Currency Effects on Private Market Portfolios

Investment returns for a private markets portfolio (or for that matter, public markets portfolio) are a derivative of a number of variables. In the current market environment, for example, rising rates, inflation, geopolitical risks, supply chain issues (to name just a few) -- have all led to broader market volatility that in turn impacts an investor’s portfolio return. For a minute, let’s assume we have all that covered and the portfolio manager has picked just the right investments, generating returns in line with their target. For an international investor, there is still one other factor that can be the shifting sands for their overall return – the currency fluctuation.

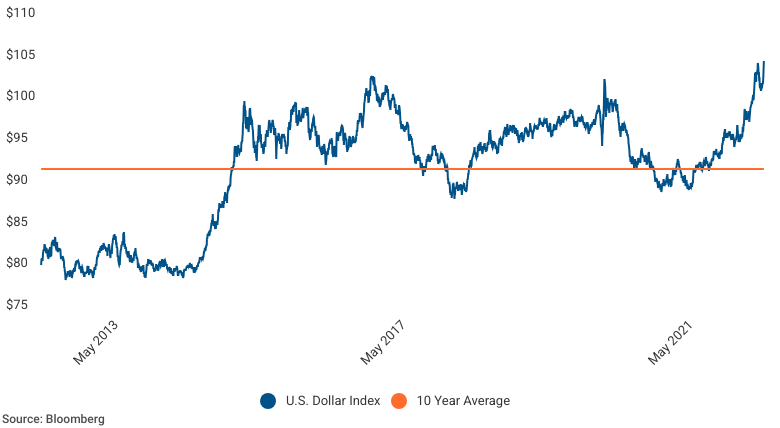

More recently, we have witnessed the USD strengthen overall against other currencies. To put it into perspective, the U.S. Dollar Index, which indicates the general international value of the USD by averaging the exchange rates between the USD and major world currencies, touched a 10-year high this summer. For non-U.S. investors allocating capital to a USD-denominated fund, this would be beneficial for the return profile as they would have invested in a currency that strengthened against their home currency. The opposite would be true for U.S. investors, investing in non-USD funds. However, the currency fluctuation can go either way, swinging the overall returns one way or the other. Over the last decade, the year-on-year change for the Dollar Index has ranged between -12% to +26%. To put it in context, the average IRR for the private markets over this period has been around 15.4%, illustrating that the currency fluctuation could either lift up or wipe off the underlying portfolio returns on an annual basis.

U.S. Dollar Index

Given the potential risk of adverse currency moves, it is natural for investors to seek a solution. We regularly field investors’ questions around hedging currency fluctuations in their private markets portfolios. This typically happens after a given investor’s home currency has appreciated, resulting in a currency adjustment loss on their foreign holdings. Most inquiries are general in nature: “What are the options for currency hedging?”; “What are the benefits and costs?”; and the most common, “How do others deal with this?”

Currency hedging is very common in other asset categories, such as tradable fixed income. Here, the asset characteristics are more favorable to placing a currency hedge. When a fixed income investor purchases a non-callable foreign bond, the investor can match the maturity and principal amount of the hedge to that of the bond. High-quality bonds exhibit low volatility in local currency terms, so most of the risk to a foreign investor comes from the currency impact. A high-quality bond trading in a liquid market could be used to collateralize the hedge, and any losses on the hedge could be offset by comparable currency gains on the principal of the bond.

The characteristics of private asset portfolios are, of course, very different from tradable fixed income, however. With private markets portfolios, challenges of hedging are greater and the potential benefits – net of costs – are hard to assess. As a result, in our experience most investors either do not implement a large-scale currency hedging program on their private markets portfolios at all, or will rely on the GP to do so.

Examples of Currency Hedging Effects in Different Asset Classes

- Tradable Fixed Income

- Known maturity and principal amount of bonds

- Most volatility comes from currency component

- Many bonds can serve as collateral for hedge

- Bonds can be sold to cover hedge loss – gain on the bond offsets hedging loss

- Private Assets

- Uncertain timing and amount of cash flows

- Most volatility comes from equity and asset-specific risk

- May need to post cash collateral on hedge which creates a drag on returns

- May need to call additional cash to cover hedge losses

But for those keen on exploring how to think about currency hedging within their private markets portfolio, we’ll address some common questions.

How much and how far out do I hedge?

