The GP-Led Secondary Market: Scaling with Relationship Capital

Executive Summary

- The GP-led segment of the secondary market is well-positioned to continue experiencing significant growth, driven by both supply and demand tailwinds. This growth trend, playing out in an undercapitalized market defined by high quality and alignment, positions the segment as an attractive investment opportunity for firms that possess both longstanding GP relationships and scaled secondary execution capabilities.

- The GP-led market’s growth trajectory has proven to be resilient irrespective of broader merger and acquisition activity levels. While continuation vehicle (CV) volumes may experience accelerated growth in more challenging liquidity environments, the sub-asset class has developed into an all-weather strategy alongside limited partner interest secondaries.

- The growth and undercapitalization of the GP-led secondary market is attracting potential new entrants and may lead to an evolving competitive landscape, specifically within the single-asset CV segment. However, having preferred access to transactions within the small and middle-market of the GP-led segment will continue to be a key differentiator and determinant of long-term success, as these transactions begin to comprise an even larger percentage of the overall market and should possess greater potential for valuation arbitrage opportunities.

From laying the foundations to raising record deal flow

One of the secondary market’s main growth catalysts over the past decade has been the expansion of the GP-led CV market. These transactions, which offer primary fund limited partners (LPs) secondary market liquidity as a supplement to the proactive selling of entire LP interests, have evolved significantly since their initial emergence over a decade ago. And, similar to the LP interest secondary market, the GP-led segment has fully transitioned into more of an opportunistic market, receiving greater acceptance from both GPs and LPs as a regular portfolio management tool.

Prior to 2016, GP-led transactions were limited to full fund liquidity solutions brought by challenged general partners looking to reset carry terms on underperforming funds and/or obtain additional fees and unfunded capital given their inability to raise new primary funds. That backdrop was not going to be a recipe for long-term success. Fortunately, the GP-led market matured over the subsequent few years, as higher-quality GPs also began utilizing the technology to transparently offer limited partners optional liquidity on older, tail-end funds. However, the real growth potential of the market started to be realized post-COVID, as large-cap sponsors began pursuing both single-asset and multi-asset CV transactions, pulling stronger performing assets out of newer funds. This shift led to the market being viewed, in part, as an alternative to traditional M&A exits and not strictly as a broader portfolio management solution. More recently, high-quality middle-market GPs began following the lead of large-cap sponsors and are now fully embracing these transactions. As a result, the GP-led market has truly emerged as an increasingly diverse, high-growth opportunity set covering the full landscape of private markets net asset value (NAV).

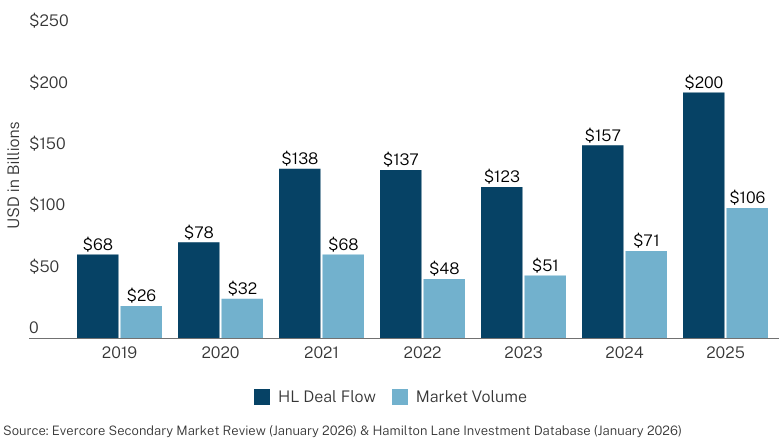

With that trip down memory lane behind us, let’s focus on the current state of the market. Today, GP-led secondary deal volumes represent close to 50% of the overall secondary market and have exhibited a 26% compound annual growth rate (CAGR) since 2019. To put this growth into perspective, GP-led market volume in 2025 has officially eclipsed the total secondary market volume from just three years ago.

