Weekly Research Briefing: The Acceleration Hits

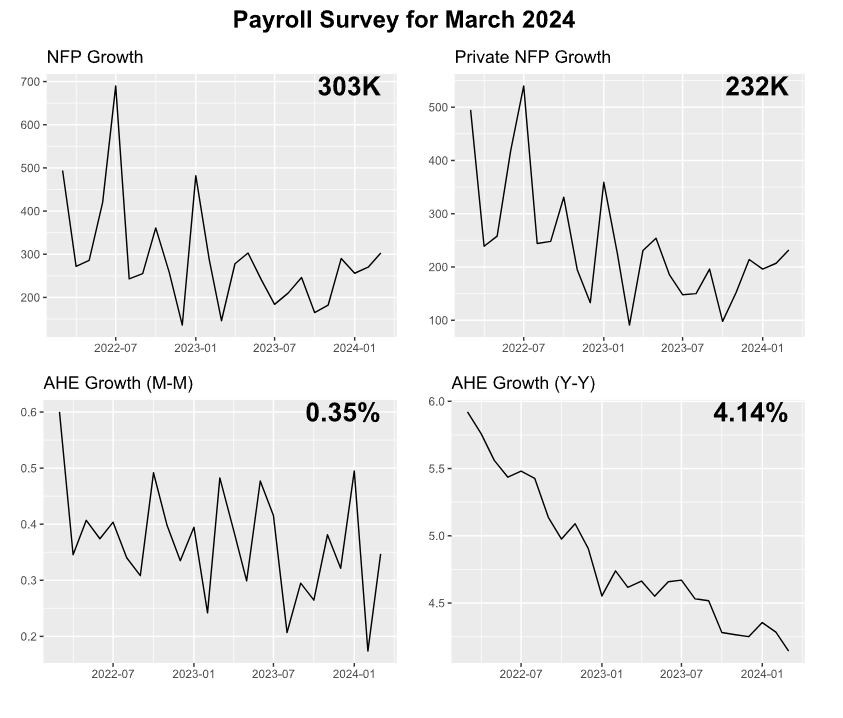

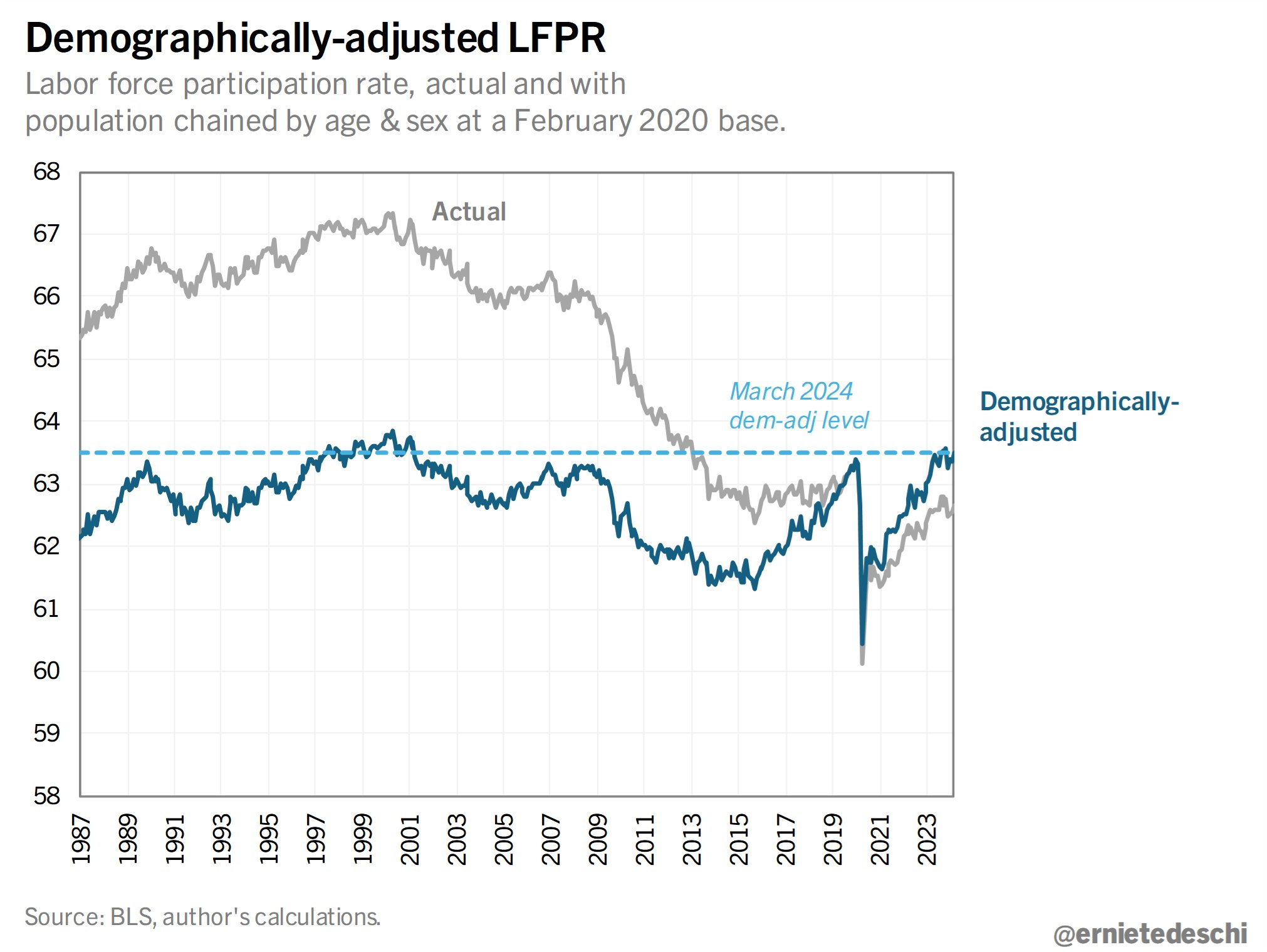

While many await a slowdown, the U.S. economy laughs and shifts into a higher gear. Last week's surge came as a result of Friday's monthly jobs data which showed accelerating job production and tepid wage growth. Both the payroll and household surveys contributed strong numbers. March's job creation was led by part-time jobs as industries like leisure/hospitality, construction, retail and healthcare amounted to almost 2/3'rds of the new jobs. And if you look at the demographically adjusted labor force, the U.S. is back to running at past peak employment levels. So even if employers were looking for full-time workers, are they even available?

