Weekly Research Briefing: Finding Liquidity

February usually brings us frozen lakes, fountains, and birdbaths. There is little frozen water happening this week unless maybe you live in the remote woods of northern Maine. Even natural gas prices are trading at multi-decade lows as global winter reserves have barely been touched this season. Great news for northern hemisphere homeowners. Bad news for ice climbers and pond hockey players.

Today's financial markets are also operating in a world that is less and less frozen every day. As you look at the news across the tape, in any newspaper or on any financial news network, you will see a system getting more liquid every day. This is a very good thing. Companies are borrowing at even tighter spreads as private lenders and banks compete for their business. The M&A train has left the station and is picking up speed as companies want to buy and sell assets. Wall Street strategists are lifting their S&P 500 price targets (UBS to 5,400 and GS to 5,200 just today) as earnings outlook continues to improve. Companies and financiers continue to liquify their balance sheets and portfolios as assets that were frozen on balance sheets during COVID, or the Fed's Hike-o-Rama become transactional and financeable with others. Even commercial real estate is moving. It might be trading at 50 cents on the dollar, but at least it is moving. All this liquidity is good. It will help the markets digest their problem assets and buoy the values of the best assets.

Looking back at last week's data, the CPI and PPI came in hot. You can blame the seasonal adjustments or the lagging OER and shelter inflation components, but at the end of the day, the data needs to move lower for the Fed to act on lowering rates. Meanwhile, the Empire Fed, Philly Fed and NAHB (homebuilder) survey numbers came in better than expected which will not make the FOMC's job any easier. January retail sales figures did come in very weak as the mid-month freeze hit many brick and mortar stores hard. But the University of Michigan Consumer Sentiment continued to move higher with those surveyed seeing more car buying and less worries of job losses in their future.

For this holiday shortened week, expect little economic data while all eyes turn to NVIDIA's Wednesday afternoon earnings. Good luck to the analysts covering the stock. No pressure, but the fate of the markets might rest on this number. Just kidding. Or not? Have a great week everyone.

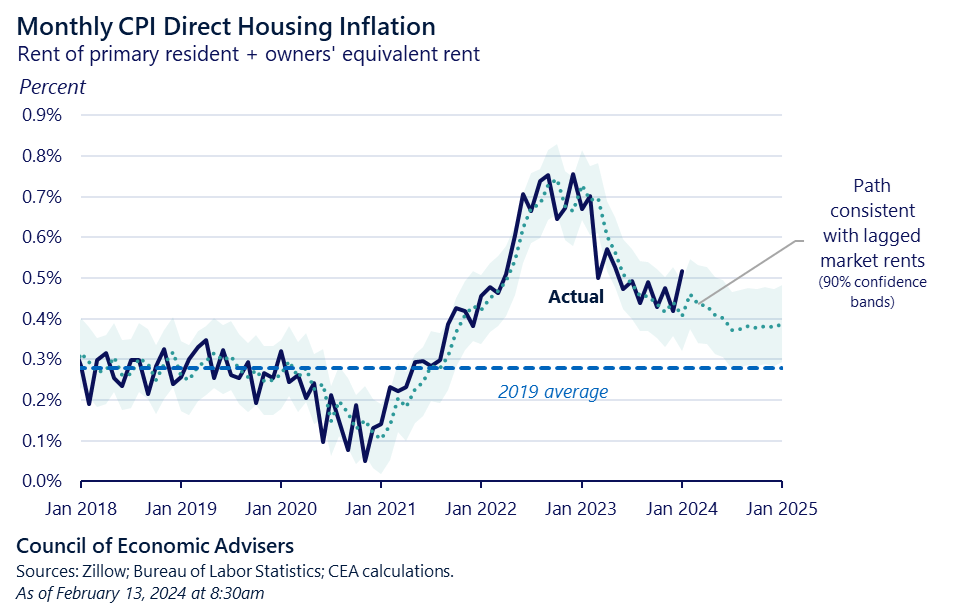

The song remains the same when looking at the CPI figures last week: Housing costs have yet to break...

@WhiteHouseCEA: Housing prices increased 0.5% in January, a tick above December’s rate. As CEA discussed in a blog post, CPI housing inflation has generally declined with lagged market rent inflation. But lately, it has remained elevated.

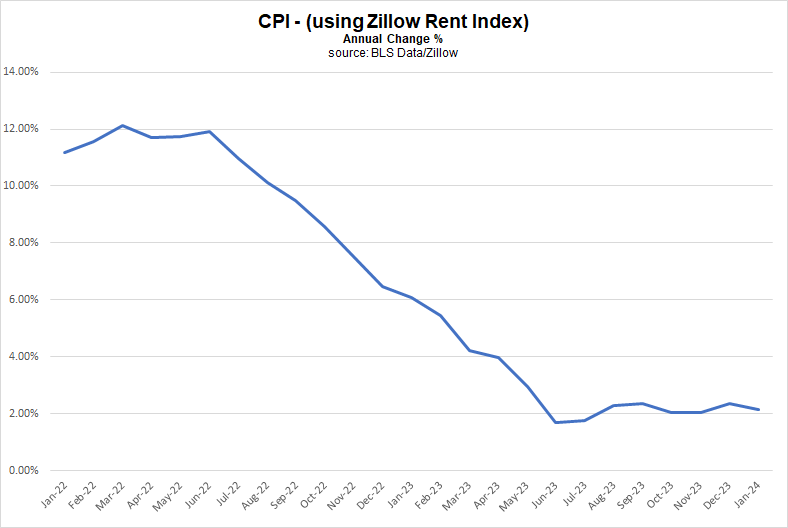

If only the BLS would use the Zillow rental index, we could move on and complain about something else...