The remarkable growth in overall secondary supply fueled in large part by these GP-led transactions has led to a supply/demand imbalance, with the annual secondary capital overhang ratio (i.e., secondary unfunded capital divided by annual transaction volume) sitting near historical lows at approximately 1.0x. This effectively means that secondary buyers barely have enough available capital to cover one year’s worth of trailing market volume. Thus, it is our strong belief that the current growth rate of the GP-led market would be even higher if it were not restricted by what remains an undercapitalized and under-resourced market.

Hamilton Lane continues to see annual GP-led deal flow volumes that are 2x what is actually closing, which we believe speaks to the pent-up supply in the market (and of course, Hamilton Lane’s strong positioning as a preferred strategic partner from the perspective of GPs).

GP-Led Deal Flow & Market Volume

Built to endure market cycles

Market growth and macro trends

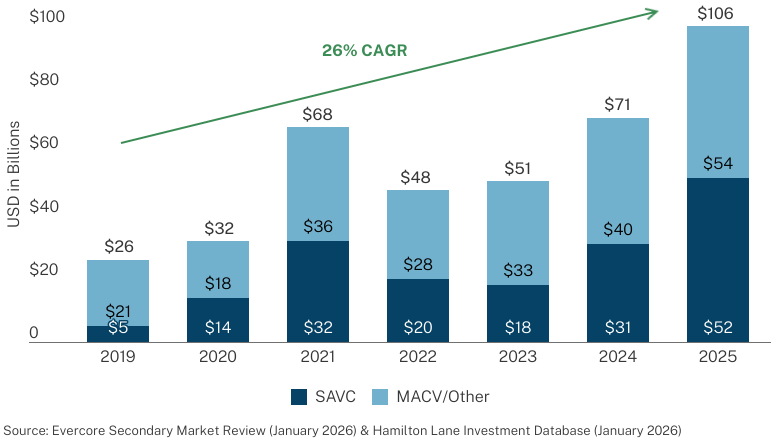

While the entire GP-led market has exhibited strong volume growth since 2019, the most pronounced growth has been seen within the single-asset CV segment. These single-asset transactions have grown at an approximate 48% CAGR since 2019 and have positioned the GP-led market as a viable alternative to traditional M&A sales, not simply as a scaled supplement to LP interest secondaries.

GP-Led Volume

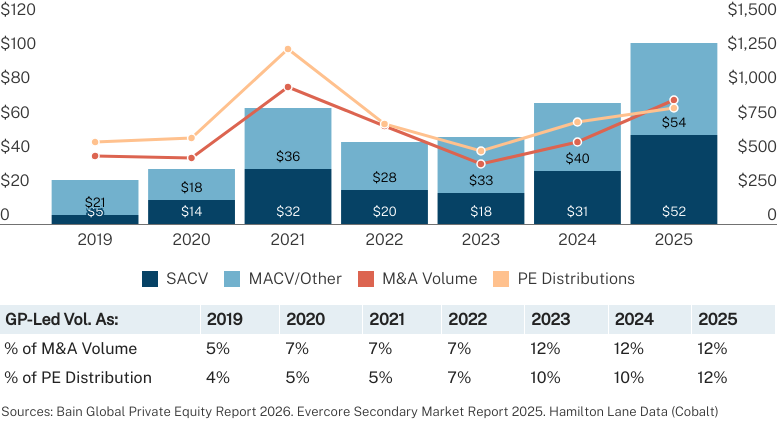

However, with single-asset CVs increasingly being viewed as an alternative to traditional exits, some voices from beyond the trenches of the secondary market are suggesting that the recent growth of the GP-led market is a temporary phenomenon and primarily a function of a weak M&A market. These voices typically reference that over the past four years, CVs have represented an increasing percentage of overall sponsor-backed exit volume and distributions, as illustrated in the chart below.

