What Does Secondary Market Growth Mean for You?

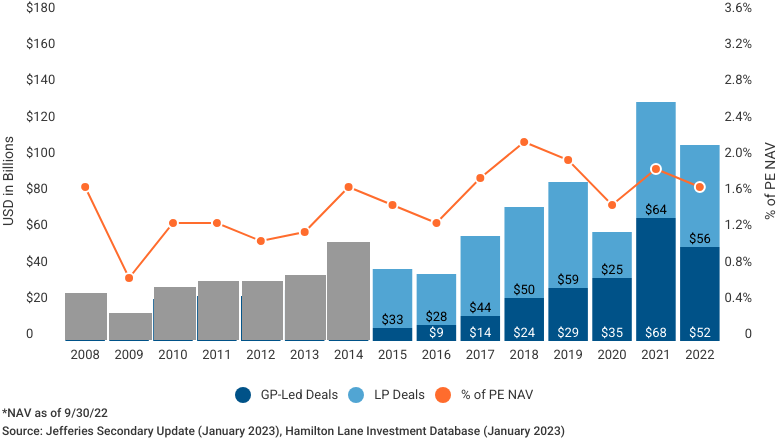

Few corners of private markets can match the recent growth of secondaries. Once the province of distressed sellers and “zombie funds," secondaries now involve the bluest of blue-chip LPs and GPs (see here and here). This evolution has helped annual volume rocket from $20 billion in 2008 to well more than $100 billion in 2021 and 2022.

Secondary Market Volume

And we continue to see the momentum build. In 2022, 50% of LP portfolio transactions involved first-time sellers.1 And as we have noted elsewhere, GPs are increasingly looking to get in on the GP-led secondary action.

So the momentum and traction is there. Against this backdrop, some investors are asking what the secondaries phenomenon means for them. While for others, the question is, “Can I responsibly ignore it?” Let’s revisit why this market has grown, but also explore what it means for investors. As always, we’ll do it with a dash of data.

Secondaries’ Market Share is Rising

Any way you look at it, secondaries’ presence in private markets is growing. Back in 2012, secondary market volume of $25 billion was trivial compared to total private market distributions of $463 billion. That’s only 5% the size. By 2022, however, this figure had risen to 10%. In other words, secondaries’ share of private markets liquidity is rising.

This is logical for several reasons. For one thing, it’s healthy and desirable for a mature asset class to offer investors a liquidity outlet. Liquidity is available within investors’ public stocks and fixed income portfolios, so why not private markets? This makes an asset class more attractive to would-be primary investors. Because increased primary commitments translate to more “inventory” for would-be secondary investors, that can attract more secondary capital and further enhance the viability of that market. A virtuous cycle.

Meanwhile, stigma and unfamiliarity are not the roadblocks they once were. LPs are no longer branded as distressed if they come to market. For GP-leds, “zombie fund” is very often the opposite of the profile for today’s transactions. And LPs and GPs alike continue to see their peers pursuing these transactions and are becoming educated by buyers and intermediaries.

Another factor is hold periods. The long-term trend has been that GPs are holding assets longer – whether in existing fund structures, through continuation funds, or by raising long-dated vehicles. The median hold period for exited private equity investments has risen from 2.9 years in 2002 to 5.6 in 2022. There can be benefits to compounding returns over longer periods under consistent GP ownership, and private markets have been recognizing that. In such a world, it’s only fair for LPs to have more options and influence in generating liquidity when needed.

These are just a few of the forces increasing seller interest – and they are secular trends. In the shorter term, cyclical factors such as the denominator effect and slowed distributions in an uncertain environment provide even more tailwinds.

Secondary Market Secret Sauce: Flexibility

Flexibility and innovation have also been important drivers of secondary market growth. The secondary market excels in this area – in fact, in our 2023 Market Overview we highlight secondaries as “the area of the private markets where the most innovation and creativity is occurring around exits and liquidity options.” Examples include “fund restructurings” a decade ago, strip sales, fund-level preferred capital, and the partial-fund “continuation vehicles” of recent years—to name just a few. The market has also been adaptable, pulling out some tools (and not others) when they fit a given moment. For example, spinout transactions may be prompted by new regulations, tender/staple transactions or annex funds by a tough fundraising environment, and traditional LP secondaries by a widespread denominator effect. This provides more opportunity across a variety of environments.