@wabuffo: Here's what y-o-y CPI monthly readings would've been if one plugged in Zillow's data instead of the BLS's for shelter inflation. We've been at 2% since June. Fed shoulda cut already.

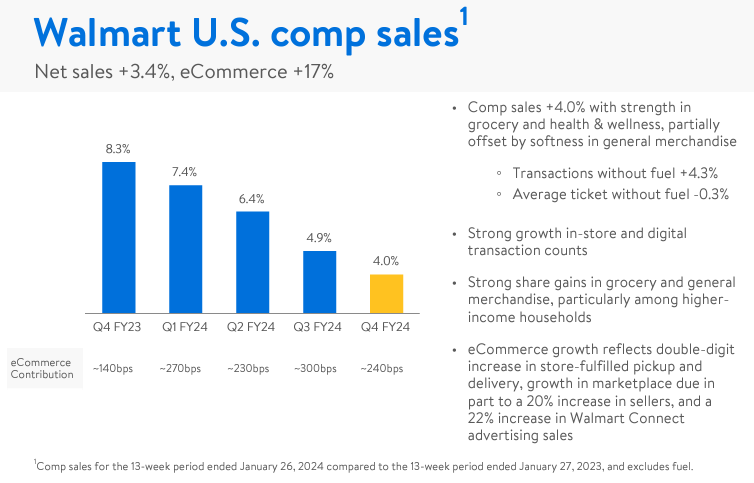

Today's Walmart call showed price deflation occurring across the store but the CEO wanted even more...

Chief executive Doug McMillon said in November that the world’s largest retailer could find itself “managing a period of deflation” in early 2024, in a potentially encouraging sign for the broader economy given Walmart’s reputation as a consumer bellwether.

McMillon said on Tuesday that Walmart’s general merchandise category in its US operations was “there” in terms of a “deflationary position”, but in the three months to January, “the slope of the decline softened”.

Prices are lower than a year ago, he told analysts, “but not as much as the trendline would have suggested” at the end of the preceding quarter. Prices for food and consumables were “slightly higher than a year ago”, he added...

“Our general merchandise prices are lower than a year ago, even two years ago in some categories,” McMillon said. Prices for eggs, apples and deli snacks have fallen from 12 months ago, but the likes of asparagus, blackberries, paper goods and cleaning supplies were up.

Mimicking Walmart, Kraft Heinz brand product prices are slowing rapidly but have not yet gone negative on a year over year basis...

@knowledge_vital: $KHC - Disinflationary data point of the morning: Kraft's North America prices rose +2.5% in Q4, a large drop from +5.8% in Q3 and +9.4% in Q2.

Working against falling consumer goods prices are rising air travel luggage fees...

Now who wants to help me lift my 100-pound carry-on bag into the overhead rack?

American Airlines will now charge $40 to check a bag at the airport for domestic flights or $35 for those who pay in advance online. Previously, the airline charged $30 for the first checked bag. A second bag will now cost $45, up from $40.

The price increase follows similar bumps at other airlines. Alaska Airlines raised the charge by $5 early this year to $35 for a first checked bag and $45 for a second. JetBlue Airways this month started charging $45 to check a bag at the airport, with a $10 discount for paying in advance.

Scott Chandler, American’s senior vice president of revenue management and loyalty, said Tuesday that the fee increase was driven by inflation as airlines have been battling rising costs for fuel and labor...

The rising fees can also help steer travelers into airline loyalty programs or toward pricier premium tickets that still include baggage fees. At American, for example, customers with the airline’s co-branded credit card or who have status will still receive complimentary bags, as will those who buy seats in premium cabins.

Chandler said less than half of American’s customers check bags, and most don’t pay for them. One reason: The airline has been adding bigger bins to its planes that can accommodate more carry-ons.

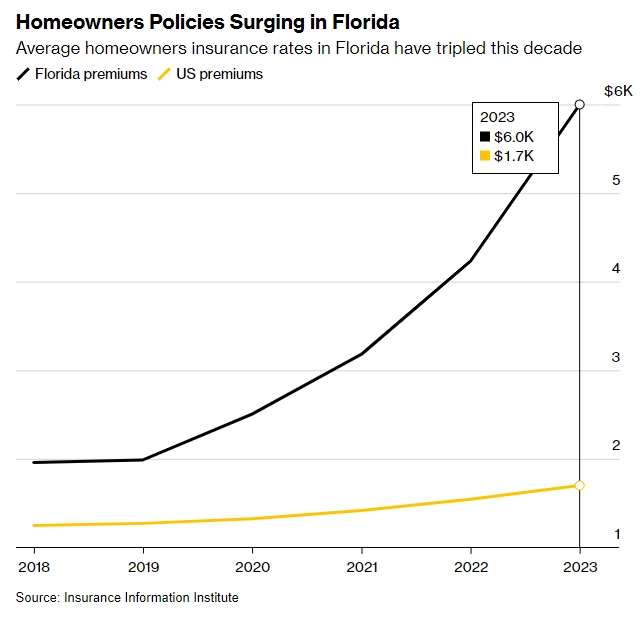

Florida residents are getting an extra set of inflation figures to worry about which is now affecting home prices...

