Portfolio Construction Vol. I: A Foundation for Success

Executive Summary:

- Private markets occupy a growing share of investors’ portfolio, with investors attracted to the asset class by the opportunity set and the potential to generate premium returns.

- The growing choice available to private markets investors provides more opportunity for customization but also risks that must be managed through thoughtful portfolio construction.

- Constructing a private markets portfolio challenges investors to make active management decisions on asset allocation, diversification, investment pacing, and exposure management, which can have a meaningful impact on portfolio risk and return.

- These portfolio construction challenges can be addressed through access to high quality data and rigorous quantitative analysis of the asset class.

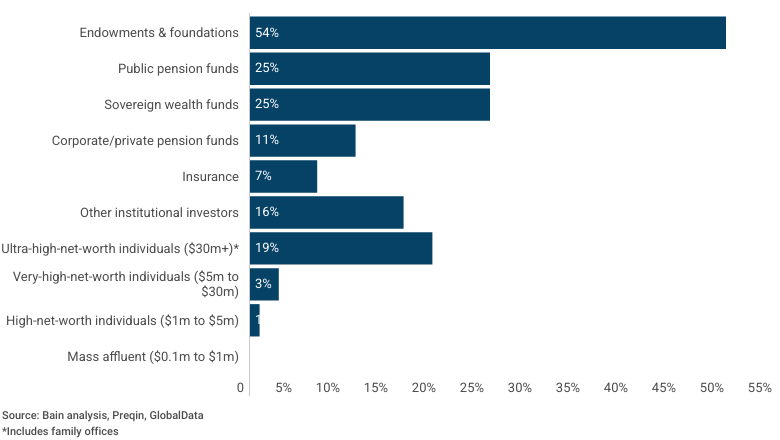

Private markets have long occupied a place in the portfolios of large, sophisticated investors, who have reaped the benefits of the asset class’s strong historical performance. Recent estimates put the average alternatives allocation of public pensions and endowments (thought to be two of the longest tenured types of private market investors) at 25% - 50%.

Share of Investors' Global Wealth in Alternative Assets in 2022

By Investor Type

Interest in the asset class has only intensified in recent years, with over $3.8T flowing into the asset class over the past three years. Both existing investors looking to increase their allocation and new investors building their initial private asset portfolio are faced with the same challenge: What is the most efficient way to construct a private markets portfolio that meets my program’s goals and risk preferences?

Historically, private market investors have focused their efforts on developing robust sourcing channels and diligent security selection. We believe that security selection alone is no longer sufficient: A thoughtful portfolio management approach is an essential component of successful private market portfolios. That portfolio management approach must be informed by rigorous, data-driven analysis and should provide transparency into decision making and private market portfolio drivers. While this function is standard among listed asset managers, private market asset managers have not been as quick to embrace portfolio construction.

Why Include Private Market Investments in a Total Portfolio?

Despite the nearly $4 trillion of capital flowing into the asset class (inspiring claims that the asset class is oversaturated), the case for including private assets in an investment portfolio is as compelling as season four of Succession. The reasons for adding a private markets exposure are as diverse as limited partners (LPs) themselves. Some of these reasons include:

- Private market investments provide access to assets that are not spanned by public markets. Think early-stage companies developing new technologies, niche manufacturing businesses, bespoke specialty loans and infrastructure assets that range from airports to waste management facilities to clean energy sources, among others. These assets are sources of tremendous economic output and should be included in a healthy, diversified portfolio. Some (but not all!) of these strategies may have lower correlations to traditional assets, offering a compelling risk-based case for inclusion in a portfolio.

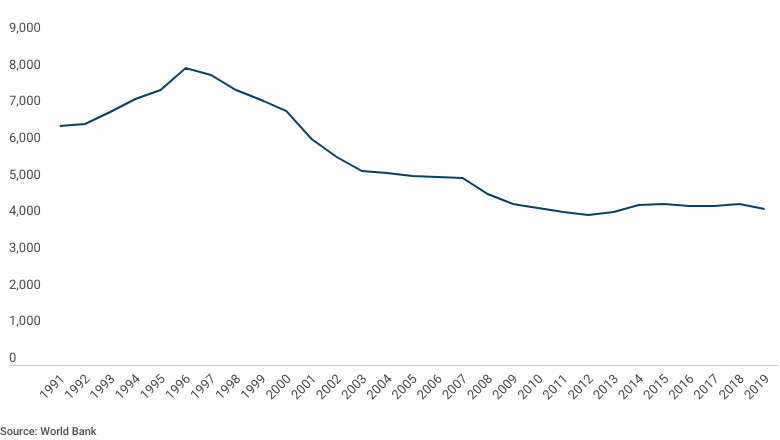

- A declining opportunity set in public markets. While much discussion has focused on whether there is sufficient supply of private investments to soak up new inflows, it seems that listed assets have experienced their own supply pressures. In the U.S., the number of listed companies has declined for nearly two decades and the largest companies now occupy a growing share of benchmark indices: The 10 largest companies in the S&P 500 currently account for 34% of the index weight.

