Secondaries have historically generated attractive returns and low volatility relative to other private markets strategies. In addition to providing investors with downside protection, secondaries have historically outperformed other primary private equity investments, making them a great complement to an investor’s overall portfolio.

Dispersion of Returns by Strategy

Vintage Years: 1979-2018, Ordered by Spread of Returns

Today’s Secondary Market Opportunity

Volatility has historically created a stronger opportunity set and it is this uncertainty that has us excited about the wave of opportunities to buy at attractive valuations on the secondary market.

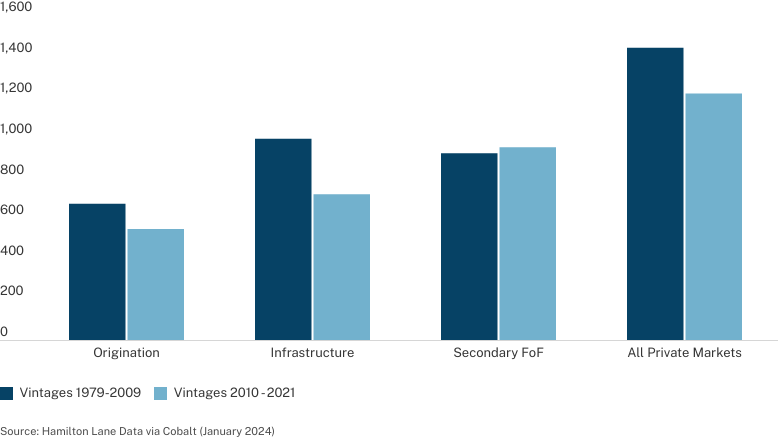

| Current Landscape | Current Market Opportunity |

|

|

|

|

|

|

|

1Source: Hamilton Lane Investment Database and Jefferies Secondary Update (July 2022)

Explore more of the trends and opportunities in the secondary market

Page 1: Strategy Definitions

Venture Capital: Venture Capital incudes any PM fund focused on any stages of venture capital investing, including seed, early-stage, mid-stage, and late-stage investments.

Growth Equity: Any PM fund that focuses on providing growth capital through an equity investment.

SMID Buyout: Any buyout fund smaller than a certain fund size, dependent on vintage year.

Mega/Large Buyout: Any buyout fund larger than a certain fund size that depends on the vintage year.

Real Estate: Any closed-end fund that primarily invests in non-core real estate, excluding separate accounts and joint ventures.

Secondary FoF: A fund that purchases existing stakes in private equity funds on the secondary market.

Infrastructure: An investment strategy that invests in physical systems involved in the distribution of people, goods, and resources.

Credit: This strategy focuses on providing debt capital.

Private Markets: Hamilton Lane’s definition of “All Private Markets” includes all private commingled funds excluding fund-of-funds, and secondary fund-of-funds.

This presentation has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this presentation are requested to maintain the confidentiality of the information contained herein. This presentation may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

Certain of the performance results included herein do not reflect the deduction of any applicable advisory or management fees, since it is not possible to allocate such fees accurately in a vintage year presentation or in a composite measured at different points in time. A client’s rate of return will be reduced by any applicable advisory or management fees, carried interest and any expenses incurred. Hamilton Lane’s fees are described in Part 2 of our Form ADV, a copy of which is available upon request.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: US SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under US laws, which differ from Australian laws.

Any tables, graphs or charts relating to past performance included in this presentation are intended only to illustrate the performance of the indices, composites, specific accounts or funds referred to for the historical periods shown. Such tables, graphs and charts are not intended to predict future performance and should not be used as the basis for an investment decision.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

The calculations contained in this document are made by Hamilton Lane based on information provided by the general partner (e.g. cash flows and valuations), and have not been prepared, reviewed or approved by the general partners.