As the jobs picture continues to improve, the forward data on transportation numbers and manufacturing orders are also shining brighter. This pickup is causing fits in the treasury bond market, while also pushing investors to consider investing their equity portfolios outside of the Mag 7. Cyclical stocks continue to outperform defensives. And value stocks are attempting to get a leg up on growth stocks. Ditto for small-cap and international equities. Maybe the upcoming earnings period will give non-Mag 7 companies a platform to talk about their improved outlooks and lower valuations. We will find out beginning this week as the big banks and a handful of other S&P 500 giants lead the discussion about Q1 earnings and their outlooks for 2024. In addition to earnings, the big CPI and PPI inflation readings will drop mid-week.

Have a great week and start to the April earnings period.

Friday's jobs numbers were fantastic...

Accelerating job growth and year over year wage growth of +4.1% which is running above the +3.2% inflation rate.

@ernietedeschi

Welcome to full employment...

@ernietedeschi: Adjusted for aging, employment and labor force participation rates are extraordinary, around 1999-2000 levels, likely ranking among the highest in US history. This is truly about as close to full employment as the US has managed to get outside of wartime mobilization.

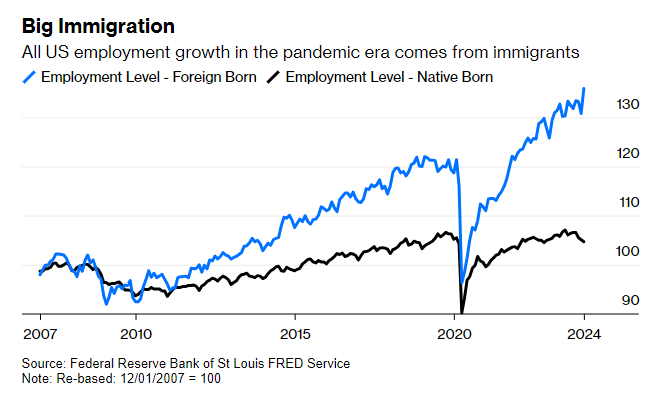

COVID retirements and workforce exits nearly crippled the U.S...

If not for positive U.S. immigration, the U.S. economy would have been significantly impacted by labor imbalances and wage inflation the last four years. As a result, America now has one of the strongest economies in the world.

Big influxes of new migrant workers can ease the risk of a damaging wage-price spiral by giving employers a greater pool to recruit from. And at present, it looks as though labor shortages would feel severe (and hence the upward pressure on wages and prices would be more intense) if it were not for a sharp increase in the number of foreign-born workers looking for a job. The figure of native-born workers in employment is still slightly below the level from the eve of the pandemic; employment of the foreign-born has increased by more than 10%.

Don Rissmiller, chief economist of Strategas Research Partners, points out that the US has been “significantly boosted by additional labor supply (a country with more people has more GDP),” and that this has offset ageing demographics. He adds: “This could be a politically unstable path (especially given the US election in November), but it counts as growth in the meantime. ‘Big immigration’ helps explain the resilience of US activity against the backdrop of more sluggish economic data abroad.”

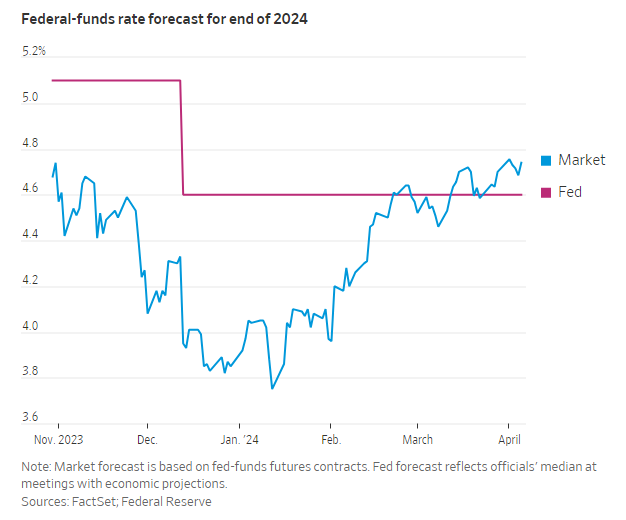

As the economic trade-off tilts toward growth, future Fed Funds rate cuts are being scrutinized...

Wall Street’s expectation that the Federal Reserve will cut interest rates several times this year has helped power stocks to records. Now, some investors think the central bank might not cut rates at all.

After the latest blockbuster jobs report Friday showed continuing strength in the economy, more traders are betting the Fed may cut the benchmark federal-funds rate just once or twice this year, fewer than officials’ last median forecast of three quarter-point cuts. And a handful are even starting to wager that the central bank will leave rates where they are...

“The last of the economic bears are throwing in the towel,” said Joe Brusuelas, chief economist at RSM US. “We have a sustained economic expansion, and investors who manage risk are now repricing it.”

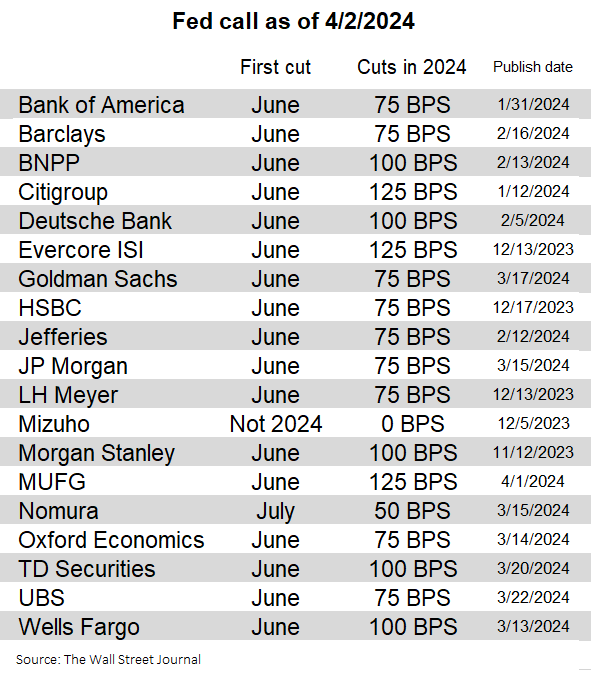

And most all of Wall Street has slid their next cut forecast to June...

@NickTimiraos: The sell-side bank and Fed forecaster consensus is now aligned in expecting the first rate cut in June, with the previous outliers recently junking their recession calls. The uniformity here oversells the degree of conviction around a June cut. These have moved a lot in 2024.