CV Market vs. Global M&A Volume and PE Distributions ($B)

While these percentages have certainly increased considerably, the increase has mostly been driven by the significant decline in both M&A volumes and LP distributions since the market’s peak of 2021. Looking deeper into the overall GP-led and single-asset continuation vehicle markets, you’ll see that the growth trends from 2022 through 2025 are not materially different from the longer-term growth trends experienced between 2019 and 2025. More importantly, if you focus solely on the 2019 to 2021 period, GP-led market growth was significantly higher than the growth rate of the past three years (38% vs. 31% for overall GP-led volumes and 150% vs. 48% for single-asset continuation vehicles). In fact, the second half of 2021 had been an all-time six-month record for both single-asset CV volumes and M&A volumes until just recently (second half 2025 single-asset volumes set a new six-month record at $33B, compared to $28B in the second half of 2021). All this data suggests that the CV market is well-positioned to exhibit attractive growth rates in both strong and weak M&A markets alike.

Supply and demand drivers

That’s not to say that the weaker exit markets, lower distributions and challenging fundraising backdrop of the past 3+ years haven’t had any positive impact on the CV market, but we believe the recent environment has merely served to enhance pre-existing tailwinds. Similar to what happened in mid-2020 (and what ultimately drove the strong growth in 2021), M&A market uncertainty is the trigger that leads to even more GPs realizing the numerous benefits that continuation vehicles can offer, including:

- Economic benefits: By holding trophy assets longer, GPs can realize significant economic benefits in the form of reinvested and future carry, capturing upside themselves in lieu of transferring this over to competing sponsors (including sponsors which are now trying to masquerade as secondary investors). For companies with a buy and build thesis, additional unfunded capital raised through CV transactions can further enhance these economic benefits for GPs.

- Relationship benefits: Similar to co-investing, high-quality GPs can use CVs to strengthen strategic long-term relationships with their core LPs, providing additional support and momentum for future primary fundraises.

- LP liquidity: The ongoing aging of private markets NAV, combined with declining DPIs across the industry, has LPs gravitating towards GPs which are more creative and flexible as to how they generate liquidity within the context of a traditional commingled fund.

The above benefits, rather than a challenged M&A market, are what’s truly driving the long-term supply tailwinds in the market.

Fortunately, demand tailwinds are now building as well, as the profile of the average CV transaction continues to evolve and become more compelling from the buyers’ perspective. As more LPs recognize the attractiveness of GP-led continuation vehicles as an asset class, we anticipate that buy-side capital will eventually increase as needed to digest the pent-up supply that currently exists in the market.

Increasing buy-side interest will be driven by the following themes:

A high-quality, trophy asset market: The market remains heavily weighted towards high-quality companies backed by high-quality sponsors. Across all continuation vehicle transactions that we reviewed as an existing limited partner between Q4 2022 and Q2 2025, the average realized multiples of cost for selling funds was 4.5x across multi-asset continuation vehicles and 3.9x across single-asset CVs.1

Strong alignment: With attractive performance comes crystalized carry and the ability to craft strong alignment. The average GP commitment to CVs over the past three years has been approximately 9% of total commitments, well in excess of the average GP commitment made to significantly more diversified co-mingled primary funds. Just as important, GPs rolled 100% or more of realized carry proceeds in 88% of deals.