All of which brings us to one key takeaway: We believe secondary investors should have mandates as flexible as this market. For example, an LP-only fund would have missed out on a good opportunity with GP-leds in late 2020. Similarly, a fund restricted to GP-leds would miss out on many current LP opportunities driven by PE overallocation. Buyers with broad mandates can go where the value is at all times, providing for smoother deployment and a better risk/return profile.

Rising Market Share on the Buy Side, Too – But Still With More Runway

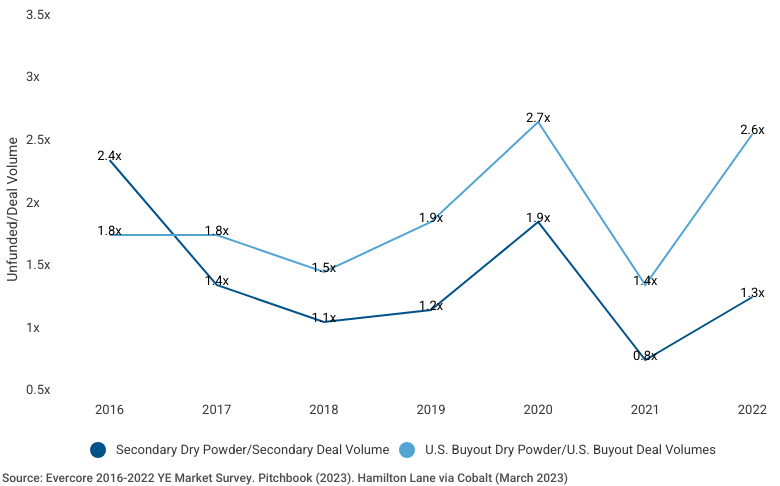

Secondaries’ ascent isn’t limited to the sell-side. Of course, someone must fund the buyers for transactions to happen, and that is starting to play out. From 2018-2022, eight secondary funds raised enough capital to be classified as “Mega” if they had been buyout funds. That figure was zero just one decade earlier (2008-2012). And now the largest secondary fund ($22 billion+) is nearly the same size as the largest buyout fund ($25 billion).

As crazy as it may sound, though, secondaries funds have not raised nearly enough. A good way to see this is in the ratio of dry powder to annual deal volume. As shown below, this ratio has been falling as the denominator (secondary transaction volume) has been rising. 2022 stood at 1.3x, while the same ratio for U.S. buyout funds was 2.6x. That is a striking difference! Simply put, not enough capital is being assembled to match the opportunity in secondaries. And that gives buyers leverage, which has combined with market volatility to

Annual Capital Overhang (Buyout vs. Secondary)

The Case for Strategic Allocation

What does one do when a market is growing and undercapitalized? Invest! Many deep-pocketed investors are clearly taking this view. After all, a $22 billion secondary fund is only possible if there are large investors committed to the asset class. Gone are the days when the typical secondary fund investor was a newly-launched PE program, out for a quick fix on vintage year diversification and the J-curve. Certainly, secondary funds are a good solution for that, and the J-curve-busting discounts are a big selling point. But, as we have pointed out before, most of the returns in secondaries still come from go-forward appreciation.

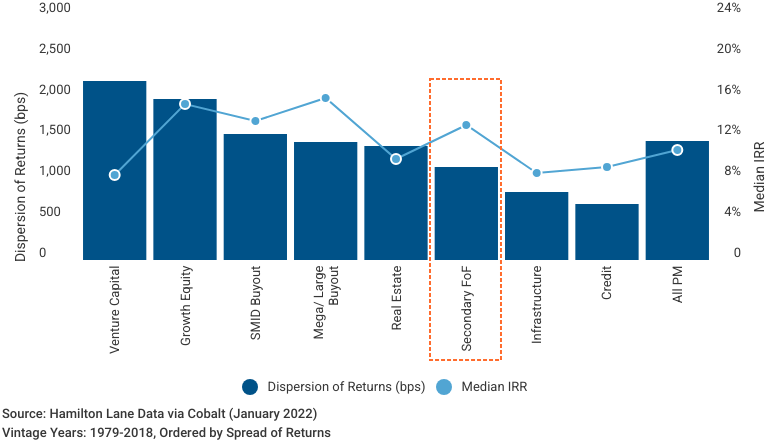

Secondary fund investors have been rewarded to date. As shown below, secondary funds’ IRRs have rivaled those of buyout funds, while dispersion is between that of real estate and infrastructure. Not bad for a risk/return profile! And that’s before considering the accelerated cash flow:

