The Devil Is in the Details: Middle-Market Infrastructure Investing

The French novelist Gustave Flaubert famously said, “le bon Dieu est le dans detail,” which over the years has been loosely interpreted to mean, “the Devil is in the details.” A perfectionist, Flaubert constantly strove to find “le mot juste,” or “just the right word” in his novels, sometimes occupying an entire week writing and rewriting a single page with an intense focus on detail.1 Why? To ensure that his writing was “rhythmic as verse, precise as the language of sciences, undulant, deep-voiced as a cello, tipped with flame: A style that would pierce your idea like a dagger, and on which your thought would sail easily ahead over a smooth surface, like a skiff before a good tail wind.”2

Never in our lives could we hope to write something so beautiful. But Flaubert was right, the Devil is most certainly in the details.

What does this have to do with investing? Or even infrastructure? As middle market-focused investors, we will endeavor to explain.

The Middle Market

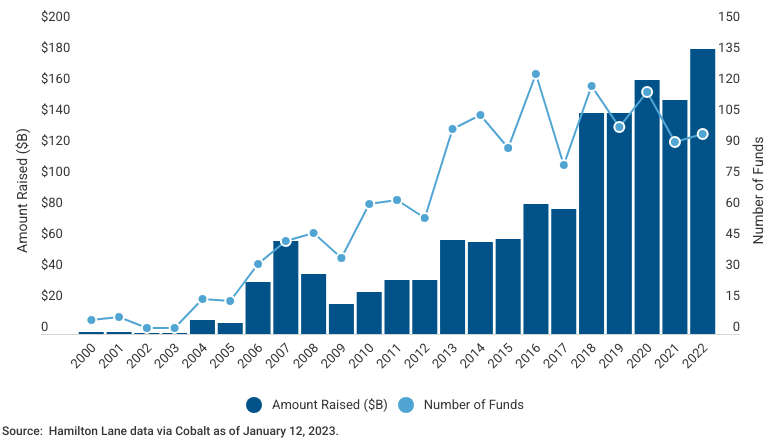

First, let’s look at fundraising in infrastructure private markets. It is well known that the market has expanded significantly since the early 2000s. As shown in the chart below, infrastructure fundraising has grown at an annualized rate of more than 24% over the last two decades.

Closed-End Infrastructure Fundraising - 2000-2022

During that period, infrastructure private markets matured and, as we have identified in prior missives, a fundamental shift occurred around 2016 when the size of infrastructure funds began to increase markedly. And, as the pools of capital increased, so too did managers’ focus on larger investments.

Despite infrastructure fundraising favoring larger and larger funds, the vast majority of transactions continue to take place in the lower and middle market. In fact, as shown below, 96% of transactions completed in 2022 were in assets with enterprise values below $2.5 billion, and 78% of transactions were in assets with enterprise values under $500 million. This has been the case for some time, and it’s no secret to investors. The lower and middle market represents a deeper pool of infrastructure opportunities for investment, at least in number.

Transaction Count By Size

In addition to depth and liquidity, the middle market can provide other attractive characteristics for investors, including the possibility of higher returns from the implementation of value-added business plans. These business plans are often more capex or operationally intensive and can involve more nascent asset or platform profiles compared to their larger peers. This can lead to transaction dynamics and key value drivers being somewhat different in large versus smaller deals. Let’s take a closer look at some examples based on our general observations of the market today.

Large versus Middle Market Comparison

First, in our view, many of the larger transactions we see today have greater exposure to the macro environment, which can include more demand cyclicality, and higher sensitivity to GDP growth as well as capital market risks. These macro risk exposures result from more established assets often commanding higher entry valuations with more limited operating levers available for deal sponsors to pull in order to add value. In contrast, many of the deals in the small to mid-market space appear to have more flexible options available in their tool kits to more effectively insulate them from certain macro risks. These value creation initiatives often include elements such as platform expansions, asset roll ups/aggregations, or build vs. buy on projects where the early-stage development risk has been sufficiently mitigated. In our view, greater market liquidity and a more intense focus on value creation should provide small to mid-market assets with better exit options and less reliance on multiple expansion.

