Inflation: We've Seen This Movie Before…Or Have We?

[*movie announcer voice*] “IN A WORLD TODAY WHERE ‘RISK ON’ IS EVERYTHING, VALUATIONS ARE SKY HIGH, AND RATE HIKES LOOM ON THE HORIZON, ONE PRIVATE MARKETS FIRM SETS OUT TO MAKE SENSE OF IT ALL…”

Ok, so that's a bit sensationalized, but in keeping with our movie theme, we were going for maximum dramatic effect. After all, the variables cited are all very real. Risk-on seems to be what the public markets are pricing into valuations today. Signs of relatively positive investor sentiment are showing up in everything from growing allocations toward equities, to private market funds and managers raising capital at a groundbreaking pace, to the record amount of deal volume completed over the last 12 months. So it’s all good, right? Maybe. Then again, it’s tough to ignore the specter of rising interest rates on the horizon. Lurking in the back of most investors’ minds remains a question of how best to prepare for the likelihood of rising interest rates over the medium term. Not only could rate hikes put pressure on real GDP growth, but they also signal potential asset price corrections ahead. (Cue the suspenseful film soundtrack...)

The timing and magnitude of interest rate increases are challenging to predict, especially amid some of the varying economic indicators policy makers must weigh. While the world’s central bankers will want to ensure that global economies do not “overheat,” they must also be mindful of the sensitive economic recovery underway. That’s a delicate balancing act – even in times when there’s not a pandemic variable at play.

Based on all these considerations, the chart below gives a sense of the U.S. Fed’s latest thoughts on potential funds rate increases over the next three years and beyond. Half of officials now expect an uptick in rates sometime in 2022. Broader consensus shows a more meaningful steepening in 2023.

Chart 1: Latest Fed Funds Rate Projections

.png) Source: Bloomberg

Source: Bloomberg

Perhaps making this more perplexing is the fact that we have not lived through an environment like this in quite some time. The question many investors are asking is how best to weatherize portfolios through this period.

But first, a friendly reminder: Don’t overthink the value proposition of the private markets…

Navigating an environment like this starts with developing a broader portfolio construction philosophy and setting asset allocation goals. Let’s start by assessing the decision to make or increase private market allocations. While we are admittedly biased, and without making this too much of a commercial for the asset class, the charts below summarize the core rationale behind growing private market allocation among investors of all shapes and sizes – performance. An actively managed, long-term-focused investment philosophy has outperformed public market equivalents. Take a look at the consistency of outperformance generated historically. The chart below illustrates that at nearly any point over the last 20 years, choosing the trailing 10-year performance of a private market investment strategy would have outperformed public equity benchmarks. The same holds true if you look at performance by vintage – in 19 of the past 20 years, private equity outperforms the benchmark (by the way, the same stat holds true for private credit in terms of 19 out of 20-year outperformance).

Chart 2: Rolling 10-Year Time-Weighted Returns

Chart 3: Buyout IRR vs. PME

And remember it’s also a numbers game…

In the sphere of private companies – there are just more of them. You are talking about tens of thousands of private companies globally with scale – revenue of greater than $100 million – versus a few thousand publicly-listed companies. The private company universe is also growing, whereas the latter has shrunk over the past three decades. The chart below showing the U.S. corporate landscape illustrates this point, showing that nearly 90% of companies generating greater than $100 million of revenue – sizable businesses – are privately owned.

Chart 4: U.S. Public & Private Companies by LLTM Revenue ($M)

At the same time, businesses are staying private longer. For example, as my colleague Blaine Rollins pointed out in a recent Weekly Research Briefing, of the 100+ tech IPOs completed from 2018-2020, the average age of the company pre-IPO was roughly 12 years old. Comparatively, for the period of 1998-2000, that age was just over five years old. The private company landscape is simply more robust and fragmented. Investors that can access the private ecosystem have shown the ability to create outperformance relative to a very efficient – and passively managed – public market realm. On the public side, access and information are equal for all. That’s not necessarily the case when it comes to private investments.

End commercial; now back to our feature film.

The silver lining of growth

The prospect of rising rates and the accompanying potential for a correction to asset prices is a risk that investors must factor into strategy decisions. But we would all do well not to lose sight of the bigger picture and consider these challenges in the context of a healthy growth outlook. Rising interest rates are, in fact, the result of a strong economic recovery that has continued to fuel strong returns over the past 18 months. We continue to experience positive economic growth against a backdrop of a healthcare crisis that is continuing to show signs of improvement and progress. As we discussed in our last piece on inflation, both consumers and businesses are generally in good shape, with healthy balance sheets for both. Not to mention, consensus estimates show that global growth over the next several years is poised to exceed longer-term historical averages. That bodes well for global economies.