Florida’s southwestern coast — long one of America’s fastest-growing regions — is losing some of its boomtown swagger as a home-insurance crisis and other soaring costs make homes unaffordable.

Homeowners from Sarasota south to Naples, known for its eight-figure waterfront mansions, are having a tougher time selling their properties, and the buildup in inventory has caused home prices to fall at some of the fastest rates in the nation. Realtors point to rising insurance costs that were exacerbated by Hurricane Ian in 2022, prompting some homeowners to list their homes for sale and would-be buyers to walk.

“You’ve got people that went through the storm and just want to move on, and don’t really think the affordability is here anymore because of insurance,” said Marlissa Gervasoni, president of the Royal Palm Coast Realtor Association. “From what I’m seeing, I believe they are looking for areas that might be less costly.”

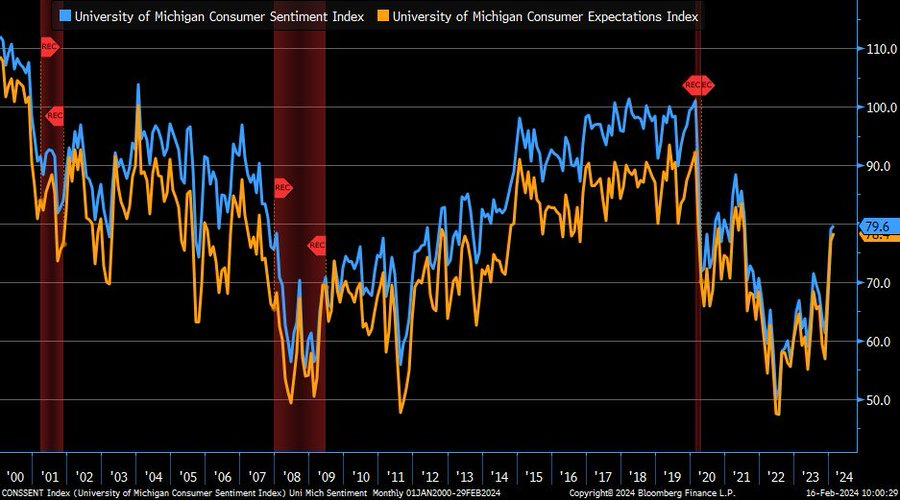

Consumers are continuing to feel better and better...

@LizAnnSonders: February @UMich Consumer Sentiment Index (blue) up to 79.6 vs. 80 est. & 79 in prior month … expectations component (orange) rose as well, up to 78.4 vs. 77.1 prior

Walmart's figures today gave us some good insight into the U.S. economy...

+4% comp store sales on top of a +8.3% a year ago is a good stack of numbers. Average ticket of -0.3% shows deflation setting into the customer's basket. The number of transactions was +4.3% so customers are shopping more often.

Home Depot also posted numbers today which showed just how difficult January's weather hit...

@conorsen: To show how much January weather impacted the economy, Home Depot US company comps by month: November: -2.7%, December: +0.6%, January: -9.1%.

Of course, bad weather for Home Depot is good weather for auto parts retailers...

@TheTranscript_: O’Reilly Automotive CEO: "As we progressed through Q4, results remained relatively consistent from a volume perspective, with each month performing better than our guidance expectations… We are off to a solid start in 2024, aided by favorable winter weather in January.."

In other earnings tidbits. Med-tech giant Medtronic confirms the rebound in hospital procedures...

@TheTranscript_: Medtronic CEO: "We had a strong finish to our fiscal year....Our accelerating revenue growth was broad-based, driven by procedure volume recovery, supply improvements, and innovative product introductions"

Also, positive comments from Wendy's, Coca-Cola and Applied Materials...

"Why do we believe this economy is doing pretty well? We are basically in full employment. Grocery inflation is coming down. So quarter versus quarter the consumer should start to see net disposable income coming up slightly, feel a little bit richer, and feel a little bit like, yes, what I can treat myself and come a little bit more often into the restaurant." - The Wendy's CFO Gunther Plosch

"In North America, consumer spending in aggregate is holding up well"... "Another important fact that I highlight is the inflationary pressures, which are moderating or stabilizing across most of our markets." - Coca-Cola CEO James Quincey

"In our discussions with customers, we're hearing that overall market dynamics are improving. There is a reacceleration of capital investment by cloud companies, fab utilization is increasing across all device types & memory inventory levels are normalizing" - Applied Materials President & CEO Gary E. Dickerson

In its annual report, semiconductor chip equipment manufacturer ASML calls the bottom...

Given their very high-end position in the advanced semi food chain, it is a good idea to listen closely to what they are saying.

ASML Holding NV said the semiconductor market has reached its nadir and there are now are signs of a rebound.

“We believe that the market has now reached the lowest point of the dip,” ASML Chief Financial Officer Roger Dassen said in comments in the company’s 2023 annual report published on Wednesday. “Although we cannot predict the exact nature of the slope ahead, the recovery is nascent.”