Number of Listed U.S. Companies

There are similar trends in other pockets of the private markets. Take private credit: Banks and other traditional financing sources have backed away from syndicated leveraged lending, which is now being done more capably by private lenders.

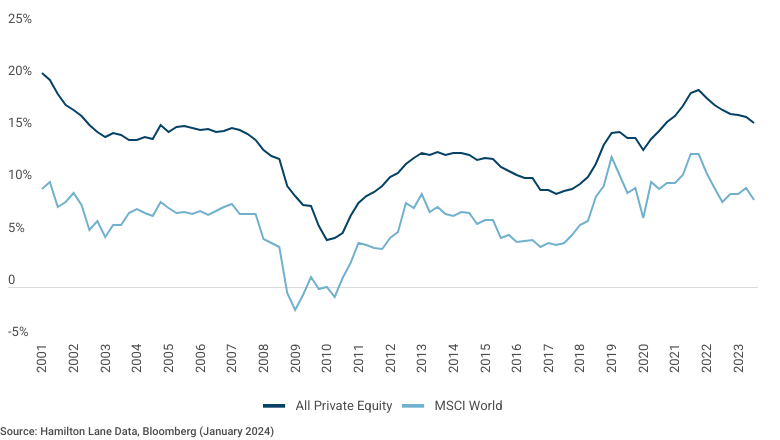

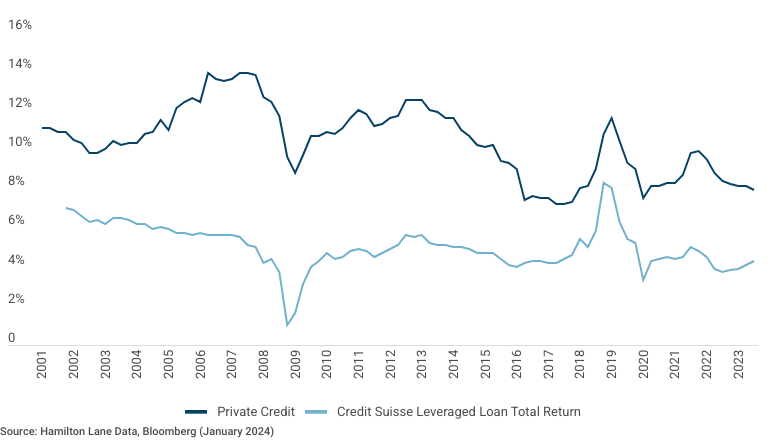

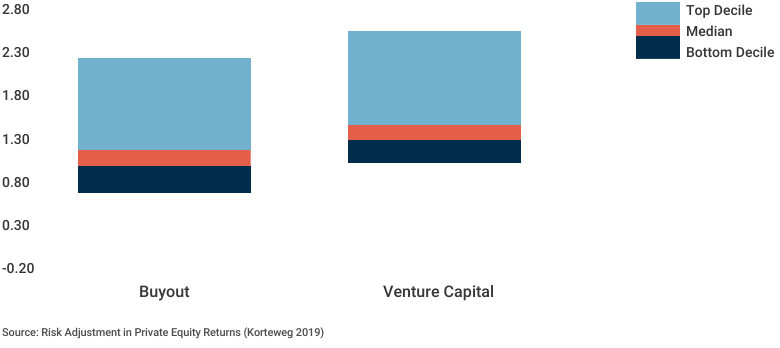

- Return enhancement. Arguably the chief driver of investor interest in private markets is the prospect of generating a premium return as compensation for taking on additional liquidity risk. Historically, private markets have largely lived up to their reputation as a source of premium returns (though you could easily fill an entire year of industry conference airtime debating the sources of those returns!). The compounding effect of hundreds of basis points of excess returns per annum will have an exponential effect on total investor wealth creation.