Chart 5: Global GDP Growth (% Annualized)

So where should investors go in an environment that will likely demonstrate solid growth but not without some unique challenges (not the least of which is a likely shift upwards in interest rates)? Fear not. Let’s take a page from the Hamilton Lane playbook and ask the data to do the talking:

Private Market Performance in a Rising Rate Environment

What investment areas look interesting in a world where interest rates start to rise again? Roll the tape: the historical data can play back part of that story. While we haven’t navigated an environment like this for quite a long time, the analysis below shows the performance by strategy of funds invested between 1985-2010. It shows how strategy performance varied for those funds actively invested A) During periods of rising rates and B) At all other times during the period (i.e., not a rising rate environment).

Chart 6: U.S. Private Equity During Rate Hikes Median Net IRR

Vintages 1985-2010

So that’s it. All your answers on where to invest in one simple chart. Not so fast, Ricky Bobby. Here’s another place where context is useful. Just like any other asset class, having a relative ‘market weighting’ likely makes sense when considering decisions in an environment like this. Before considering individual strategies, I’d caveat the remainder of this piece with two very fundamental philosophical biases we have toward private markets investing:

1) Do not try to time the market. You will likely lose; it won’t end well; insert your own quasi-apocalyptic result here. Just don’t do it.

2) Just because one investment strategy allocation may appear more interesting today on a relative basis, it doesn’t mean to totally abandon or avoid others. Nor does it mean that other strategies will not have merit. As always, manager, sector and individual deal selection are key elements that must be considered.