Investors can enter a hedging transaction by purchasing an option or entering a forward contract. In either case, the investor must determine how much currency exposure to hedge and for how long. This matches well to the nature of fixed income investments, but not to private markets investments. In most cases when an investor makes a private markets investment, he or she has only a rough idea of the exit timing and just a best guess on exit proceeds. This creates an inevitable mismatch of timing and size between the hedge and the underlying investment.

While this mismatch is an important source of residual risk, it is not the only challenge to placing an optimal hedge. An investor cannot fully quantify their currency exposure by simply looking at the reference currency of the fund, since the GP may make unhedged investments in other jurisdictions. Even assessing the corporate headquarters location of a portfolio company does not uniquely determine that company’s exposure to currency movements. A company could have significant export revenues or even operations overseas. In an extreme example, a Belgian company who reports its financials in Euros may nonetheless see both its raw material inputs and its exported outputs priced in USD. An investor who hedges based purely on the reference currency of a fund or even the locations of portfolio companies could overestimate or underestimate the optimal hedge.

How big is the risk reduction?

The goal of any hedging transaction is reduction of portfolio risk, so it is worth assessing how much risk reduction actually can be achieved. Let’s go to our example of a global bond investment, where we observe that currency fluctuations drive the bulk of volatility in such portfolios. This is because high-quality bonds have relatively low volatility in local currency terms. This is not the case in most private equity investments, where the dispersion of potential return outcomes is much broader.

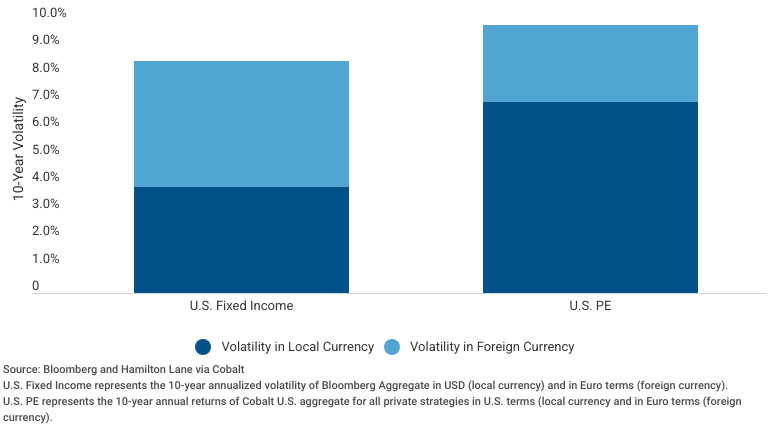

Hedging currency only addresses one source of risk in the portfolio. Among developed markets investments, the volatility seen by a global investor may not be much greater than that of local investors. In the example of a Europe-based investor with capital allocated to U.S. private equity, they saw 28% of the annual volatility come from currency fluctuation in the last 10 years, with the remaining 72% reflected in the local currency returns of PE. Even when one hedges the currency component, the investor is still exposed to the equity risk.

Portion of Volatility from Currency Movements

How much does currency hedging cost?

Whether a private markets investor decides to use forward contracts or options, hedging can be costly.

Forward contracts can compensate for adverse moves in the currency, but if the currency moves in the opposite direction, the investor will have to post cash collateral for the unrealized loss on the hedge. Even if the counterparty extends credit to the investor for collateral purposes, any losses need to be settled in cash at the expiration of the hedge. At that time, it may not be possible to sell the private assets for an offsetting profit.

Long positions in options can allow an investor to forego potentially large hedging losses, but they require cash upfront to pay option premiums. Private markets investing is already cash-inefficient for an investor given the nature of capital calls and distributions, so funding a hedging program would be another draw on portfolio liquidity, and the costs could provide a drag on overall returns.

The cost of hedging using forward contracts depends on two key factors:

- Interest Rate Differential: Put another way, the difference in short-term rates in the home and foreign currency. Investors looking to hedge their foreign currency exposure pay the foreign currency interest rate and receive the home currency interest rate. That means investors whose home currency is lower yielding compared to the foreign currency will incur a cost of hedging due to this rate differential and vice versa.

- Currency Basis: The incremental cost over and above the interest rate differential that is a function of supply and demand across currencies.

