What you should know:

- Single-manager and multi-manager evergreen funds offer distinct approaches to private market investing.

- In a single-manager fund, a general partner (GP) selects and manages all investments within the fund.

- In a multi-manager fund, a fund manager allocates capital across multiple GPs in the form of co-investments and secondaries. Each GP brings specialized expertise to manage their specific investments.

- Single-manager and multi-manager funds can work together to enhance portfolio composition. A multi-manager fund might serve as a diversified core holding, with single-manager funds acting as strategic satellite investments, complementing and building around the core position.

If you’re a wealth professional interested in private markets, you may have already decided evergreen funds are a compelling choice. These open-ended funds provide diversification and the potential for outperformance. In addition, they're more accessible than traditional private market funds, offering lower minimum investments, simplified paperwork, and greater liquidity.

Among the numerous evergreen fund choices investors have, one major factor that differentiates them is whether they operate as a single-manager or multi-manager fund. Both offer benefits, and they’re often used together in portfolios.

Multi-manager funds are a strong choice for investors as a core exposure to private markets. Single-manager funds are more specialized, making them appropriate as a supplemental private markets investment. For example, a single-manager fund might be a good choice for an investor who wants to invest with a specific GP known for an investment strategy.

Breaking Down the Differences

| Category | Single-Manager Funds | Multi-Manager Funds |

| Fund manager's role | The GP raises capital, selects investments, and operates the portfolio companies. | The fund manager raises capital, selects deals, and invests alongside specialized operating GPs. |

| Fees | Often have simpler fee structures, but that doesn’t necessarily mean these funds have lower fees. Fees vary depending on the fund. | Often negotiate low or no-cost deals, resulting in competitive fees. Each fund varies significantly, and the only way to determine which fees are lower is to compare specific funds. |

| Risk | Risk is concentrated with a single GP, making performance highly dependent on their expertise and market conditions within their niche. | Risk is spread among multiple GPs, reducing the impact of any single GP’s performance. |

| Key advantages | A single GP often possesses deep expertise in a specific strategy, enhancing their ability to outperform benchmarks. These tend to perform well when market conditions align with their approach. | A multi-manager portfolio is diversified across market strategies and can dynamically tilt allocations based on market conditions. |

| Investor fit | Best as a satellite option that provides exposure to a specific fund manager platform. | Best as a core position with broad exposure across strategies, geographies, and GPs. |

Specialization: Focused vs. Broad Expertise

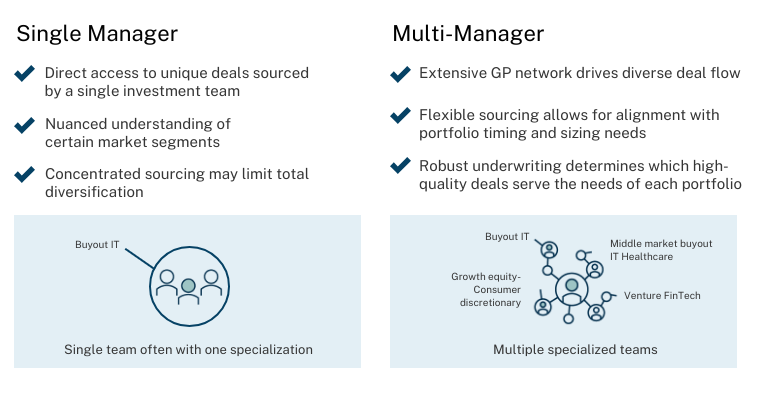

Single-manager funds typically reflect a GP’s established investment strategy, with the GP controlling and operating each portfolio company. These funds often share deals with traditional limited partnerships managed by the same GP.

Multi-manager evergreen funds, offered by investment firms with a proven track record of allocating institutional capital, leverage extensive GP networks to access diverse co-investments and secondaries. This enables them to build diversified portfolios across multiple managers within a single fund.

A Closer Look

Evergreen funds demand a steady stream of high-quality deals while pursuing long-term strategies. Both single-manager and multi-manager funds aim to deliver strong private equity returns, but their approaches differ significantly. Here’s a concise breakdown:

Specialization: Focused vs. Broad Expertise

Single-manager GPs typically focus on specialized strategies, with larger GPs employing dozens of sourcing professionals who are experts in their chosen strategy.

In contrast, a multi-manager approach allows fund managers to cover a broader range of opportunities. Beyond their in-house sourcing teams, these managers often collaborate with thousands of external experts across various strategies. This enables more flexible capital allocation across different vintages and market segments.

For both single-manager and multi-manager funds, the fund manager's quality is paramount. In a single-manager fund, success hinges on the GP’s expertise. In a multi-manager fund, the manager must have strong relationships with top-tier GPs to identify and secure high-quality deals.

Geographic Reach: Local Edge, Global Scope

For investors seeking global exposure, understanding the differences between fund types is crucial. Data shows that general partners (GPs) often outperform when investing in their home regions, where their local market expertise provides a critical edge. For optimal performance in Europe, choosing a European fund manager is vital.

How does this apply to single-manager versus multi-manager funds? Single-manager funds tend to be specialized, and those focused on a single region may be well-suited for investors seeking concentrated regional exposure. The effectiveness of single-manager funds with global exposure, however, will depend on the GP’s regional presence and focus.

In contrast, multi-manager funds include GPs from diverse regions, providing access to multiple regional specialists within a single fund. As a result, multi-manager funds are often the preferred option for investors looking to diversify across multiple geographies.

Portfolio Fit: Core or Satellite?

Choosing between single-manager and multi-manager evergreen funds depends on how you incorporate private market funds within your overall portfolio. It’s not an either/or choice. Single-manager funds may be best for focused satellite investments while multi-manager funds are often ideal for diversified, core investments.

Both fund types benefit from the flexibility of the evergreen model, allowing investors to adjust private market allocations more easily compared to traditional closed-end funds.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable, but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.