In favor of rate cuts are ongoing indications of slowing inflation. This week will be a big one for input there...

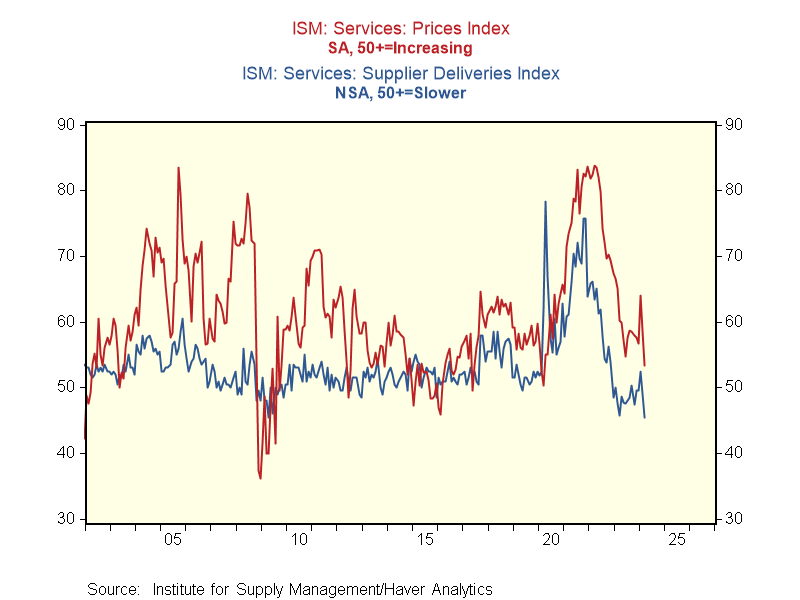

@RenMacLLC: Cooling off of services inflation? In March, the ISM services prices index eased to 53.4, the lowest since the onset of the COVID-19 pandemic. Supply chains have shown improvement too with supplier delivery times improving to their best since April 2009.

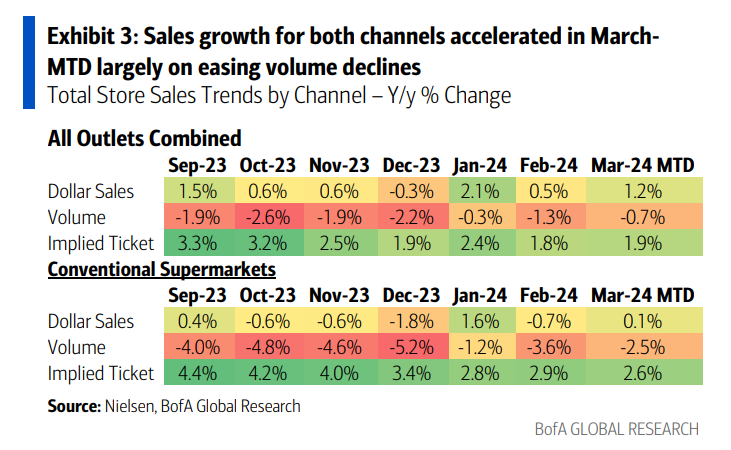

Here is a grocery store inflation data point falling to +2.6% year over year in March...

BofA Global

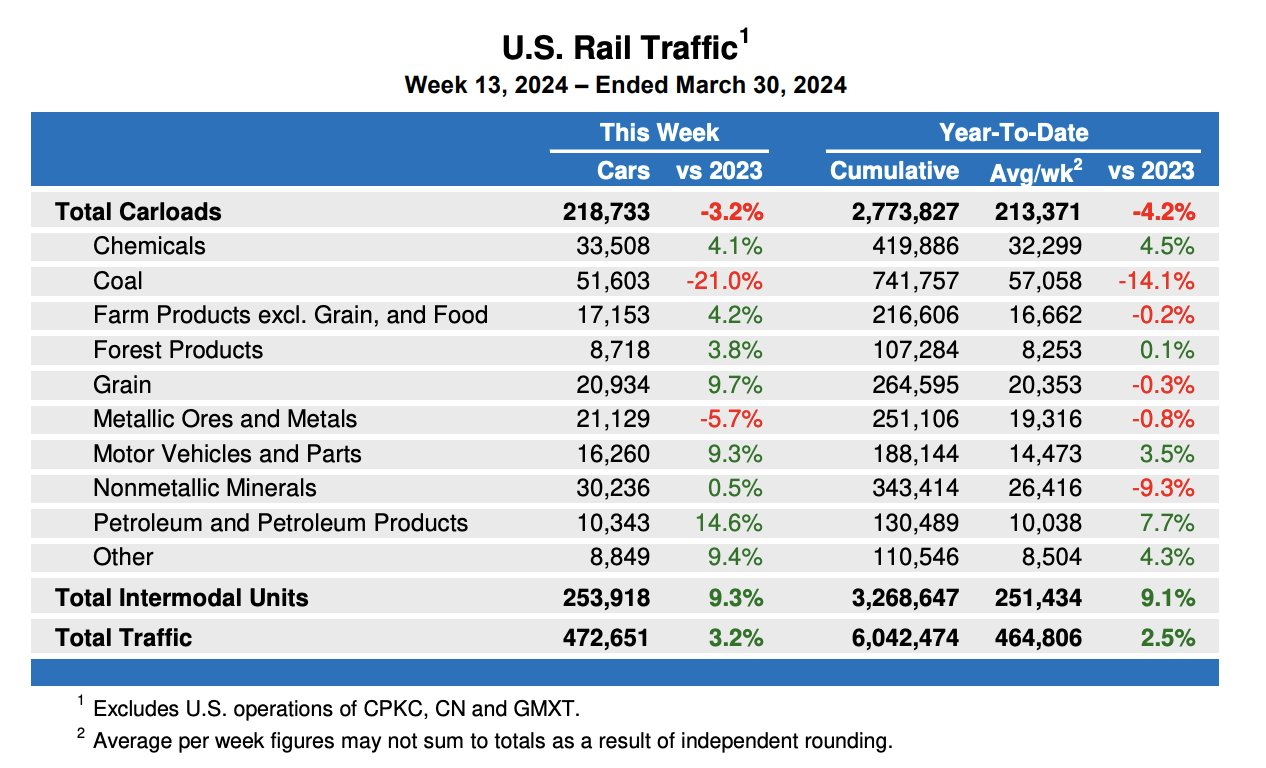

U.S. rail traffic continues to surprise on the upside...