Private Equity 10-Year Rolling Returns

Private Credit 10-Year Rolling Returns

Portfolio Choice

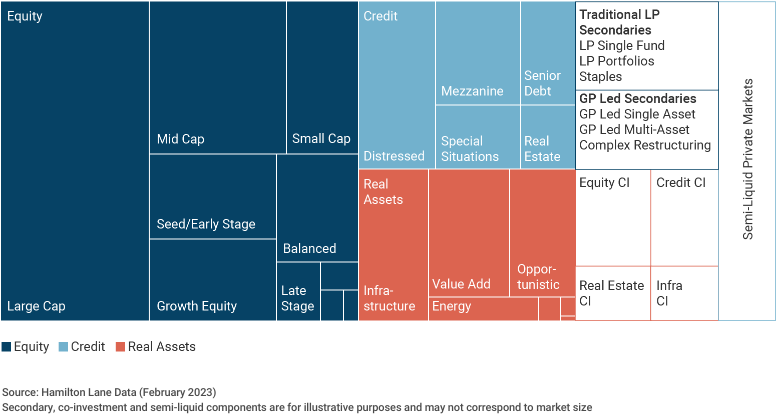

Growing investor interest in private markets has been accompanied by an explosion in the flavors of private market assets, strategies and access points. Take a look at the dollars raised in private markets over the last five years:

Private Markets - Today

Trailing 5Y Fundraising: $3.9 Trillion

The strategies on offer today occupy a much more complete range of risk and return profiles than the strategies on offer just 10 years ago. From the time between the release of Taylor Swift’s album 1989 in 2014 (best track: Blank Space) to the time she released Midnights in 2022 (best track: Snow on the Beach), the number of funds raised increased from approximately 2,800 per annum to nearly 5,700 per annum1, private debt expanded from a distressed debt driven market to include proper loan origination strategies with AUM growing from approximately $704B to $1.94T, infrastructure funds raised $1.01T, and the venture capital market boomed after a decade of dormancy. Private market portfolios are now customizable in ways that were hard to imagine when a young, blonde girl from Pennsylvania released her self-titled debut album. This has shifted the conversation from manager selection to portfolio construction.

Portfolio Construction Levers

While industry dynamics and data suggest investors should seriously consider a private markets allocation, this asset class is certainly not devoid of risk. Successful investors dedicate significant resources to risk management, with the understanding that managing a private markets portfolio entails a much different set of decisions than a portfolio of listed assets does. Benefits do not accrue without a cost.

- The illiquidity of most private assets is among the more obvious factors that investors must contend with. Investors have historically accessed private markets through closed-end fund structures, which have contractual lives that can span a decade or beyond. The timing and sizing of the fund’s cash flows are uncertain, which can make them difficult to predict. At the asset level, hold periods for private equity deals now average five or more years. In the interim, there are few low-friction options for LPs seeking liquidity.

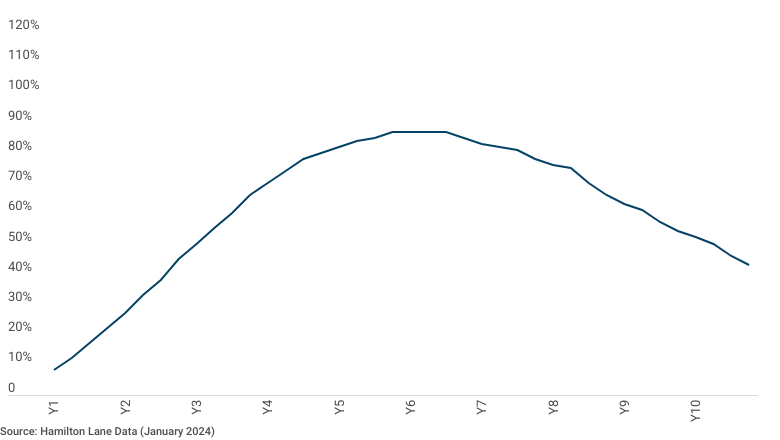

- Building and managing exposure can be a challenge when investing through closed-end, blind pool limited partnerships, which have long been the default investment options for many LPs. At the early stage of a fund’s life there is little exposure to private companies as it takes time for a fund manager to build a portfolio of assets. As the fund’s assets mature and are sold, the exposure to private companies winds down.

Private Equity Average NAV as a % of Fund Size

Vintage Years 2000-2021

This means that fund investors must pay careful attention to the sizing and pacing of their commitments to achieve and maintain a target exposure to private markets. Newer structures, such as co-investments, secondaries, and evergreen funds give investors more tools for building and managing exposure.