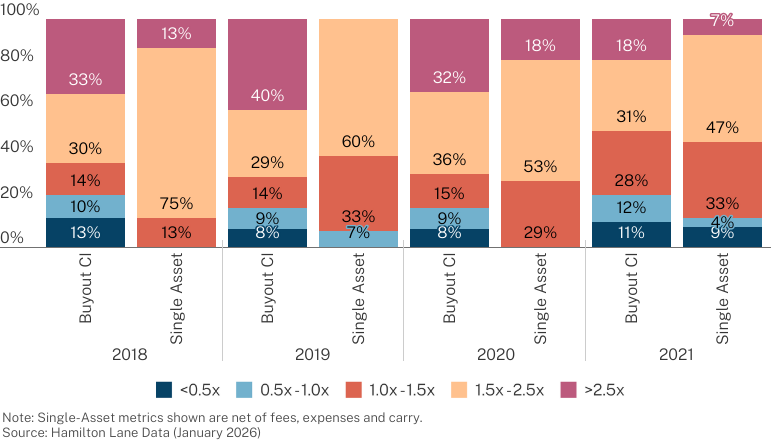

Attractive risk-adjusted performance: As it relates to single-asset continuation vehicles specifically, the focus on high-quality assets with strong existing sponsor alignment and familiarity should, in theory, lead to lower loss ratios and greater early appreciation potential versus traditional buyout deals (where existing shareholders are sellers and ownership change may lead to operational disruption). As shown below, CV performance thus far is proving the lower risk thesis out.

"Co-Investment" vs Single-Asset Continuation Vehicles

Middle-market differentiators

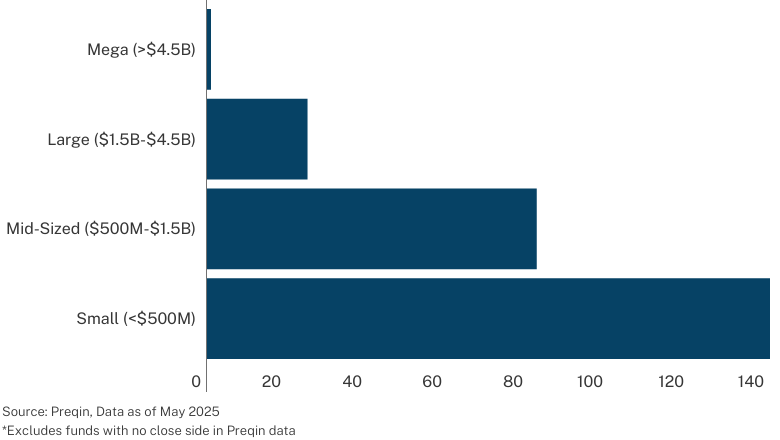

As the GP-led market transitions to one dominated by relationship-oriented, high-quality GPs, secondary firms which are generally viewed as strategic LP capital should continue to benefit from priority access to deal flow. More specifically, secondary firms with small- and middle-market relationships could be best positioned to capitalize on the current GP-led market opportunity given the increasing share of the market that these sponsors now represent.

Number of Continuation Funds* Closed

By Fund Size

And Access to high-quality middle-market deals should provide these secondary firms with some clear competitive advantages:

Differentiation: Traditional primary LPs are recognizing the benefits of investing capital into the CV market. These LPs often possess strong GP relationships, but they generally lack the structuring expertise and team depth to source, lead and negotiate GP-led transactions. So, while there is a good chance that non-traditional secondary investors will increasingly look to invest into GP-led transactions directly, they will need to do so through highly-syndicated, larger CV transactions. And similar to today’s third-party co-investment market, as traditional LPs begin to access larger syndicated deals directly, the large secondary funds leading these deals (and the sub-scale secondary funds playing into these syndicates) may experience some new fundraising challenges. However, secondary firms that focus on difficult-to-access, non-syndicated small and middle-market transactions will continue to offer a strong value proposition to the broader LP universe.

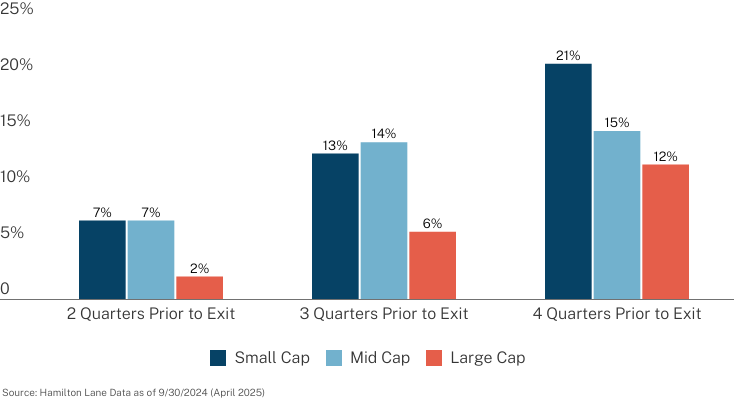

Value arbitrage: Our internal data shows that the median single-asset continuation vehicle was priced at 99.5% between Q4 2022 and Q2 2025.2 With deals being effectively priced at NAV, the potential for secondary valuation arbitrage at entry is tied to the conservatism, or lack thereof, in a GP’s NAV. Historically, small and middle-market GPs have proven to be materially more conservative than larger sponsors, as evidenced by the larger exit uplifts to NAV that they have captured through market cycles.