ASML is the world’s top maker of lithography systems, machines that perform a crucial step in the process of creating semiconductors. The demand for its products is a bellwether for the industry, even as chipmakers including Intel Corp., Texas instruments Inc. and Infineon Technologies AG have warned of subdued sales this year.

The Veldhoven-based company is the only producer of extreme ultraviolet lithography machines that are used by Taiwan Semiconductor Manufacturing Co., Samsung Electronics Co. and Intel for the most advanced fabrication. The equipment prints patterns of transistors onto silicon wafers, which are then sliced into individual chips...

“The longer-term trends are unmistakable,” Dassen said, citing artificial intelligence, electrification and the energy transition as boons to ASML’s business.

If you want to see some positive liquidity, just look at Monday's list of stocks hitting all-time new highs across multiple industries...

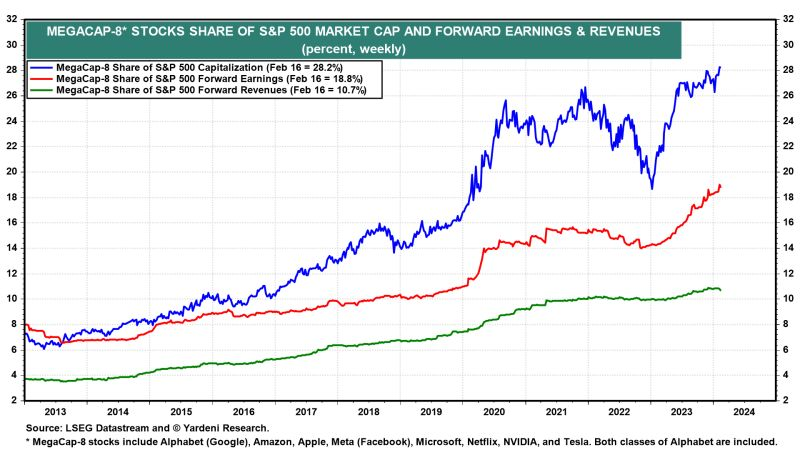

Lots of criticism for the largest stocks in the market, but guess where the sales and earnings growth is coming from...

@GunjanJS: Goldman: "The 4Q earnings season also highlighted the ongoing fundamental strength of the mega-cap 'Magnificent 7' stocks". If NVDA reports estimates in line with consensus, the Magnificent 7 will have grown sales by 15% YoY and lifted margins by 582 bp YoY, leading to 58% earnings growth

@yardeni

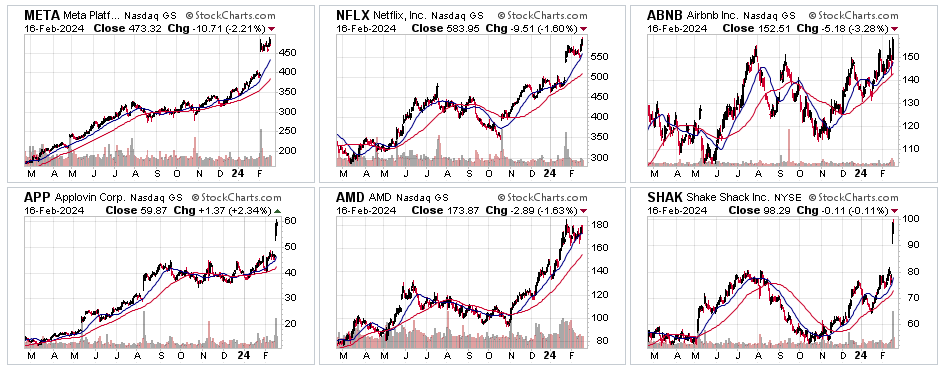

Several other high growth companies in the market are also seeing their stocks launch up and to the right...

I see social media, media, leisure, mobile apps, semiconductors, and a restaurant all breaking out. No doubt this will get the high growth venture cap and investment bankers back to the offices.

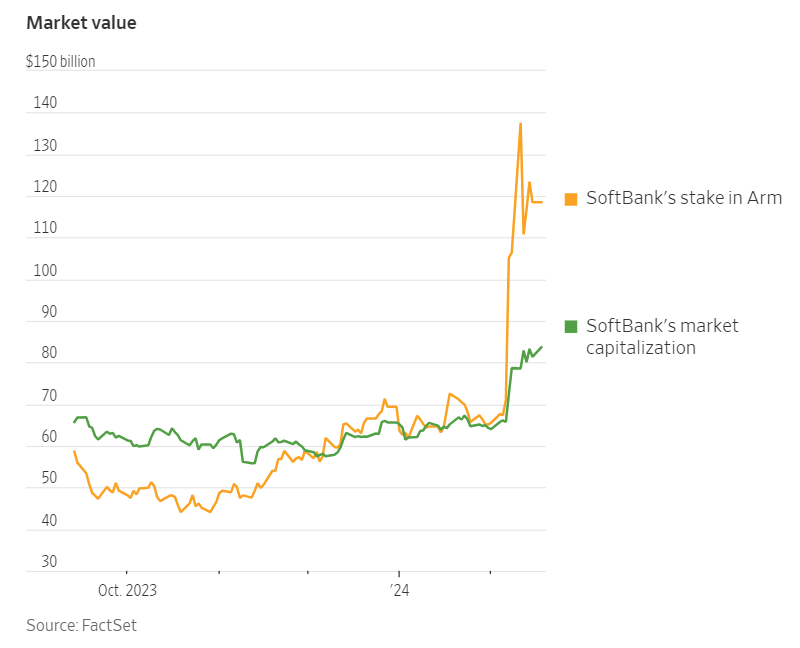

Excitement in technology investing has created an interesting situation at SoftBank...