@SethCL: If there were a forward leading indicator of manufacturing and retail sales it may be rail traffic, as I have been pointing at since Q4 2023. The trend in growth has been heralding a rebound in goods transports, now being expressed in #ManufacturingPMI

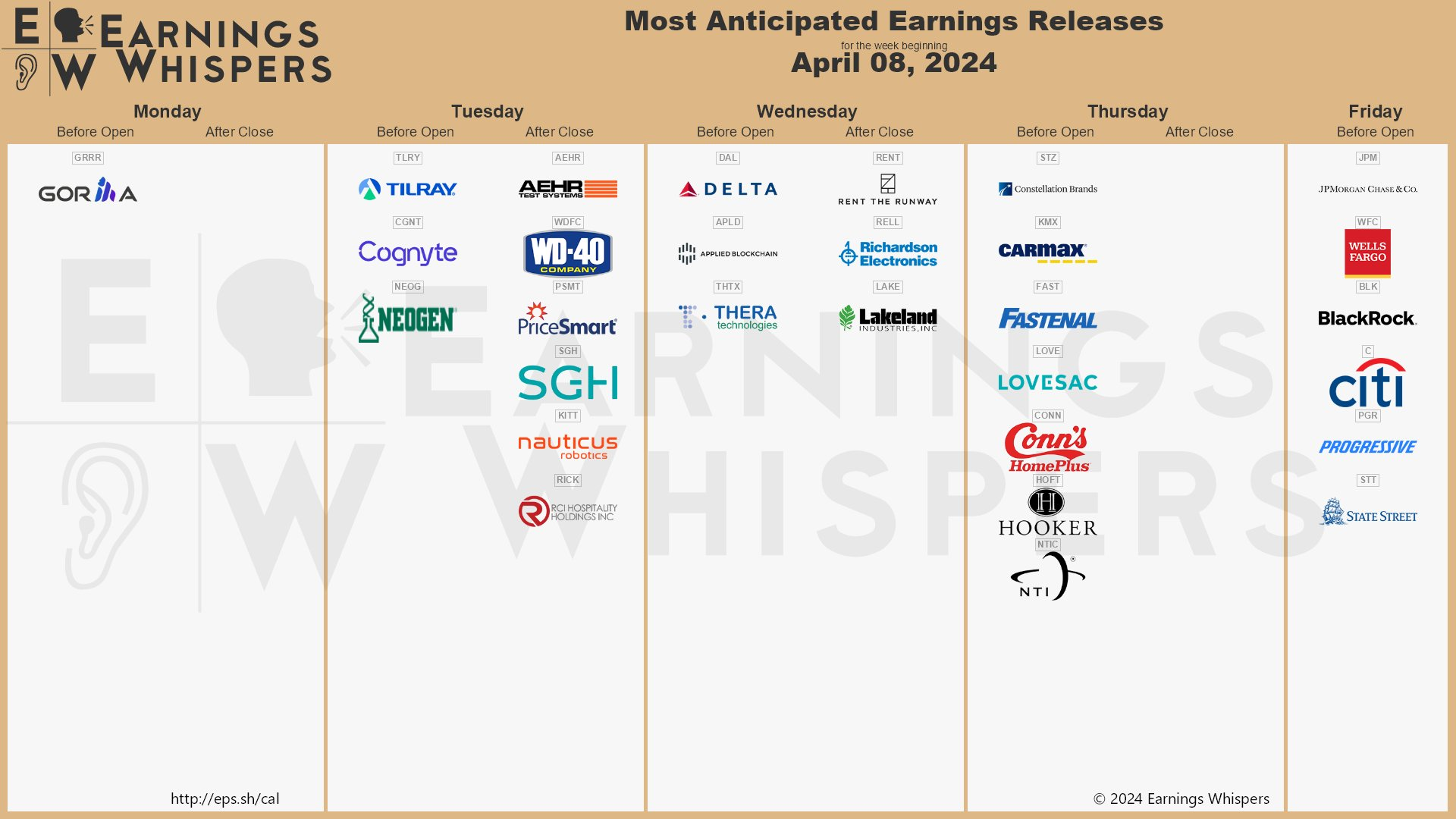

Here comes Q1 earnings reports...

Let's see if WD-40 can copy their spectacular report from three months ago. The big financials begin on Friday with J.P. Morgan, Wells and Citi dropping before the markets open.

@eWhispers

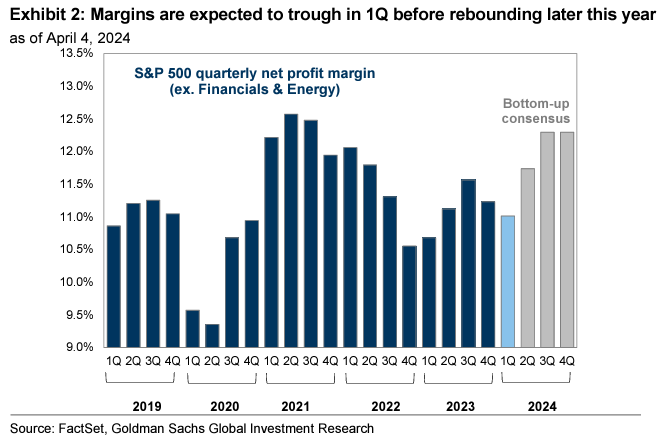

This Q1 should be the low in margins for 2024 and guidance for future quarters will be closely watched...

S&P 500 margins are expected to sequentially trough in 1Q. Bottom-up consensus expects the S&P 500 will post 10.9% net margins in 1Q, a 28 bp sequential contraction but a 2 bp yr/yr expansion. Energy, Materials, and Health Care are each expected to post yr/yr margin contractions of greater than 100 bp. The 10 S&P 500 stocks with the largest market caps are expected to expand margins by nearly 400 bp year/year while the remaining 490 firms in the index will see margins fall by 57 bp.

Goldman Sachs

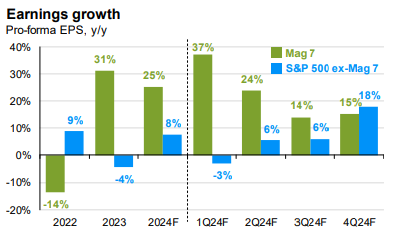

As economic strength broadens in 2024, the non-Mag 7 companies will have a good earnings story to follow...

A resilient economy and strong consumer demand are expected to fuel a rise in earnings growth for S&P 500 companies for a second straight quarter following three straight quarters of profit contraction. And strong margins from big tech firms will likely be a key driver.