Median Exit Markups by Fund Size During the Year Prior to Exit

Global Buyout Deals Exited from Q1 2019 - Q2 2024

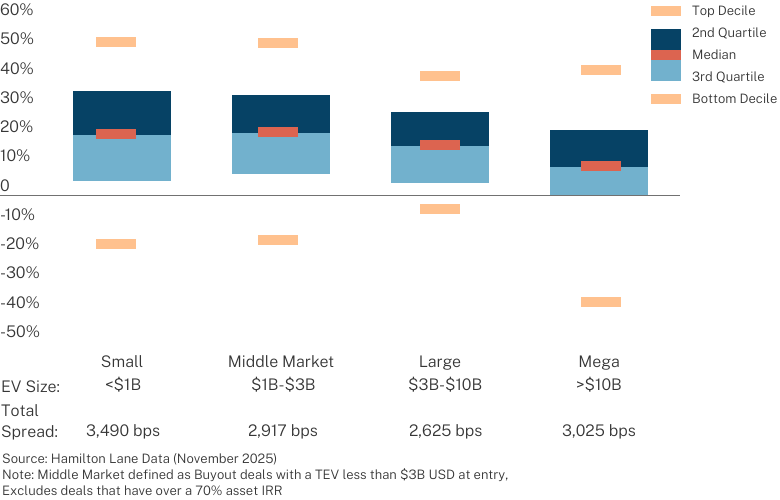

Middle-market historical performance - Small and middle-market private companies are well-positioned to outperform as they tend to i) operate in more fragmented markets (resulting in greater buy and build potential); ii) have more conservative valuation and leverage levels; and iii) have more paths to exit (i.e., not dependent on the public markets).

We reviewed our proprietary database of buyout co-investments since 2003 and found that the median realized gross IRR for small and middle-market buyout deals was 21.1% compared to the average median realized gross IRR of 16.6% for large-cap buyout deals (driven in large part by the 36% greater EBITDA growth seen in small and middle-market deals compared to large-cap deals).

Buyout Spread of Gross IRR by EV

Deal Vintages 2003-2024. Realized Deals Only

Although it’s still early days, research suggests similar outperformance might now be playing out across the CV market. CV deals with fund sizes of $500 million or below (those generally focused on small and middle-market companies) have thus far returned a median net multiple of 1.6x, outperforming CVs with larger fund sizes that have returned 1.4x to date.3

Today, GP market growth is further solidifying the importance of relationship capital in the secondary market. We believe that only the platforms with both secondary market expertise and strong LP/GP relationships – especially in the middle market – may be able to fully capitalize on the supply/demand imbalances and access truly differentiated transactions. Partnering with platforms that possess these attributes can make the difference between hundreds of bps of outperformance potential and getting left behind.

1 Source: Hamilton Lane Proprietary Dataset

2 Source: Hamilton Lane Proprietary Dataset

3 Source: Morgan Stanley PCA - Continuation Fund Performance (October 2025)

Continuation Vehicles: A vehicle in which secondary buyers acquire one or more assets from an existing fund.

Co/Direct Investment Funds: Any PM fund that primarily invests in deals alongside another financial sponsor that is leading the deal.

Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.

Private Equity: A broad term used to describe any fund that offers equity capital to private companies.

This document has been prepared solely for informational purposes and contains proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this document are requested to maintain the confidentiality of the information contained herein. This document may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which affected markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of 2/10/2026