SoftBank owns 90% of Arm Holdings. This stake in ARM is now worth almost 150% of the value of SoftBank. Let's now watch how this arbitrage fixes itself.

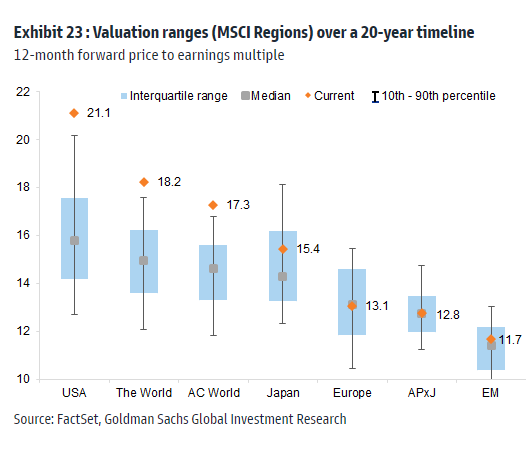

Quickly rising liquidity has mostly benefitted the U.S. equity market...

The non-U.S. equity valuations still look rather average versus the past 20 years.

Goldman Sachs

Liquidity in action: One of the biggest M&A deals of 2024 hits the weekend tape...

It might be a for stock deal, but it is still a mega-deal among two of the biggest players in credit card issuance and processing.

Capital One said it will buy Discover Financial Services for more than $35 billion, a deal that will marry two of the largest credit-card companies in the U.S.

Under the terms of the all-stock deal, Discover shareholders are set to receive 1.0192 Capital One shares for each Discover share, representing a premium of about 27% based on Discover’s closing price Friday. After the deal closes, Capital One shareholders will hold roughly 60% of the combined company, with Discover shareholders owning the rest.

Capital One is making a big bet at a booming time in the credit-card sector. More consumers are moving from paying with cash to cards as a result of generous rewards programs and the digitization of commerce—a transition that accelerated with the pandemic. A recent increase in credit-card debt has provided a further boost to issuers.

Buying Discover would give Capital One, a credit-card lender with a market value of a little over $52 billion, a network that would vastly increase its power in the payments ecosystem...

An acquisition of Discover will rank among the biggest deals so far in 2024. After a lull in M&A activity in 2023 as economic and other uncertainty and increased interest rates took a bite out of the appetite for deals, volumes have gotten off to a relatively strong start and are up 90% in the U.S. compared with a year earlier, according to Dealogic. Other big transactions include software maker Synopsys’ roughly $35 billion acquisition of rival Ansys and Diamondback Energy’s $25 billion deal for Endeavor Energy.

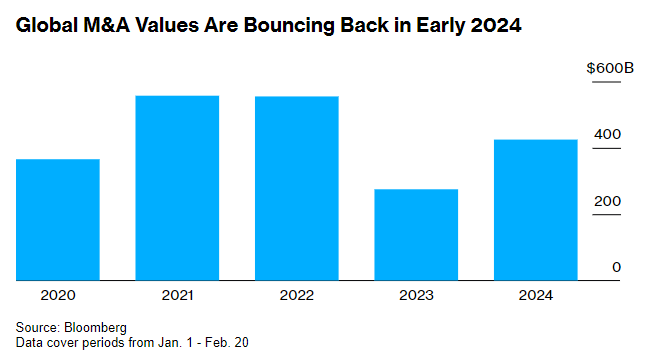

Global M&A activity is now bouncing off a trampoline...

The US is leading a revival in global mergers and acquisitions that many dealmakers didn’t think would emerge until later in the year.

The latest big transactions in the country are led by Capital One Financial Corp.’s $35 billion offer to buy Discover Financial Services. Elsewhere, Truist Financial Corp. is selling its insurance brokerage business in a deal valuing the asset at $15.5 billion and Walmart Inc. has agreed to acquire smart-TV maker Vizio Holding Corp. for about $2.3 billion.

These take the value of deals announced globally this year to roughly $425 billion, according to data compiled by Bloomberg — a figure that’s up 55% on this point in 2023.

This is good news for dealmakers working hard to put two consecutive years of falling values behind them. The end of the interest rate-hiking cycle is creating more certainty around valuations, while rising equity markets are providing buyers with extra financial firepower for acquisitions; more than half of the 10 biggest deals announced this year are being financed at least in part by stock.

Also, the largest European private to private transaction for 2024 has just been announced...

TPG Inc. has emerged as the highest bidder for Alter Domus, the fund administration company backed by Permira, in what’s set to be one of the biggest European private equity deals this year, according to people familiar with the matter.

The buyout firm is competing with rival suitors Hellman & Friedman and Cinven to acquire the business, the people said, asking not to be identified because the information is private. A transaction could value Alter Domus at about €4.5 billion ($4.9 billion), the people said...

Alter Domus handles administrative and compliance issues — including cash management and know-your-customer requirements — for private equity and other alternative investment firms. The company, founded in 2003, has about $2.2 trillion under administration.

And another mega-deal is in the works over in Europe...

