right management teams. Fiber is expected to grow from ~25% of the U.S. broadband market to 42% over the next five years, while cable is expected to shrink from ~55% to 40%.

U.S. Residential Broadband Subscribers by Types

Millions, 2021-2030

Moreover, consumers are demanding faster delivery speeds for more data-intensive applications, and legacy copper lines have reached their performance limit, even with new technologies rolling out. This fragmentation creates attractive consolidation opportunities, as many providers still struggle to achieve commercial scale.

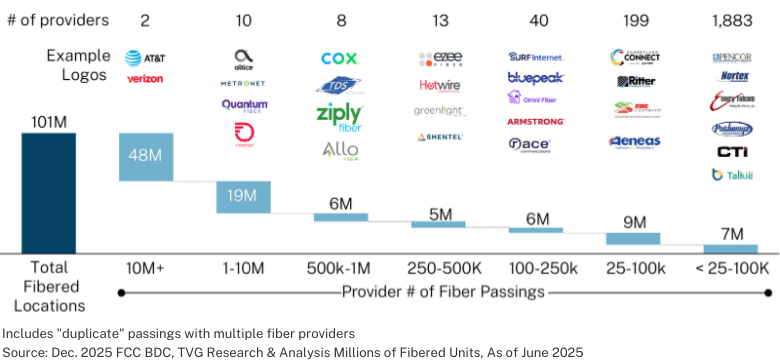

As illustrated below, the top 12 providers account for ~66% of the fiberized locations, while the remaining 34% is provided by the remaining 1,450 providers, with the bulk of those surpassing fewer than 25,000 residences. Multiple expansion through consolidation is compelling here, with acquisition multiples for sub-scale, single-city platforms ranging from 6-8x, while multiples for scaled platforms can reach 16-20x.

Fiber Passings1 by Footprint Size

M of Fibered Units, As of June 2025

Renewables catch their breath

While the One Big Beautiful Bill Act (OBBBA) gut-punched the renewables sector in 2025, growing power demands and rising purchase power agreement (PPA) prices have helped asset owners absorb the blow, as shown by the U.S.’s trailing 6-year renewable transaction activity below. Despite the regulatory changes to federal production and investment tax credits, transaction activity remained strong through Q3 2025.

U.S. Renewables Transaction Volume and Count

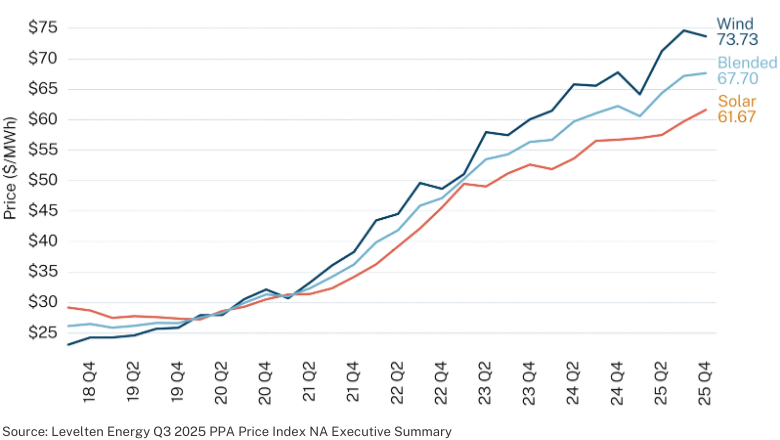

Rising PPA prices are helping developers offset reduced credit values as federal credits, which have supported the U.S. renewable sector over the past five years, begin to roll off. Why? Renewables remain one of the easiest forms of bulk generation to install in the U.S. With increasing power demand and significant constraints in new gas-fired generation, renewable contracting remains strong, especially from corporate counterparties. Contrary to some headlines, renewables have not been left out in the cold.

Market-Averaged U.S. Continental PPA Index

Favorable cold storage dynamics

As a sub-sector, cold storage is a relative newcomer, but one that fits traditional infrastructure characteristics, including high barriers to entry, long contract structures with credit-quality tenants and strong cash yields. And investors are warming to private cold storage companies.

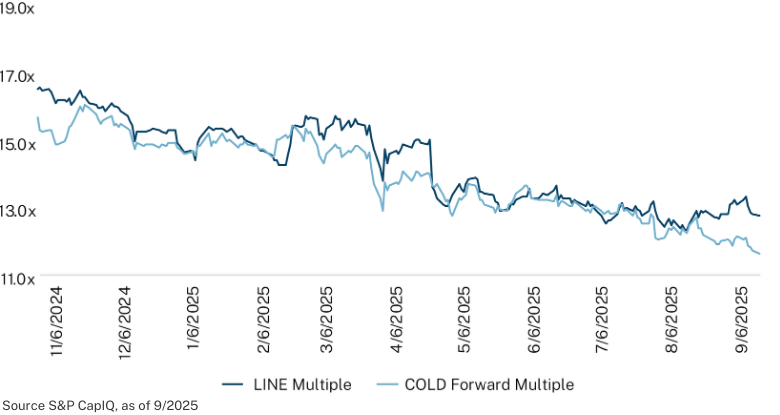

Today, the industry is dominated by two large public players, Lineage and Americold, which have been under pressure over the last 18 months, with EV to EBITDA multiples falling from 18-22x to 14-16x, respectively.