To put some of this into context, we’ll compare two transactions reviewed by our team in the past few years. Both targets operate in the same telecom sector but have very different value creation profiles. Target A is a large company with an established asset base. The sponsor’s investment thesis focuses on leveraging its scale to capitalize on access to accretive financing and to enhance its strategic relevance to counterparties. In contrast, Target B is a smaller company where the sponsor’s investment thesis revolves around driving upside through aggressive leasing of existing assets and creating a larger portfolio through the execution of a pre-specified, often pre-contracted, but capex-intensive, growth pipeline. The success of an investment in Target A is driven by access to capital markets and valuations in the sector, while Target B’s value creation relies more on operational enhancements, site aggregation and platform growth.

Both assets have similar risk profiles, but the base case return for middle market Target B is higher, and its value creation depends on strategy execution that is more influenced by the decisions made by the deal sponsor than by exogenous market factors.

Comparison of Middle Market Deals

We know what you’re thinking: You don’t need to read any further – you’re ready to put all of your infrastructure capital into small to mid-market opportunities. We like your enthusiasm, but hold that thought for just a second: Simply switching allocation from large to middle-market transactions is, of course, no guarantee of higher returns. As we have said, the smaller end of the market is larger (by number), often less mature, and assets require greater attention from sponsors. And while investors recognize the opportunity this presents, this can also heighten deal and sponsor selection risk – all of which is to say, one cannot simply carve out capital for the middle market and expect higher returns.

Let’s compare two middle-market opportunities as an example. Revisiting Target B and comparing it against another middle-market opportunity in the same sector, Target C, we see a similar investment thesis focused on i) aggressive leasing to increase tenancy rates for individual towers; and ii) platform expansion through the execution of a growth pipeline. But this where the similarities end.

As we dig into the details, we see a different approach to assumptions and to what the transaction sponsors need to “get right” for the investment thesis to play out as planned. Generally speaking, the success of an investment in Target B relies on a more conservative set of assumptions, whereas Target C is a bit more aggressive:

Middle Market Comparisons

As shown, Target C assumes higher tenancy growth rates, co-tenancy rental rates and rent escalators; all of this while assigning lower operating expense assumptions and having less of its new assets pre-contracted at the time of construction, thereby introducing greater merchant risk.

Of course, any transaction has a wide range of factors and variables to consider, and the above examples are just a few of many. We could also go on into other aspects, but suffice it to say that investors interested in the middle market need to fully understand the idiosyncrasies of the sectors in which they operate, dig into the assumptions and appreciate the nuances of each transaction to ensure they have a full picture of the risks being assumed in chasing the target return. Some investors may be well equipped to do this on their own, but for others, a successful middle market investment program needs a partner with:

- Deal Flow – The ability to see the entire market;

- Scale – Sufficient resources to review the vast number of opportunities; and,

- Experience – Proficiency across sectors.

The middle market surely presents opportunities, but as Flaubert suggested, “le bon Dieu est le dans detail.”

2Flaubert, Gustave. The Letters of Gustave Flaubert 1830–1857. Translated by Steegmuller, Francis.

There are a number of factors that can affect the private markets which can have a substantial impact on the results included in this analysis. There is no guarantee that this analysis will accurately reflect actual results which may differ materially. These valuations do not necessarily reflect current values in light of market disruptions and volatility experienced in the fourth quarter of 2020, particularly in relation to the evolving impact of COVID-19, which is affecting markets globally.

The information contained in this presentation may include forward-looking statements. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable but the accuracy of such information cannot

be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorized and regulated by the Financial Conducts Authority. In the UK this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws. The PDS and target market determination for the Hamilton Lane Global Private assets Fund (AUD) can be obtained by calling 02 9293 7950 or visiting our website www.hamiltonlane.com.au.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

As of February 21, 2023