Some of the world’s largest buyout firms, including Advent International and Blackstone Group Inc., are circling the consumer health division of French pharmaceutical giant Sanofi ahead of a potential separation of the business, according to people familiar with the matter.

The business is also drawing early interest from Bain Capital, CVC Capital Partners, EQT AB and KKR & Co., the people said, asking not to be identified as the matter is private. The unit could be valued at about $20 billion in any deal, they said.

Sanofi said in October that it plans to separate the division, which sells over-the-counter products including Phytoxil cough syrups and Icy Hot pain relief gels. Advisers to the Paris-based drugmaker have communicated that it’s open to a sale of the consumer health business if it can achieve its desired valuation, the people said.

Shares of Sanofi jumped as much as 3.2% in Paris trading Tuesday, the biggest intraday gain in nearly four months. They were up 1.9% at 4:57 p.m. in the French capital, giving the company a market value of about €111 billion ($120 billion).

One more transaction in the private equity world for a ten-figure deal...

KKR & Co. has agreed to acquire a stake in Cotiviti from private-equity manager Veritas Capital in a deal valuing the healthcare-technology business at around $11 billion.

The transaction would give the two New York-based firms equal ownership stakes in Cotiviti, according to an announcement planned for Wednesday. The Wall Street Journal reported in December that the firms were in discussions.

The deal would rank among the largest recent private-equity transactions. Buyout firms slowed dealmaking after the Federal Reserve began raising interest rates in 2022, with the debt used to finance acquisitions getting more expensive and harder to obtain.

The deal would also represent a significant payday for Veritas, which took Cotiviti private for about $4.16 billion in 2018. The firm specializes in buyouts of companies at the intersection of technology and government.

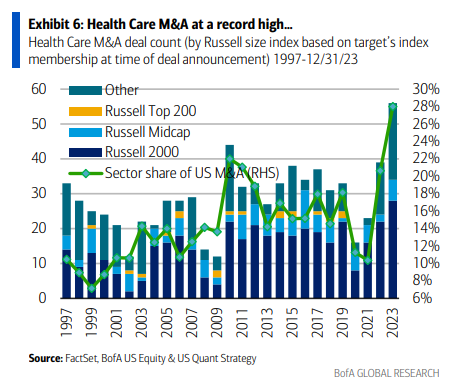

Speaking of Health Care M&A, no slowdown for those bankers and lawyers the last two years...

BofA Global

In another sign of a very healthy and liquid market...

GE sells $1.1 billion of GE Healthcare in a Thursday afternoon drive-by that lifts both GEHC and GE on Friday.

@wallstengine: $GE announces a secondary offering of 13M shares in GE HealthCare Technologies $GEHC, aiming to exchange shares for debt held by Morgan Stanley. This move will reduce GE's stake, currently standing at 13.5% with ~61.6M shares.

Overflowing swimming pools full of cash flow at IHG which will be returned to shareholders...

+16% REVPAR in 2023 led to a doubling in profits. So, with more than enough to fund new property growth, IHG is going to hike the dividend and buyback 10% of its market cap. You can guess the same liquidity problems are happening at other large hotel owners.

InterContinental Hotels Group said it expects to return up to $1 billion to shareholders via a share buyback program and dividends as its hotels and resorts growth strategy pays off.

The owner of the Crowne Plaza and Holiday Inn hotel brands said strong cash generation was supporting investment in growth initiatives, and that it was launching a share buyback program of up to $800 million for this year. It lifted its final dividend to 104 cents from 94.5 cents the year prior, taking the full dividend for the year to 152.3 cents.

The planned shareholder returns are equivalent to 10% of its $10 billion market capitalization at the start of 2023, IHG said.

IHG said it opened 31 hotels last year and that it was expanding its presence in markets such as China, where it already has 700 hotels open, with 500 more in the pipeline. In India it has 46 hotels up and running, with 49 more in the pipeline, while in Saudi Arabia it plans to add to its 49 existing hotels with 39 more.

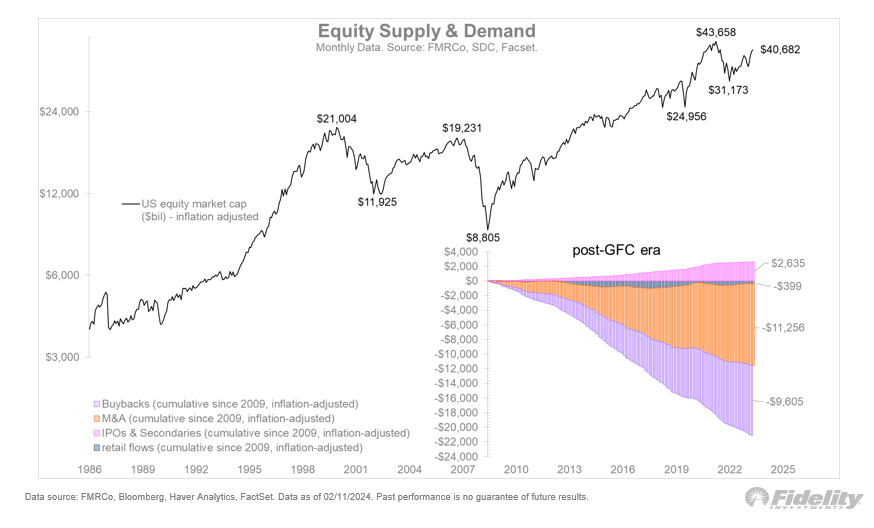

Speaking of massive buybacks, here is a great chart of the cumulative shrinkage in the amount of equity supply since the GFC...