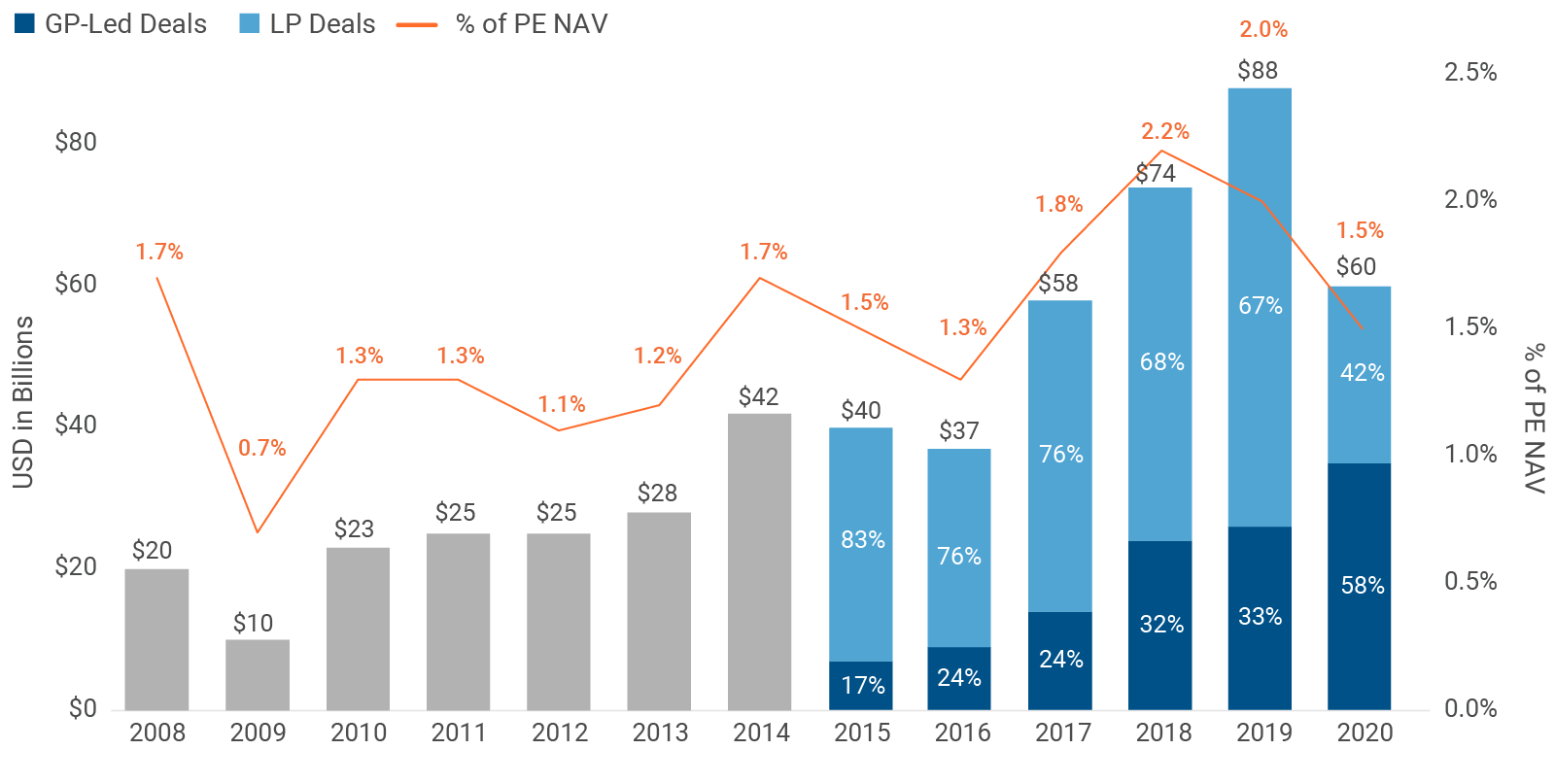

Where are the private markets today? Historical investor choices have created the current NAV footprint shown on the left – largely generated through an era of accommodating monetary policy – whereas the chart on the right provides a glimpse into more recent fundraising trends over the last three years.

Chart 7: Private Markets Industry Allocations

Investors must now consider how to modify exposures in an environment that, quite frankly, we haven’t experienced in quite some time. A pivot to more hawkish policies will certainly have investment strategy implications. Think of the last time central bankers raised interest rates meaningfully and kept them at elevated levels. Or better yet, when was the last time inflation was the primary concern for policy makers driving rates upward? You’d probably need to take a time machine back almost 40 years, to the early 1980s.

For Your Consideration:

Sticking with the theme of ‘things that happened several decades ago which are now coming back into focus,’ let me use some movies of the distant past to introduce some areas for investors to consider. The movies selected – generally from the ‘80s and ‘90s – have all been recreated in recent years (or with new versions coming soon). Just like rising rates now coming back into view, so are remakes and sequels of these “blasts-from-the-past” of the silver screen.

Heighten Focus on Yield and Duration (“The Karate Kid”)

Speaking of things that withstand the test of time, our first strategy area takes inspiration from “The Karate Kid.” The original was introduced in 1984 and tells the story of a new-kid-in-town overcoming adversity and bullies with help from a sage mentor teaching the ancient philosophies of martial arts and life. The story is back in a recent Netflix re-creation, “Cobra Kai” with Johnny Lawrence – the aforementioned bully – now doing the teaching. As far as “ancient philosophies” for investing in a potentially volatile climate; one is to trust the old stalwart of focusing on current yield and shortened duration. As the chart above illustrated, relying on areas like private credit and infrastructure can mitigate downside and deliver relatively strong performance in the face of rising interest rates. (Note for movie buffs: I also recognize there were a few other remakes of “The Karate Kid” starting in the mid-90s, but Cobra Kai is the most recent and has the most original cast members taking another bite of the franchise apple.)

IMDB

Private Credit – Seeking shorter duration exposures can be one way to mitigate some of the risks of a rising rate environment. Private credit and other structured credit-oriented strategies can also take advantage of potentially widening spreads in the face of increased public market volatility. Over 90% of private credit today resides in floating rate securities, most with 1% LIBOR floors, providing potential for upside in a rising rate environment. And with higher rates, it is no surprise that more traditional, long-dated public fixed income/high-yield strategies have been under pressure. Many investors continue to flood into floating rate, syndicated leveraged loans (for example, 2021 is shaping up to be a record year of inflows, largely coming from mutual bond fund and other passive investment vehicles) which has led to continued tightening of pricing and a generally ‘frothy’ syndicated debt market. And while not totally immune from public market tightening, private credit continues to be a popular alternative to these syndicated credit market dynamics. It is also one of the more “nascent” areas of private markets in terms of new and evolving sub-strategies. This has provided investors with more flavors of private credit to choose from and increased optionality post-GFC, with less supply from traditional banking institutions.

Real Assets – Offers similar benefits in terms of yield given the contractual nature of assets and cash flows in most segments of infrastructure and real estate. As shown in the performance chart above, real assets has been a top-performing area given the inflation-linked nature of many investments. For example, most segments of commercial and industrial real estate have built-in inflation escalators generating higher rents and lease rates. Other areas, like apartments and hotels, benefit from frequent (or even daily) repricing capability. Similarly on the infrastructure side, contractual price escalators are usually adjusted on a quarterly or annual basis and tied to CPI or PPI indices. Macro tailwinds and secular shifts such as a multi-trillion-dollar infrastructure spending bill in the U.S. and increasing shift toward renewables globally create additional momentum. Private capital providers play a critical role in fostering these transitions in a more efficient manner. My colleague Brent Burnett describes some of the implications of increased infrastructure spending plans for the private market space.