Profits for the seven biggest growth companies in the S&P 500 — Apple Inc., Microsoft Corp., Alphabet Inc., Amazon.com Inc., Nvidia Corp., Meta Platforms Inc. and Tesla Inc. — are on course to rise 38% in the first quarter, according to Bloomberg Intelligence. When excluding them, the rest of the index’s profits are anticipated to shrink by 2%.

Wall Street expects this trend to reverse as the year progresses. In the fourth quarter, those seven firms are expected to post earnings growth of 15% compared with 18% for the rest of the S&P 500, according to data compiled by David Kelly, chief global strategist at JPMorgan Asset Management.

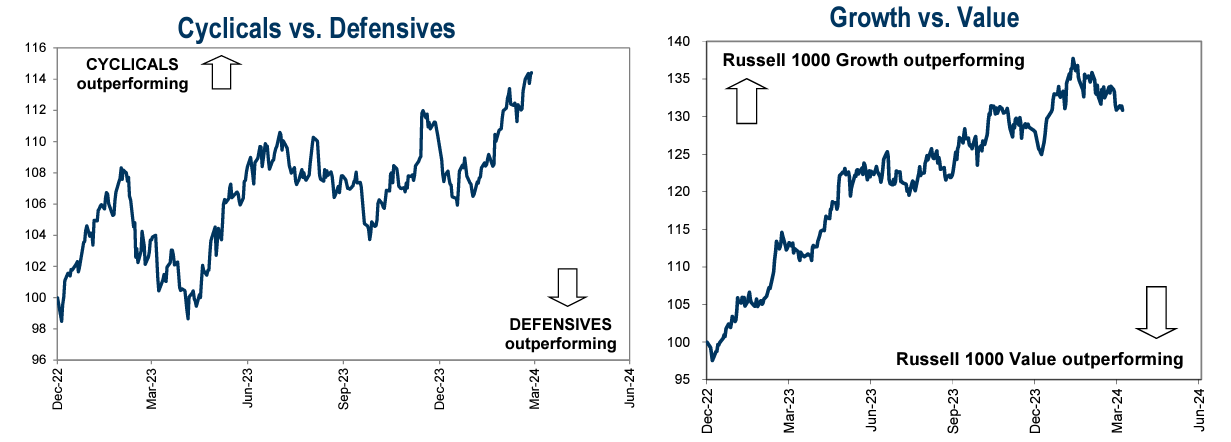

Cyclicals have confirmed a broadening out of the market. Now it is time for Value stocks to follow...

Goldman Sachs

The S&P 500 took home all the chips last year. Can't imagine a repeat as the economy broadens out...

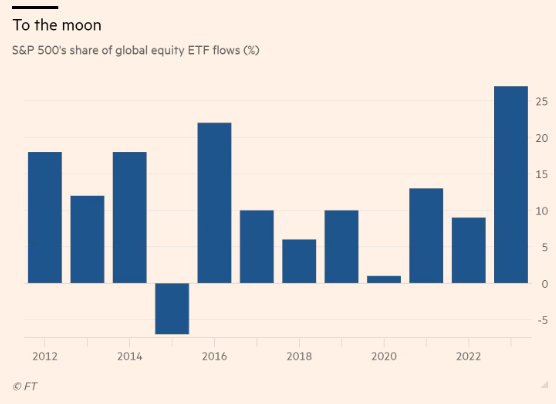

Wall Street’s blue-chip S&P 500 index captured its highest share of global equity exchange traded fund flows for at least a decade last year, as the rise of the so-called Magnificent Seven reshaped benchmarks worldwide.

ETFs tracking the S&P 500 vacuumed up a record $137bn in net terms last year, according to data from Vanguard, surpassing the previous peak of $119bn in 2021.

This accounted for a record 27 per cent of all global equity ETF flows, compared with just 9 per cent in 2022, 13 per cent in 2021 and 1 per cent in 2020. The prior peak, in data going back to 2012, was 22 per cent of global flows in 2016.

The inflows means America’s global dominance of global equity markets is now approaching the levels seen in the 1950s and 1960s, when the US led the postwar economic recovery and the Nifty Fifty grouping of Wall Street blue-chip stocks reaped the rewards.

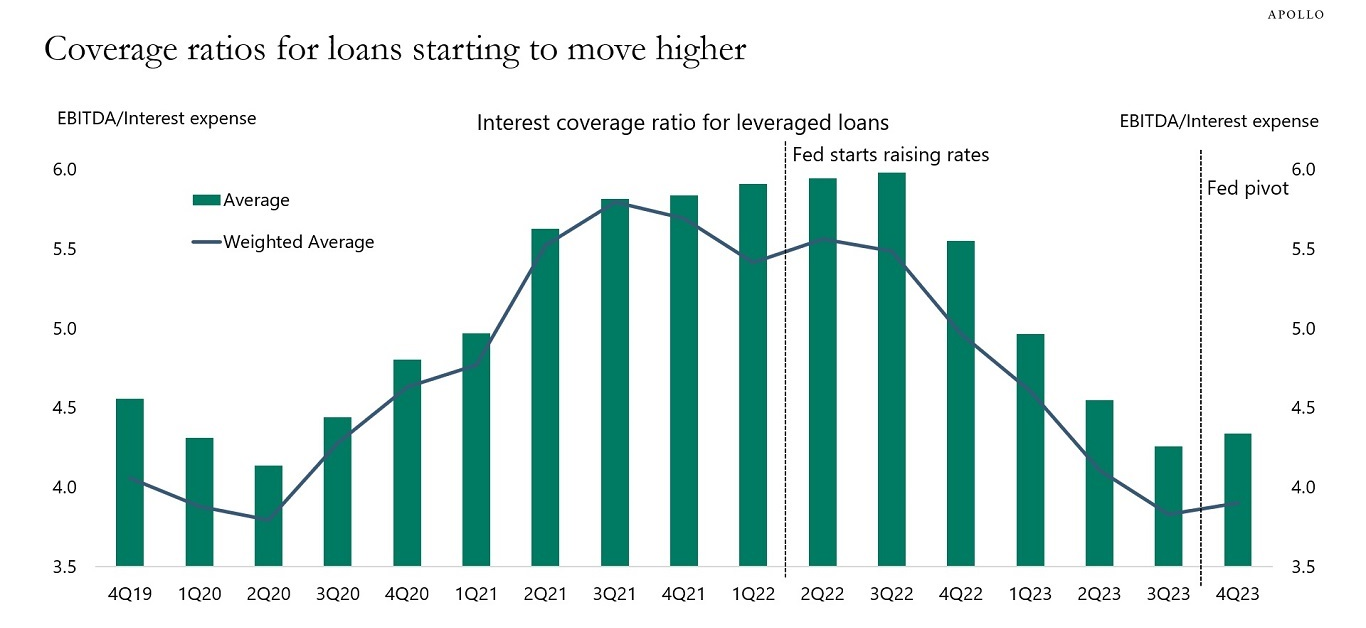

Improving top lines and margins is leading to better interest coverage which should accelerate in 2024...