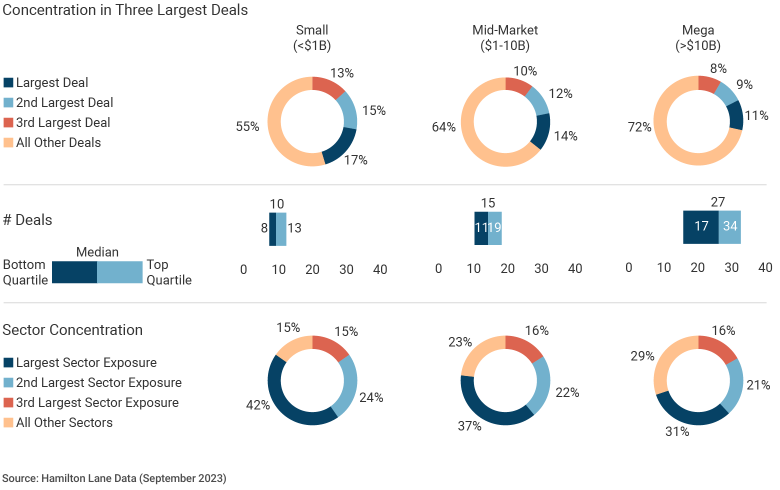

- Diversification across multiple dimensions is possible with strategic portfolio construction. Asset-level diversification is the primary focus of many LPs since private equity funds are typically concentrated by both sector and number of deals.

Average Buyout Fund Diversification by Fund Size

But that is not the only axis of diversification which LPs need to consider: Vintage year diversification is equally important since funds and deals are not continuously up for bid and there is substantial variance in vintage year returns.

- Sourcing: Historically, there have been limited (credible) investable private markets solutions by which a new investor can easily buy a slice of a diversified private markets exposure (though there are innovative structures looking to change that!). As a result, investors must work to source fund manager relationships. LPs looking for co-investment and secondary market exposure must build additional sourcing channels (and diligence capabilities), especially if they are sensitive to “double down” risk: betting additional capital on a portfolio company they already have exposure to through a fund investment. Private market investors must be prepared to be active portfolio managers.

All of these portfolio construction levers create opportunities for well-informed investors with a thoughtful, strategic plan to create additional value in their portfolios. But – and arguably more importantly – thoughtful portfolio construction is a critical risk management function. The establishment and documentation of portfolio goals and the tracking of those goals can help limit the risk of falling short of expectations.

Data and Measurement Challenges

Data opacity and attribute measurement can hinder even the cleverest portfolio strategists. For all the portfolio benefits that an investment in private assets can yield, it is likely the single worst asset class for reliable, transparent data, bar none. It is the Gigli of data. We believe that this has stunted the development of sophisticated portfolio construction techniques, since high-quality data is a prerequisite for the development of portfolio construction strategies.

Commercially available datasets have made strides over the past decade, with a few high-quality data sources emerging, which have enabled LPs to make smarter portfolio construction decisions.

| Lack of a long history of reliable data | Lack of consensus on "best" performance measurement techniques | |

| Challenges |

|

|

| Solutions |

|

|

But the challenge for LPs doesn’t stop after data acquisition. The debate over how to measure key portfolio construction attributes is more intense than the debate over how to pronounce GIF. Private assets are valued infrequently (usually on a quarterly basis) and are necessarily subject to appraisal valuations: an estimate of the price an asset would fetch in an orderly sale process between two informed parties. Cash flows for an asset can also be unpredictable and therefore may not occur at a constant frequency or size. This stands in stark contrast to listed assets, which have observable, transaction-based prices available by the millisecond. The measurement techniques designed with those characteristics in mind must be adapted to account for the quirks of private market investments.

There are three critical attributes that must be estimated for each private markets strategy or investment: return, risk, and liquidity. Return and risk may seem obvious – after all, they are central to nearly every asset allocation framework under the sun.

But as we’ll see in this series, the accurate estimation of those parameters and the incorporation of those estimates into traditional portfolio optimization exercises is trickier than it may seem at first glance. It won’t surprise you to learn that estimating risk is a particularly contentious subject. A recent survey of literature that sought to estimate the beta of private equity found beta estimates ranging from 0.4 to nearly 3.0, proving that the best way to start a bar fight among private market risk professionals is to ask them their estimate of beta for private equity.

Dispersion of Academic Private Equity Beta Estimates

Some might argue that liquidity is a subset of risk, but we think that liquidity deserves special consideration given the quantum of liquidity risk inherent to the asset class (there is a reason many investors specify an “illiquidity premium” in their private market benchmarks). Investors accessing the private markets through fund structures will have some portion of their commitment tied up for over 10 years, while, at the asset level, average hold periods approach or exceed five years for private equity, infrastructure and real estate assets. A thoughtful portfolio construction plan should account for that illiquidity so that allocations can be sized and built prudently.