@TimmerFidelity: Below I show the same thing but cumulatively since the Global Financial Crisis. The supply of public equities has been $2.6 trillion, and the demand has been almost $21 trillion. It’s a stunning feat and goes a long way to explaining the market’s $41 trillion valuation.

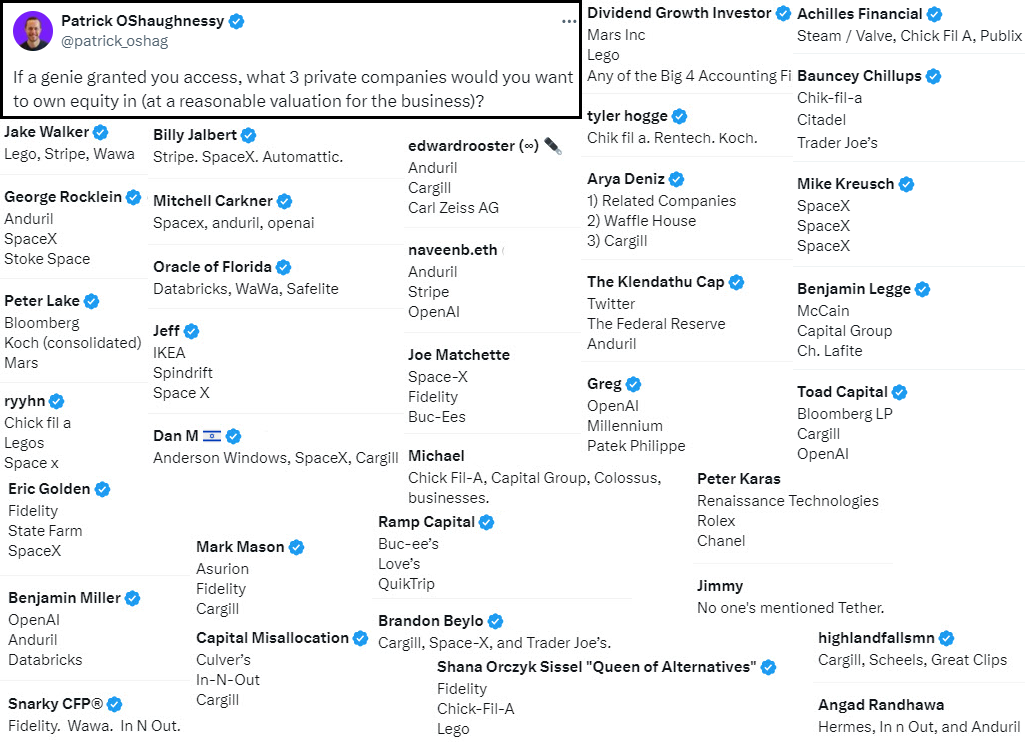

If you could buy any 3 private companies, what would they be?

Here is a good sample of answers from FinTwit. Lots of repeated names. Many names that you could already own if you have exposure to PE funds directly or indirectly (like thru your pension plan).

As I wrote earlier, the credit spread collapse is allowing all companies to borrow at very tight levels...

Ares Management Corp. is leading a $3.3 billion private credit loan for UK insurance broker Ardonagh Group Ltd., with the debt’s pricing among the lowest seen in direct lending, people with knowledge of the matter said.

Ardonagh’s loan is set to price at 475 basis points over a US reference rate, the people said, asking not to be identified. That would make it among the cheapest private credit deals on record, according to data compiled by Bloomberg. Goldman Sachs Group Inc.’s asset management division is also a significant lender, the people said.

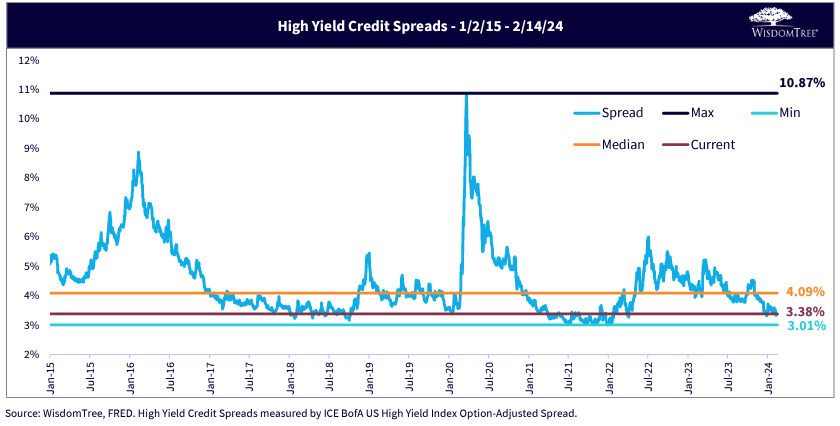

Checking in on 10-year high yield spreads shows you just how low the current spreads are versus the last ten years...

Wisdom Tree

The flood of liquidity is helping everything...

The wave of money making its way into the credit market is acting as a shield for investors against every negative scenario - even the prospect of ever-fewer central bank cuts this year.