After the Fed started raising rates in March 2022, coverage ratios began to move lower, see chart below, and after the Fed turned dovish at the November 2023 FOMC meeting, coverage ratios have started to rebound. The bottom line is that the strong economy and strong earnings combined with very easy financial conditions are helping companies manage their balance sheets, including high debt levels.

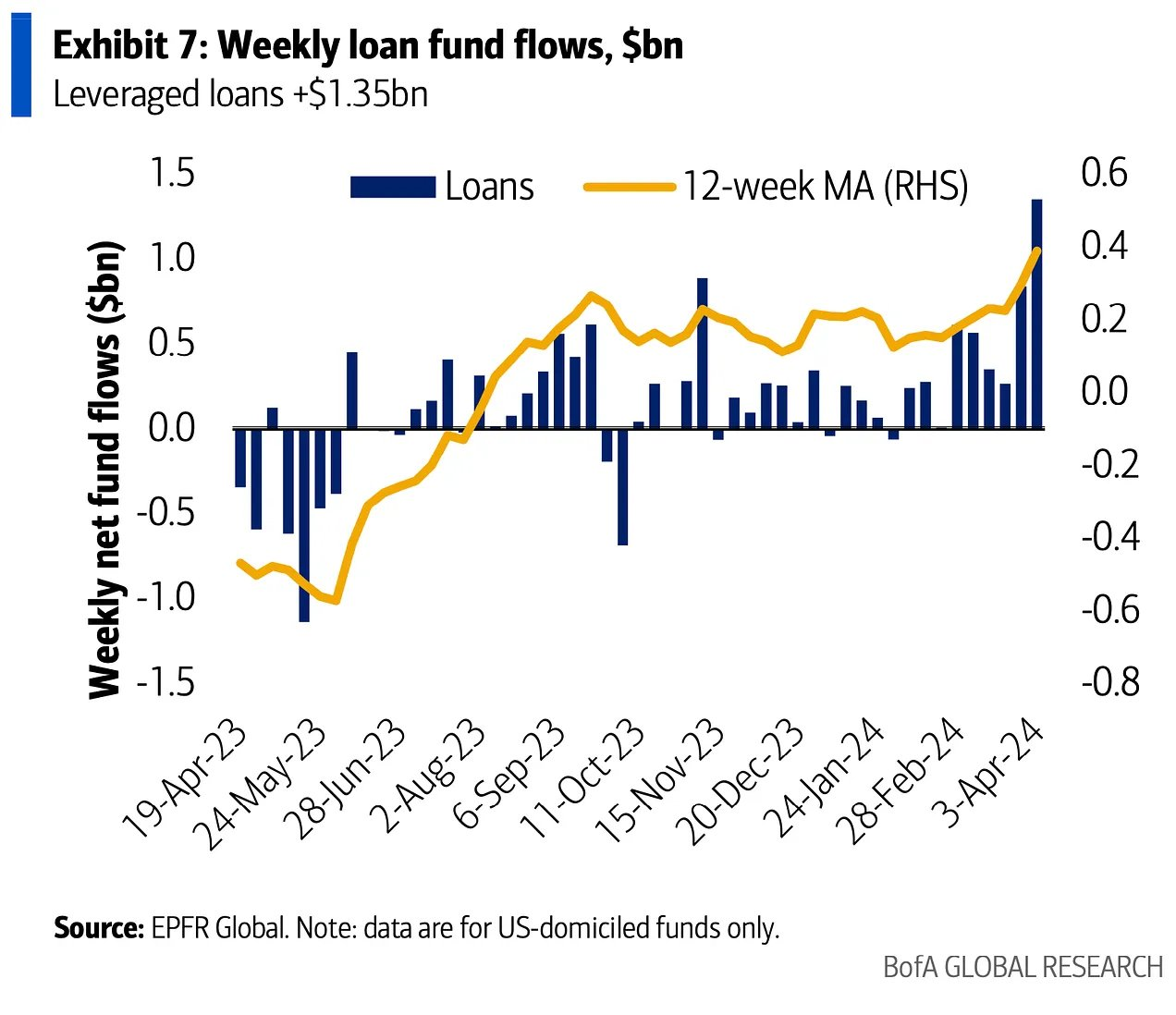

This outlook for better interest coverage is why investors are so comfortable pushing into the credit markets...

@dailychartbook: "This week’s inflow to loans was the strongest weekly inflow since April 2022, at [+$1.35bn] from +$0.84bn the prior week." – BofA

Here is an example of a large high yield credit deal that was 4-times oversubscribed...

Rakuten Group Inc. priced a $2 billion junk bond after boosting the size of the offering by 60% due to strong demand from investors.

The Japanese conglomerate priced the deal to yield 9.875%, according to information from a person familiar with the matter. The issuer increased the five-year deal from $1.25 billion on Wednesday, after demand for the offering surpassed $8 billion, according to people with knowledge of the matter...

A sweetener for investors was that Rakuten’s offering promised a much higher yield than other similarly rated BB credits. The average yield-to-worst on bonds with this rating is 6.63%, according to data compiled by Bloomberg.

The latest transaction marks Rakuten’s second offering this year after it sold $1.8 billion of notes in January that yielded 12.125% — a record for a Japanese firm issuing dollar bonds.

I could have written a book about all the M&A deal announcements over the last 2 weeks...

Instead, here is a list of all the headlines. Look at all this activity. Public companies, private companies and financial buyers are all active. Confidence has returned to the markets and corner offices are acting.