A Preview of What’s to Come

We’ve now spent nearly 2,000 words laying out the myriad of decisions investors must make to construct a successful private markets portfolio. The challenges facing private market investors are varied and complex. The good news: These challenges can be overcome with high-quality data, the appropriate tools to apply theory to data, and a willingness to view data from several angles to build the confidence that you have the right approach.

Hamilton Lane is fortunate to maintain what we believe to be one of the most comprehensive, detailed private asset datasets in the industry. We track data on tens of thousands of funds and hundreds of thousands of assets stretching back to the decade that gave us the floppy disk, the first Rocky movie, and the dissolution of a modestly successful musical act from Liverpool (that’s the 1970s).

Hamilton Lane Fund Investment Database

12,500+ Funds | 8,600+ Fund Families*

We’ve also spent over 30 years (alas, we are no longer eligible for any 30 Under 30 lists, no matter how much we insist our next birthday is still our 29th) building tools to analyze that data, with a particular focus on portfolio construction. In the coming months, we will share the data and insights that influence our private markets portfolio construction philosophy in a series of papers, covering topics such as:

- Techniques for estimating risk, return and liquidity that inform asset allocation decisions

- Mechanisms for building and managing private markets exposure and liquidity

- Evaluating portfolio health and portfolio maintenance

Strategic portfolio construction is critical to the success of private markets portfolios. With this data and toolkit in hand, we hope that private markets investors will make savvier portfolio construction choices and will build more resilient portfolios. Stay tuned.

All Private Markets: Hamilton Lane’s definition of “All Private Markets” includes all private commingled funds excluding fund-of-funds, and secondary fund-of-funds.

CI Funds: Any fund that either invests capital in deals alongside a single lead general partner or alongside multiple general partners.

Co/Direct Investment Funds: Any PM fund that primarily invests in deals alongside another financial sponsor that is leading the deal.

Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.

Credit: This strategy focuses on providing debt capital.

Distressed Debt: Includes any PM fund that primarily invests in the debt of distressed companies.

EU Buyout: Any buyout fund primarily investing in the European Union.

Fund-of-Funds (FoF): A fund that manages a portfolio of investments in other private equity funds.

Growth Equity: Any PM fund that focuses on providing growth capital through an equity investment.

Infrastructure: An investment strategy that invests in physical systems involved in the distribution of people, goods, and resources.

Late-Stage VC: A venture capital strategy that provides funding to developed startups.

Mega/Large Buyout: Any buyout fund larger than a certain fund size that depends on the vintage year.

Mezzanine: Includes any PM fund that primarily invests in the mezzanine debt of private companies.

Multi-Management CI: A fund that invests capital in deals alongside a lead general partner. Each deal may have a different lead general partner.

Multi-Stage VC: A venture capital strategy that provides funding to startups across many investment stages.

Natural Resources: An investment strategy that invests in companies involved in the extraction, refinement, or distribution of natural resources.

Origination: Includes any PM fund that focuses primarily on providing debt capital directly to private companies, often using the company’s assets as collateral.

Private Equity: A broad term used to describe any fund that offers equity capital to private companies.

Real Assets: Real Assets includes any PM fund with a strategy of Infrastructure, Natural Resources, or Real Estate.

Real Estate: Any closed-end fund that primarily invests in non-core real estate, excluding separate accounts and joint ventures.

ROW: Any fund with a geographic focus outside of North America and Western Europe.

ROW Equity: Includes all buyout, growth, and venture capital-focused funds, with a geographic focus outside of North America and Western Europe.

Secondary FoF: A fund that purchases existing stakes in private equity funds on the secondary market.

Seed/Early VC: A venture capital strategy that provides funding to early-stage startups.

Single Manager CI: A fund that invests capital in deals alongside a single lead general partner.

SMID Buyout: Any buyout fund smaller than a certain fund size, dependent on vintage year.

U.S. Mega/Large: Any buyout fund larger than a certain fund size that depends on the vintage year and is primarily investing in the United States.

U.S. SMID: Any buyout fund smaller than a certain fund size that depends on the vintage year and is primarily investing in the United States.

VC/Growth: Includes all funds with a strategy of venture capital or growth equity.

Venture Capital: Venture Capital incudes any PM fund focused on any stages of venture capital investing, including seed, early-stage, mid-stage, and late-stage investments.

Index Definitions

MSCI World Index: The MSCI World Index tracks large and mid-cap equity performance in developed market countries.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which is affecting markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot

be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of January 31, 2024