Risk premiums on high-grade and junk bonds fell Tuesday despite hotter-than-expected US consumer-price rises that pushed prospects for the Federal Reserve’s first rate cut firmly into the summer. A gauge of default insurance only rose to levels recorded on Monday.

The continued strength of corporate-bond spreads underscores the numbing effect of persistent flows pouring into credit funds, making managers flush with cash that needs to be invested. Even a blow to the main driver of bullish expectations for bond returns this year — interest-rate cuts by central banks as the battle against inflation approaches its end — is not enough to dent it.

CBRE might have called the bottom in commercial real estate last week...

CBRE said Thursday it’s “cautiously optimistic” that the worst is over for office leasing, particularly for the Class-A properties that make up about two-thirds of its leasing revenue. The positive tone briefly helped quell worries about the market for commercial real estate that have roiled shares in property managers and lenders from New York to Munich and Japan in recent weeks.

CBRE’s results “point to us approaching somewhere close to the bottom of the cycle in terms of commercial property,” said Haig Bathgate, head of investments at UK wealth manager Atomos. “There’s evidently been a lot of negativity in this asset class.”

Hot in 2021: Leaving the Bay Area. Hot in 2024: Moving to the Bay Area...

Many have discovered that launching a startup tech company without a California presence is like entering the boxing ring with one hand tied behind your back.

During the pandemic, scores of Silicon Valley investors and executives such as Rabois decamped to sunnier American cities, criticizing San Francisco’s government as dysfunctional and the city’s relatively high cost of living. Tech-firm founders touted their success at raising money outside the Bay Area and encouraged their employees to embrace remote work.

Four years later, that bet hasn’t really worked out. San Francisco is once again experiencing a tech revival. Entrepreneurs and investors are flocking back to the city, which is undergoing a boom in artificial intelligence. Silicon Valley leaders are getting involved in local politics, flooding city ballot measures and campaigns with tech money to make the city safer for families and businesses. Investors are also pushing startups to return to the Bay Area and bring their employees back into the office.

San Francisco has largely weathered the broader crunch in startup funding. Investment in Bay Area startups dropped 12% to $63.4 billion last year. By contrast, funding volumes for Austin, Texas, and Los Angeles, two smaller tech hubs, dropped 27% and 42%, respectively. In Miami, venture investment plunged 70% to just $2 billion last year.

“An ecosystem such as SF’s that has been built over the last 50-plus years doesn’t just die because of a pandemic for a few years,” said Mo Koyfman, founder of venture firm Shine Capital. He pointed to the proximity of universities such as Stanford as reasons why top-tier venture firms need to maintain a presence in the Bay Area.

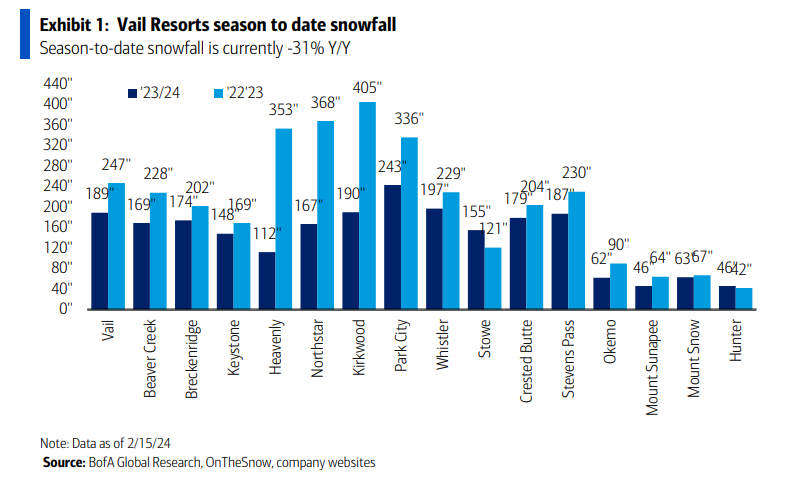

Go Stowe!

After an incredible 2022-2023 ski season, this year's snow yardsticks are lagging unless your mountain is in Vermont. Let's see if California can get one more big one before the March temps begin to melt it away.

BofA Global

I have been riding my Peloton wrong for six years now...

Let's see if I can do it correctly for the next 50 years. If you haven't read "Outlive: The Science and Art of Longevity", pick it up and check it out. A great read. See you at the back of the pack.

If you think every workout has to be a sweat-fest that leaves you gasping for air, think again.

You should perform most of your cardiovascular exercise at a level that lets you carry on a slightly strained conversation. It broadly means exercising at a relatively low effort for a long time.

This type of training helps us produce energy more efficiently by stimulating our cells’ powerhouses, the mitochondria. Over time, this translates to better health and athletic performance.

Elite athletes spend much of their time training at this intensity. It is the secret to helping them go faster for longer, says Dr. Benjamin Levine, a sports cardiologist at UT Southwestern Medical Center in Dallas.

In fitness speak, that mellow intensity level is called Zone 2. Its benefits have recently been touted in books like the bestseller “Outlive: The Science & Art of Longevity,” by Peter Attia and on the eponymous performance-focused podcast hosted by Stanford University neuroscientist Andrew Huberman.

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: The Home Depot Inc., Coca-Cola Co., and ASML Holding NV

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.