- “High quality property Apartment Income REIT Corp (AIRC - R1000 - $4.5b market cap) to be taken private by Blackstone Real Estate for $39.12/share in a $10B all-cash transaction”

- “Cloud revenue management software provider Model N (MODN - R2000 - $1b) To be acquired by Vista Equity Partners at $30/share in $1.25B all-cash transaction”

- “Aerospace company Ducommun (DCO - R2000 - $700m) confirmed that the Company’s Board of Directors has received an unsolicited non-binding indication of interest from Albion River LLC, a private direct investment firm, to acquire all outstanding shares of Ducommun for $60.00 per share in cash”

- “Insurance software company Sapiens (SPNS - R2000 - $1.7b) will explore a sale of the company”

- “Cardiovascular device manufacturer ShockWave Medical (SWAV - R1000) To be acquired by Johnson & Johnson (JNJ) at $335.00/shr in cash at EV of $13.1b”

- “Jersey Mike's considering a sale to Blackstone for $8b”

- “Allianz (ALV.DE) to sell U.S. MidCorp and Entertainment insurance business to Arch Capital (ACGL) for $450m”

- “Australian credit bureau Illion bought for AUS$820m by Experian (EXPN.UK)”

- “Hubspot (HUBS - R1000 - $33b mkt cap) in talks with Google (GOOGL)”

- “DS Smith (SMDS.UK) in talks with Int'l Paper (IP) and Mondi Group (MNDI.UK) about a €5b deal”

- “Kerig (KER.FR) Acquires Via Monte Napoleone 8 property in Milan fashion district for €1.3B from Blackstone”

- “Gildan Activewear (GIL.TO - C$8.3b mkt cap) put up for sale by Board”

- “Saint-Gobain (SGO.FR) to acquire Bailey Group for C$880m”

- “TPG Capital signed a definitive agreement to acquire Classic Collision, a leading, national collision repair multi-site operator”

- "Schlumberger (SLB) to buy ChampionX (CHX) in $7.8b all-stock deal”

- “EQT confirms exclusive talks with ICG Infra to acquire Ocea Group, a leading French water and heat submetering infrastructure provider”

- “BC Partners inked a $4b deal to sell a majority stake in information technology provider Presidio to Clayton Dubilier & Rice”

- "Welsh Carson Anderson & Stowe agreed to sell compliance software maker Avetta to EQT for about $3b”

- “Silver Lake to take Endeavor (EDR - $18b mkt cap) private in a cash deal valuing entertainment firm at $25b EV which is the largest PE deal of a public company in a decade”

- “Blue Owl (OWL) to Buy Insurance-Focused Asset Manager Kuvare Asset Management for $750m“

- “Canada Pension Plan Investment Board is selling its stake in the world's foremost organizer of motorcycle racing, Dorna, for $1.9b to Liberty Media Corp (LBTYA)”

- “Goldman Sachs Group Inc.’s Petershill unit agreed to acquire a 40% stake in Kennedy Lewis Investment Management”

- “Canadian payments processor Nuvei has struck a deal to be bought by private-equity investor Advent International for $6.3b”

- “Home Depot said it was making a big bet on SRS Distribution, a private-equity-owned roofing distributor”

- “China developer Wanda sells 60% of mall unit to private equity firm PAG in $8.3b deal”

- “Japan's Panasonic Holdings will sell its entire stake in Panasonic Automotive Systems to private equity firm Apollo Global Management for $2b”

- “Alight has agreed to sell its professional services and payroll outsourcing business to an affiliate of private equity firm HIG Capital for up to $1.2b”

- “Britain's Johnson Matthey (JMAT.UK) will sell its medical device components business to Montagu Private Equity for $700m in cash”

- “TPG Inc. is in talks to buy the manufactured housing business of Canadian Apartment Properties REIT for more than C$700m”

- “Francisco Partners to Acquire Jama Software for $1.2b”

- “PAI Partners strikes €330m deal for Italian haircare group Beautynova”

- “Carlisle Companies (CSL) to Acquire MTL Holdings for $410m”

- “The US arm of accounting firm Grant Thornton has agreed to sell a majority stake to the investment group New Mountain Capital”

Multiple tape news sources

One of the more notable deals was Blackstone's decision to pay a 25% premium to acquire a high-end apartment REIT...

Blackstone is taking private Apartment Income REIT, known as AIR Communities, which owns 76 rental housing communities that are primarily in coastal markets, including Miami, Los Angeles, and Boston, the companies confirmed Monday. Blackstone plans to invest another $400 million to improve these properties, the firm said...

The acquisition is Blackstone’s largest transaction in the multifamily market. It reflects the firm’s bullishness on rental housing and its belief that commercial real estate overall is bottoming and the time is ripe to step up investments.

“We can see the pillars of a real-estate recovery coming into place,” Blackstone President Jonathan Gray said on an earnings call earlier this year. “We are, of course, not waiting for the all-clear sign and believe the best investments are made during times of uncertainty.”

Also, in RE, available premium locations colliding with deep pocketed buyers are causing a stir in the high-end retail real estate market...

There’s no commercial real estate crash on New York’s Fifth Avenue or the Champs-Élysées in Paris.

Luxury brands are racing to buy properties on the world’s most famous shopping streets. One reason is the fear that, if they don’t buy their flagship store from the landlord, one of their rivals will do so and send them packing.

Kering, the owner of luxury brands including Gucci and Saint Laurent, handed Blackstone €1.3 billion, or $1.4 billion at current exchange rates, for a building this week on Milan’s Via Montenapoleone. It is one of Europe’s most expensive shopping streets, and Saint Laurent is already a tenant at one of the building’s retail units...

Based on the rent the Via Montenapoleone property is generating, the price Kering paid is equivalent to a roughly 2.5% cap rate—an astronomical price considering where interest rates are at the moment. Like a bond, the lower a cap rate the richer a price paid.

It is Kering’s second major real-estate purchase of the year. The company already spent close to $1 billion in January on a property on New York’s Fifth Avenue. Rivals are also snapping up real estate. Europe’s luxury brands have spent more than $9 billion buying boutiques on the world’s top shopping streets since the start of 2023 based on Bernstein’s analysis. Chanel and LVMH are both hunting for luxury properties in New York, according to real-estate sources.

Looking at the bottom end of real estate...

The office headlines remain dismal, but the big office stocks bottomed nine months ago. Given that the stock market is a forward-looking machine, I would guess that the tone of office RE headlines will improve from here.

