A Leading Venture Platform

- Relationship driven deal flow and differentiated insights from 29 years of investing in venture

- Flexible investment strategy with multiple access points to leading companies

- Experience and expertise in structured investments

- Strong competitive position through comprehensive proprietary data and technology tools

Growth companies are staying private longer. Get access through Hamilton Lane’s venture fund.

Backed by three decades of expertise and a robust network of relationships, we believe we have built access to high-quality venture and growth opportunities. Notably, venture and growth comprise nearly 15% of the firm's total assets under management and supervision. Since 2011, we have committed over $4.4 billion to venture capital and growth transactions.* In a space characterized by a wide dispersion of returns, we believe, prioritizing top-tier investments remains essential for achieving success.

*As of March 31, 2025

Why now?

- Accelerating innovation: Innovation drives venture returns and today we are on the cusp of one of the most transformative technological revolutions of our lifetime driven by the development of A.I.

- Private markets dominate growth: Companies are staying private through their most attractive growth phases, which means the best opportunities may not be available via public markets. While there are 501 publicly listed tech companies in the U.S., private markets encompass over 700,000 tech firms*

- Market share expansion: Venture and growth equity have grown from a quarter of private equity net asset value (NAV) in 2010 to over one-third today**, propelled by attractive returns and increased demand for exposure to innovation

- Reduced capital flows: Despite access to an increasingly attractive opportunity set, venture and growth fundraising peaked in 2021***, which we believe has led to a more attractive funding environment for new investors.

*Source: Cobalt, CapIQ, CompTIA 2024 Tech Workforce, U.S. Department of Commerce (January 2025)

**Source: Hamilton Lane Data as of 09/30/2024 (January 2025) “Today” is as of Q3 2024

*** Source: Hamilton Lane data via Cobalt, Pitchbook (as of 9/30/2024)

*The share class performance prior to May 1, 2025 reflects the performance of HL VCGF Holdings LLC and is not direct past performance of the subsequently formed Hamilton Lane Venture Capital and Growth Fund, which became effective on May 1, 2025. Performance is inclusive of annual distribution. Past performance is not a guarantee of future returns. Returns shown net of all fees and expenses. Class R shares are subject to a maximum front-end sales charge of 3.50%. The prospectus contains this and other information about the Fund and is available by calling 888-882-8212. Read carefully before investing. Since Inception of HLVCGF Holdings LLC is September 30, 2024.

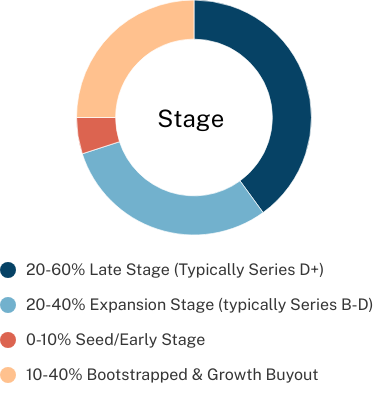

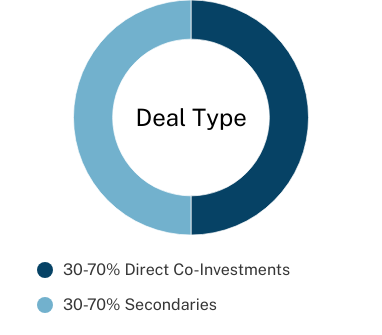

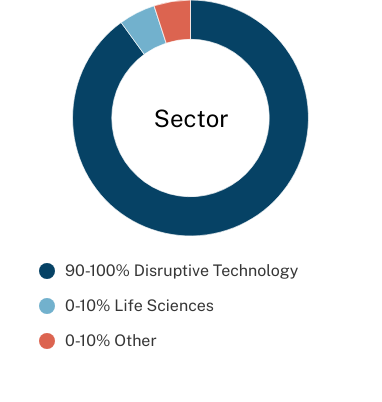

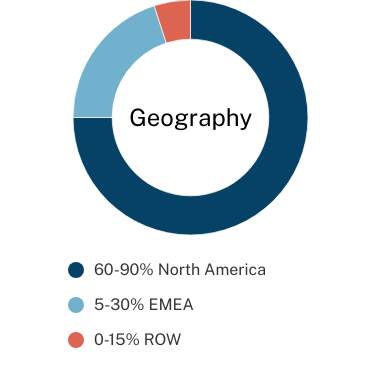

Target Portfolio Construction

For illustrative purposes only. Allocations subject to change without notice.

Related Insights

For previous monthly reports, please visit our archive.

Contact Us

For general inquiries, please reach us at 866-361-1720 or HLEvergreenOps_US@hamiltonlane.com.

IMPORTANT RISK INFORMATION

Investors should carefully consider the investment objectives, risks, charges and expenses of the Hamilton Lane Venture Capital and Growth Fund before investing. The prospectus and, if available, the summary prospectus contain this and other information about the Fund. You may obtain a prospectus and, if available, a summary prospectus by downloading the prospectus or by calling 1 (888) 882-8212. Please read the prospectus carefully before investing.

The Fund operates as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended.