Dispersion of Returns by Strategy

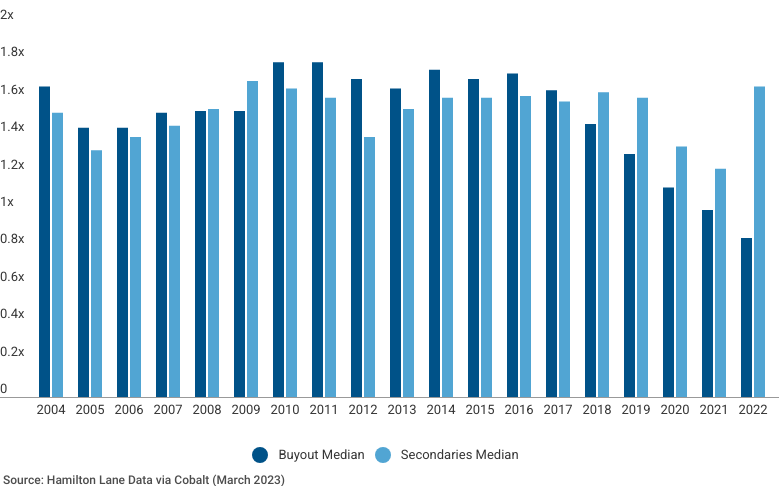

If there has been any knock on secondary performance, it’s that TVPIs have been lower than those of buyout funds. Look at the data, though, and this has arguably been overblown. In the chart below, vintage years 2018-2021 show how entry discounts boost secondary fund performance relative to buyout funds in the early years. Good news for secondaries, and no surprise there. But perhaps more surprising is that when you restrict it to more seasoned funds (2017 and older), secondaries TVPI has only trailed buyout by 0.1x, on average. And secondaries actually exceeded buyout in vintages 2008 and 2009 – a testament to secondaries’ potential upside in volatile market environments.

Median TVPI by Vintage Year: Buyout vs. Secondaries

A gap of only 0.1x is impressive considering the shorter duration of secondaries—which has some benefits. For vintages 2005-2015, the implied average hold for secondary funds has been 0.75 years shorter than that of buyout funds. And secondary funds since vintage 2010 have crossed 0.5x DPI in just 3.6 years, on average, vs. 4.8 for buyout funds. Returning cash early provides LPs with flexibility on redeployment. If that cash has other uses, then it’s available (a positive). But if the investor chooses to roll those proceeds into new secondary funds, then the overall secondary portfolio value can continue to compound, alleviating concerns of a “thin” multiple. Perhaps the TVPI shouldn’t matter so much at the fund level if the investor is thinking at the broader portfolio level.

Secondaries’ share of private markets liquidity and fundraising has been rising for long enough now that it cannot be dismissed as a fad or sideshow. If portfolio construction should reflect market composition, then not having secondaries exposure may increasingly look like a hole. The space has generated strong returns – and liquidity – for investors to date. And if there were ever a time to jump into a new sub-strategy, it’s when it is as undercapitalized as the secondary market is today.

Venture Capital - Venture Capital includes any private markets funds focused on financing startups, early stage, late stage, and emerging companies or a combination of multiple investment stages of startups.

Growth Equity - Any private market fund that focuses on providing growth capital through an equity investment.

SMID Buyout – Any buyout fund smaller than a certain fund size, dependent on the vintage year.

Mega/Large – Any buyout fund larger than a certain fund size that depends on the vintage year.

Real Estate – Any closed-end fund that primarily invests in non-core real estate, excluding separate accounts and joint ventures.

Secondary FOF - A fund that purchases existing stakes in private equity funds on the secondary market.

Infrastructure – An investment strategy that invests in physical systems involved in the distribution of people, goods, and resources.

Credit – This strategy focuses on providing debt capital.

All PM – Hamilton Lane’s definition of “All Private Markets” includes all private commingled funds excluding fund-of-funds, and secondary fund-of-funds.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which is affecting markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot

be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of April 4, 2023