The Secondary King (“Rocky”)

No, we aren’t talking about a fancy new local consignment shop, but rather one of the more interesting places of evolution within the private markets. The secondary world. What better way to introduce that topic than with a reference to a classic underdog-turned-champion story, “Rocky.” Remember when the secondary market was merely an afterthought of the private markets? Just like Rocky Balboa, the secondary strategy was a lesser-known or appreciated area of the private markets 15 years ago. It was almost considered a “dirty” word, with opportunities only thought to exist if a GP had a troubled fund or bad assets. Not anymore. Today, the strategy represents a core portion of many investor portfolios. Don’t think secondaries are growing in popularity or as a central piece of portfolio construction? On an LTM basis through June 2021, there has been an estimated $90 billion of secondary transaction volume, with 2021 on pace to be a record-setting year. As for the movie, the most recent chapters of this saga have been portrayed in “Creed,” which tells the story of Rocky Balboa becoming the teacher of his talented protégé and the son of his former rival and best friend. The “Creed” remakes with a third installment coming in 2022, are a high-powered reimagining of the original version, just like current aspects of the secondary deal market. Need an example? Look no further than my colleague Dennis Scharf’s recent paper thoughtfully summarizing the fast growing trend around GP-led investment vehicles.

Source: Pocket-lint

One can’t ignore the expanded role that secondary transactions continue to play in investor portfolios. And for good reason. Secondaries offer diversification benefits and the potential for accelerated capital deployment in a differentiated manner. Useful tools in the context of risk, which the data above supports. Specifically, the ability to structure portfolios in a more condensed manner with limited blind pool deployment risk provides investors better visibility in tailoring exposures. All valuable tools as you think about a go-forward environment that will likely generate greater rewards based on manager and strategy selection. As the amount of NAV and private market-focused capital continues to accelerate, so in turn is there more deal volume and opportunity. Even with ballooning secondary transaction volumes, the growing inventory of private market funds has meant that the “turnover” of asset transactions in this context is still a minuscule 1-2% of industry NAV. Like Adonis Creed or Rocky Balboa in the world of boxing, secondaries strategies continue to rise in the rankings within the private market ecosystem.

Chart 8: Secondary Market Volume

Source: Greenhill Secondary Update (January 2021)

Value has its day again (“Top Gun”)

Get out your aviator sunglasses and throw on your leather jacket complete with the fur-lined collar. With a Kenny Loggins-inspired soundtrack to match, in 1986 this movie created an entirely new level of “coolness.” The adventures of Maverick – a cocky, top-tier naval aviator – delivered a wide range of emotions spanning tragedy and triumph. Will Maverick be cool again? We will find out when a remake of this movie is released in 2022 (titled “Top Gun: Maverick,” where Tom Cruise is now the instructor at the famous fighter jet proving grounds).

Source: Mental Floss

Remember when value investments used to be “cool”? Those days seems like the distant past, and as my colleague Christian Kallen said recently of today’s environment, “25x is the new 15x.” With a shift in the direction of interest rates, that seems destined to change. An asset price correction broadly would be welcomed by many GPs, especially as buyout-oriented capital still represents the lion’s share of NAV. Similarly, if I had told you 10 years ago that your buyout fund selections were going to generate mid-to-high-teen net rates of return over the next decade, many investors would have “backed up the truck” to go all-in. That is exactly what they have generated. No one saw that coming. But the relative context compared to growth strategies has made the plain vanilla buyout manager seemingly less appealing. That could change quickly. A confluence of a gradually slowing economic growth outlook, increasing interest rates, and expected reversal of secular trends on tax policy – especially in the developed markets – will add pressure not only to the historical top-line growth trends, but also to the margin and free-cash-flow characteristics of many businesses. This bodes well for value-oriented investors that may see opportunities to purchase assets at a discount to today’s pricing, as well as the ability to apply their operational improvement playbooks.

Back to the performance chart above, risk appetite is a critical factor in assessing allocation in this strategy. The decision will not necessarily be a function of whether buyout / value is a good or bad place to invest, but rather how the strategy performs relative to other options in the chart, that historically, have had more positive performance correlations to rising interest rates. Also, will the landscape change – from a valuation and investment opportunity perspective – to reward leaning into this strategy? Or will returns be ‘lack-luster’ in the face of continued above-historical-trend growth and persistently higher asset prices, in which case, managers may need to adapt their approach?