EV/NTM EBITDA Multiples: LINE vs COLD

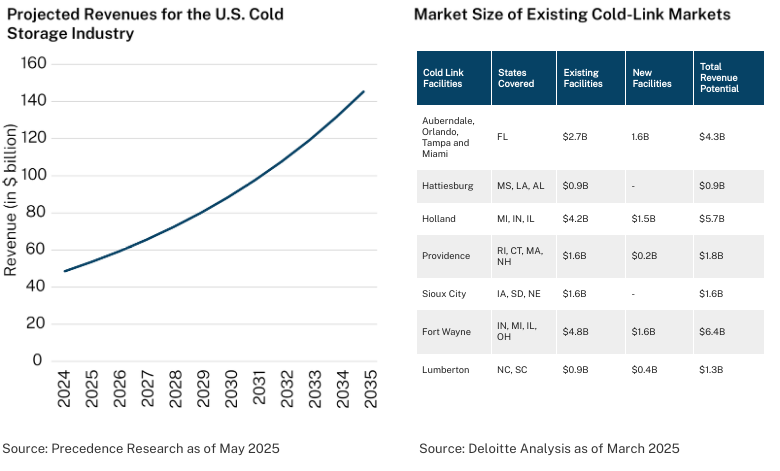

Slower growth prospects post-Covid, increased new supply in certain markets and reduced pricing power account for these declines. While cold storage headwinds persist, we believe in the sector and think that the pricing softness represents a good entry point for scaled, market-specific platforms, with demand and resulting revenues expected to grow by 8-10% over the next decade.

While increasing, supply is still muted relative to demand. Scaled platforms operating in tight supply markets with deep customer relationships, however, are very well-positioned for future growth. As the sub-sector grows, it can provide more opportunities to supplement existing infrastructure projects and add another pathway to liquidity potential for investors.

Infrastructure secondaries: From unexplored to treasure chest

Previously unexplored, today's secondary platforms can provide investors with a way to access and realize sought-after infrastructure assets. 15 years ago, the infrastructure secondary market was shallow, and single-asset deal quality wasn't optimal. Most deals trading in the secondary market at that time were characterized by poor business plan execution and no third-party exit market. Times have changed.

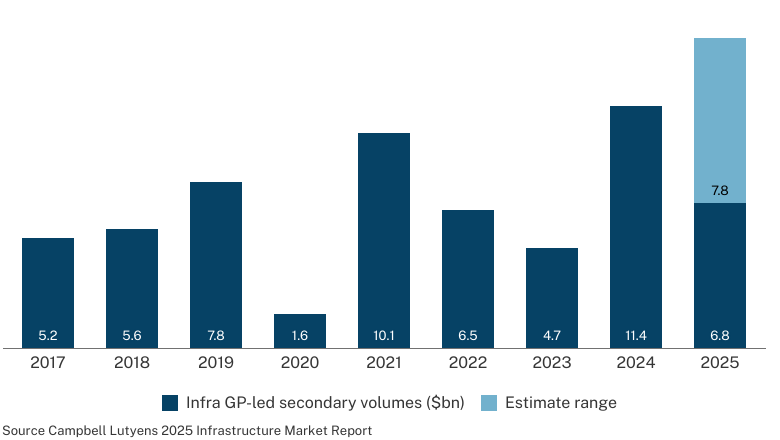

As shown above, infrastructure secondary pricing has held up the most relative to other areas of private markets, reflecting strong demand and good asset quality. In six of the last 10 years, infrastructure secondaries have traded above par, and in the last four years, discounts have averaged high-single digits. Although still small relative to private equity, infrastructure secondaries are rapidly becoming a treasure chest for LPs and GPs to access select investments and unlock liquidity potential.

Historical and Projected GP-led Infrastructure Secondary Volumes ($bn)

Case in point: From 2022-2025, the infrastructure secondaries market grew by nearly 10x, expanding to ~$22 billion in 2025 from ~$17 billion the year before and just $2.6 billion in 2022. The biggest driver of this growth has been GP-led transactions. Unlike 15 years ago, investors can now use single-asset deals to access higher-quality, more liquid, capex-intensive assets and recapitalize them for the next phase of growth. And GP-led deals can create strong alignment with new investors while giving existing investors the optionality to maintain their position or take partial to full liquidity.

We believe this market is here to stay and, like private equity, will become a significant driver of infrastructure capital flows. Given the lack of transparency in how these positions price, investors with large primary fund platforms and deep fund and asset data will be best positioned to lead in the secondary market.

Private infrastructure: Thriving in 2026 and beyond

In 2026, we believe infrastructure is poised to continue delivering compelling, long-term upside potential in a global market that has rapidly swung from one macroeconomic or geopolitical event to the other. Scaled platforms with strong relationship capital are in a leading position to help infrastructure investors capitalize on the moment.

Infrastructure: An investment strategy that invests in physical systems involved in the distribution of people, goods, and resources.

Secondary FoF: A fund that purchases existing stakes in private equity funds on the secondary market.

This document has been prepared solely for informational purposes and contains proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this document are requested to maintain the confidentiality of the information contained herein. This document may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which affected markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of 2/18/2026