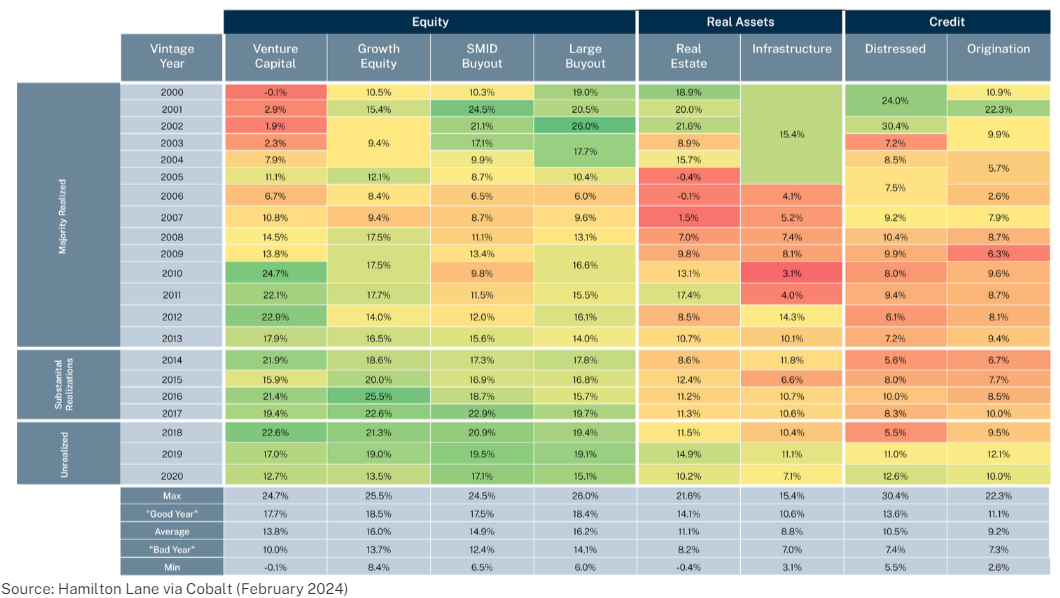

Looking more closely at the Private Markets, our HL Portfolio Management Group wrote a great paper on Portfolio Construction…

Here is a great teaser chart on vintage year returns for various LP fund categories. Much more in the full paper linked below.

LPs commonly look at IRR on a vintage year basis since it represents the total since inception return from the time of the investment decision. That is relevant for closed-end fund investors since the primary allocation decision is made at the time of commitment and rebalancing an exposure incurs significant frictions. The table below highlights since-inception vintage year IRRs since vintage year 2000 by strategy with summary information at the foot of the table. We define “Good Year” and “Bad Year” to be the average vintage year IRR plus or minus half of a standard deviation.

The vintage year IRR data confirms some commonly held beliefs and offers a few surprising ones:

- On average, private equity vintage year IRRs tended to be higher than private real asset or private credit returns. Private equity returns averaged net IRRs in the mid-teens, while real assets and credit were a couple hundred basis points lower.

- Some might also be surprised that the average vintage year IRR for large cap buyout funds is above small- and mid-cap (SMID) buyout funds. There is a widespread perception that small fund performance dominates large fund performance. In aggregate, that is not always the case.

- Venture capital, surprisingly, does not have a higher maximum return or “good year” IRR compared to its private equity peers. The strategy seems to come with more variance in vintage year returns, which is perhaps less of a surprise given the perception of venture capital as a “high risk” strategy. The strategy has posted a run of strong vintage years post-GFC, where vintage year IRRs have averaged 20%, though some of those years have substantial unrealized value remaining.

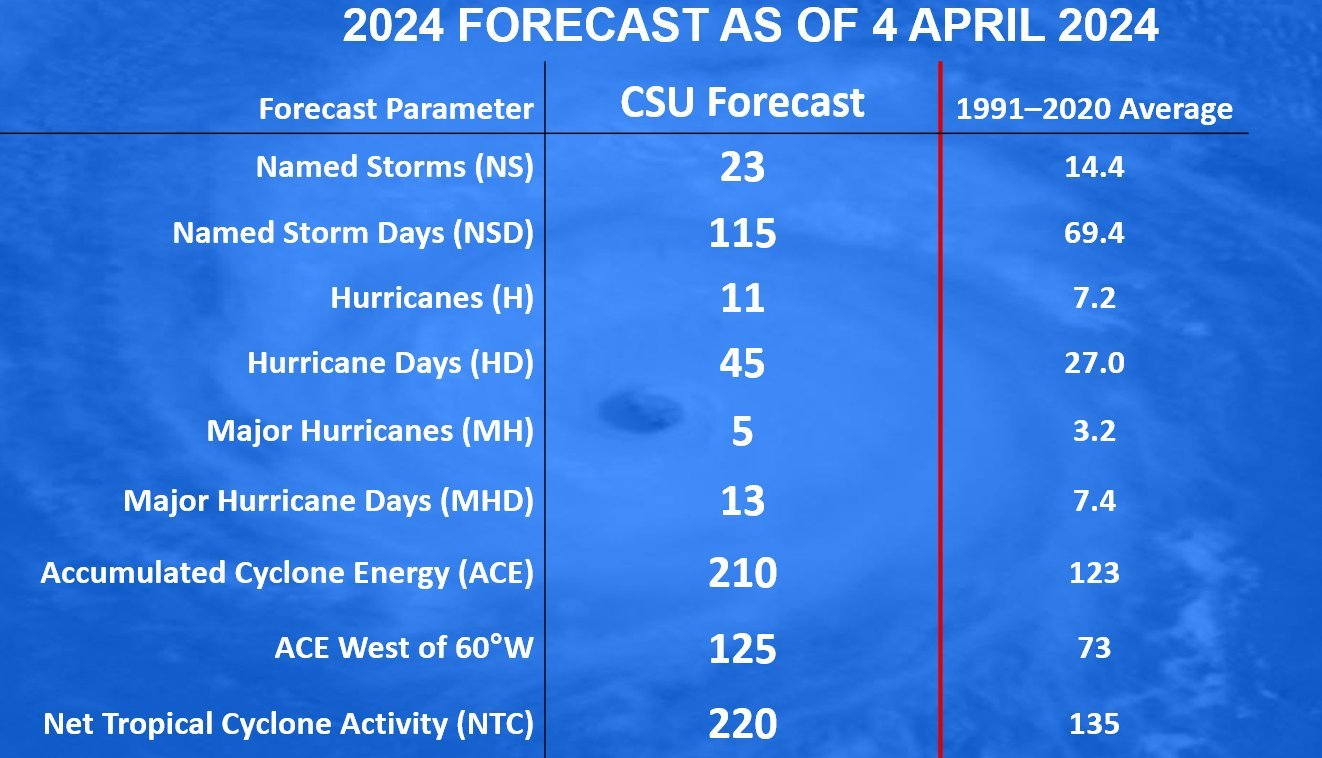

CSU released its 2024 Atlantic hurricane forecast last week. Hot oceans and La Nina will keep the Weather Channel busy...

@MikeZaccardi: The 2024 Atlantic Hurricane Season is expected to produce 23 named storms. ACE 70% above the 1991-2020 average!

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: J.P. Morgan

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.