Shares are speculative and illiquid securities involving substantial risk of loss. Shares are not listed on any securities exchange and it is not anticipated that a secondary market for Shares will develop. Shares are subject to substantial restrictions on transferability and resale and may not be transferred or resold except as permitted under the Agreement and Declaration of Trust. Although the Fund may offer to repurchase a limited amount of Shares from time to time, Shares will not be redeemable at a Shareholder's option nor will they be exchangeable for Shares or shares of any other fund. As a result, an investor may not be able to sell or otherwise liquidate Shares. Shares are appropriate only for those investors who can tolerate a high degree of risk and do not require a liquid investment and for whom an investment in the Fund does not constitute a complete investment program. The Fund has no operating history. The Board may elect to repurchase less than the full amount that a Shareholder requests to be repurchased and may under certain circumstances elect to postpone, suspend or terminate an offer to repurchase Shares. An investment in the Fund is considered illiquid.

The Fund may engage in the use of leverage, hedging, and other speculative investment practices that may accelerate losses.

The success of the Fund depends on the identification by, and the availability of suitable investment opportunities to, the Adviser and, with respect to any portfolio funds, the sponsors of such portfolio fund.

The amount of distributions that the Fund may pay, if any, is uncertain. The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors.

Certain investments in the Fund are illiquid making it difficult to sell these securities and possibly requiring the Fund to sell at an unfavorable time or price. The value of certain Fund investments, in particular non-traded investment vehicles, will be difficult to determine and the valuations provided will likely vary from the amounts the Fund would receive upon sale or disposition of its investments.

Non-Diversified Status. Although the Fund is allocated across sectors and asset classes, it is a non-diversified fund and subject to risks associated with concentrated investments in a specific industry or sector and therefore may be subject to greater volatility than a more diversified investment.

General Risks of Venture Capital and Growth Investments. Some of the companies in which venture capital funds invest, directly or indirectly, will not perform as expected. Business risks may be more significant in smaller Portfolio Funds or those that are embarking on a build-up or operating turnaround strategy.

Technology Sector Concentration Risk. The Fund may concentrate its investments in the technology sector without limitation, which can result in significant exposure to specific managers, industries, or companies. While this concentration may enhance potential returns, it also increases the risks of loss and portfolio volatility. The Fund's performance will therefore be more directly affected by developments in the technology sector compared to a more diversified fund. A downturn in this sector could have a greater negative impact. Additionally, Portfolio Funds in which the Fund invests may also concentrate in specific industries, further heightening risks, reducing liquidity, and limiting investment opportunities.

Early-Stage Companies Risk. Early-stage companies may never obtain necessary financing, may rely on untested business plans, may not be successful in developing markets for their products or services, and may remain an insignificant part of their industry, and as such may never be profitable. Stocks of early-stage companies may be less liquid, privately traded and more volatile and speculative than the securities of larger companies.

General Risks of Secondary Investments. The market for secondary investments is inefficient and highly illiquid, and no efficient market is expected to develop during the term of the Fund. There can be no assurance that the Fund will be successful in consummating the types of transactions contemplated, that it will identify or acquire a sufficient number of opportunities consistent with its investment objectives, or that it will obtain such investments on favorable terms. Although the Adviser has identified successful investments in the past, there is no guarantee it will continue to do so.

Risks Pertaining to Investments in Portfolio Funds. The Fund's net asset value may fluctuate due to market conditions, economic factors, and the financial condition and prospects of issuers in which the Portfolio Funds invest. The success of the Fund depends upon the ability of the Portfolio Fund Managers to develop and implement strategies that achieve their investment objectives, and they could materially alter their investment strategies from time to time without notice to the Fund. There can be no assurance that the Portfolio Fund Managers will be able to select or implement successful strategies or achieve their respective investment objectives. Most of the Portfolio Funds are not governed by the1940 Act, and the securities in which the Fund invests or plans to invest will generally be illiquid.

Co-Investment Risks. The Fund’s investment portfolio will include co-investments, which are indirect investments in the equity of private companies, alongside private equity funds and other private equity firms via special purpose vehicles. There can be no assurance that the Fund will be given co-investment opportunities, or that any specific co-investment offered to the Fund would be appropriate or attractive to the Fund in the Adviser’s judgment.

An investment in the Funds are generally subject to market risk, including the loss of the entire principal amount invested. An investment in the Funds represents an indirect investment in the securities owned by the Funds. No guarantee or representation is made that the investment program of the Fund will be successful, that the various Venture and Growth Investments selected will produce positive returns, or that the Fund will achieve its investment objective. For a complete description of the Fund’s principal investment risks, please refer to the prospectus.

Diversification does not guarantee a profit or protect against loss in a declining market.

Distribution Services Inc, LLC is the distributor of the Hamilton Lane Venture Capital and Growth Fund. Hamilton Lane Advisors, LLC is the investment adviser to the Hamilton Lane Venture Capital and Growth Fund. Distribution Services Inc, LLC is not affiliated with Hamilton Lane Advisors, LLC. Learn more about Distribution Services Inc, LLC at FINRA' BrokerCheck.

HMLAN-4813456-09/25