Don’t throw the baby out with the bathwater – Growth Investments (“The Matrix”)

If “Top Gun” was a test of “cool” in the ‘80s, an instant sci-fi classic was released in the late ‘90s and blew everyone’s mind with its visual and special effects. Enter “The Matrix.” And you thought Keanu Reeves couldn’t top his role as FBI Agent Johnny Utah in the ‘90s classic “Point Break.” Watch the first Matrix movie and the main character Neo dodging bullets and wearing nothing but all black leather. The movie’s release date, and Neo’s awakening from the Matrix, also corresponds with the dot-com boom time era for venture; setting off a new evolution for a ‘growthier’ part of the asset class. Buckle up, the fourth installment of the Matrix saga is scheduled to be released in 2022 as well.

Source: Rotten Tomatoes

VC/Growth strategies have been the darling for investors recently - no other area of the private markets has experienced as much growth in fundraising growth during the past five years. The performance has validated that decision. Just look at the eye-popping returns shown below. As discussed above, the buyout returns look strong until you put them side-by-side in this chart:

Chart 9: Net IRR Performance - Private Market Indexes

But perhaps in this strategy more than the others, investors must weigh their appetite for risk, recognizing that – per the chart above – historically it has performed least well in a rising rate environment. At the same time, dispersion of returns with venture and growth is generally wider compared to other equity-oriented strategies. It may be different this time, but investors must recognize the risk they are taking.

Does that mean this area is most ripe for a correction considering assets that have traded off lofty revenue-oriented multiples in a steepening valuation environment? Maybe. But the post-COVID world has accelerated the transformation of how we all live and use technology in various aspects of our lives. As such, it is hard to envision a world where tech and growth-oriented investments won’t persist given the continued need for innovation and investment. Look no further than the extended supply chain and labor force disruptions that are now creating accelerated corporate investment and capex spending to drive efficiency.

“Top Gun” and the original “Matrix” movie both still hold water when it comes to coolness. Similarly, it is not a zero-sum game in deciding between value and growth allocations. Each continues to have merit even when it may be better to lean more heavily one way depending on the opportunity landscape and the investor’s risk appetite. As always within the venture/growth area, differentiated access to the right sectors, brands and managers is the name of the game.

Conclusion

The environment going forward is likely one that will reward thematic investing and “deal picking” more so than the last decade, where favorable monetary policy has generated continued valuation growth for most major asset classes. There will be greater emphasis on fundamentals, especially profitability. While a relatively decent growth environment will persist through the medium-term, there will also be inflation and rising rates to consider. For investors, this likely creates a greater dispersion of outcomes relative to the previous five years.

What also has investors on edge is that we are potentially moving into an environment that the private markets haven’t really seen before. Think about it, using the 1980s as the relevant context, the private markets as an asset class really didn’t exist during that era. At least not with the magnitude or relevancy with which they exist today. But fear not. Just look at what the last two years have shown us. None of us had ever experienced a pandemic. And at the same time, if I had told you that private market returns during this period would have been some of the best ever generated for the asset class, most people would have been skeptical. But just like a good movie plot twist, the results surprised many of us and perhaps given us all some perspective on the next chapter for our own portfolio construction philosophies.

Strategy Definitions:

Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.

Credit: This strategy focuses on providing debt capital.

Distressed Debt: Includes any PM fund that primarily invests in the debt of distressed companies.

Growth Equity: Any PM fund that focuses on providing growth capital through an equity investment.

Infrastructure: An investment strategy that invests in physical systems involved in the distribution of people, goods, and resources.

Mega/Large Buyout: Any buyout fund larger than a certain fund size that depends on the vintage year.

Natural Resources: An investment strategy that invests in companies involved in the extraction, refinement, or distribution of natural resources.

Origination: Includes any PM fund that focuses primarily on providing debt capital directly to private companies, often using the company’s assets as collateral.

Private Equity: A broad term used to describe any fund that offers equity capital to private companies.

Real Assets: Real Assets includes any PM fund with a strategy of Infrastructure, Natural Resources, or Real Estate.

Real Estate: Any closed-end fund that primarily invests in non-core real estate, excluding separate accounts and joint ventures.

Secondary FoF: A fund that purchases existing stakes in private equity funds on the secondary market.

SMID Buyout: Any buyout fund smaller than a certain fund size, dependent on vintage year.

VC/Growth: Includes all funds with a strategy of venture capital or growth equity.

Index Definitions:

MSCI World Index: The MSCI World Index tracks large and mid-cap equity performance in developed market countries.

S&P 500 Index: The S&P 500 Index tracks 500 largest companies based on market capitalization of companies listed on NYSE or NASDAQ.