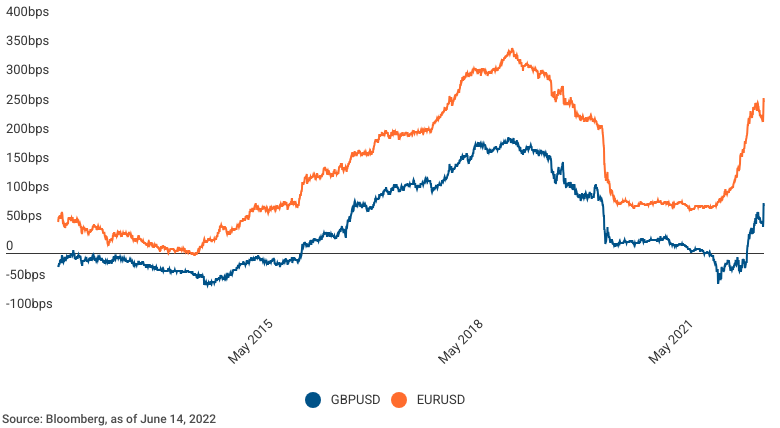

With the central banks raising rates that are not necessarily in sync with those of other economies, the interest rate differential between currencies tends to widen, increasing the cost (or benefit) of hedging depending on the direction of the hedge. In the current market environment, with Fed currently raising rates at a faster pace than other central banks, it is becoming more costly for non-U.S. investors to hedge their USD investments back to home currency. A French investor hedging its USD exposure back to EUR would currently pay approximately 260 basis point per year for the risk reduction. Ouch! The chart below illustrates this for GBP and EUR.

Cost of Hedging 12-Month exposure

Private Markets for the Long Term

If an investor is able to lock up a portion of their overall assets for five or more years of illiquidity, then perhaps daily or even quarterly volatility is not the most relevant risk measure. In terms of currency exposure for investors, the typical five-year holding period for private investments may understate the true time horizon. For an investor wishing to maintain exposure to the major global economies, any distribution from a maturing investment is likely rolled into a new commitment in the same geography. This stretches the true investment horizon to decades. Many investors find that over this extended time horizon, the costs of hedging outweigh the risk reduction gains.

What to do?

Of course, even investors with a long-term focus often are assessed on their results over much shorter intervals. But given all of the challenges of hedging, what are private markets investors to do about currency risk? We believe it is still possible to be thoughtful about how to approach the risk of cross-currency private investments.

Institutions assess their private asset performance relative to their benchmark, which is typically an index of listed assets plus a premium for illiquidity. Investors should be thoughtful in selecting a benchmark with similar exposures to geography and currency as the expected portfolio. For example, a German investor building a global private markets portfolio might select the MSCI All Country World Index total returns in euros as the basis of the benchmark. That way, any currency movements that will impact the private portfolio won’t lead to relative underperformance, since they also will be reflected in the benchmark.

Assessing risks to absolute returns, rather than benchmarking relative returns, is still a tricky matter. Most investors that choose not to hedge instead underwrite the expected returns and the risk of a private investment in the reference currency of the investor. Specifically, a U.S. investor in a Brazilian fund would assess the risk of the investment in USD over the holding period.

On some occasions, the amount and timing of private market cash flows are known within a narrow band where currency hedging may make sense. For example, a European GP who has agreed to sell a U.S. asset in four months may seek to hedge the risk of a sharp currency move before closing. In this example, the exception proves the rule. Here, the GP has a known sale price, and the short duration limits the cost of hedging. Also, to the extent the investment has grown to a significant portion of the fund, currency mismatch may be a significant driver of overall fund risk. Such hedging at the GP level represents the bulk of what we see in private investments.

Over the last few years, we have also seen the emergence of open-ended structures in the private markets space with hedged share classes offered in multiple currencies. With the investor base for these typically targeted to smaller institutions and wealthy families that are more sensitive to currency fluctuation, it is common practice to have some form of hedging program in place to minimize the investor’s currency risk, similar to what is typically witnessed in the mutual funds space.

In summary, while the benefits of hedging can be obvious and overstated in hindsight, most long-term private markets investors still find that costs, liquidity drag and complexity outweigh the potential risk reduction benefits of hedging their LP portfolios. On the other hand, GPs with clearer visibility of the near-term exposure and open-ended structures with multi-currency share classes tend to hedge out some portion of the FX exposure.

This presentation has been prepared solely for informational purposes and contains confidential and proprietary information, the disclosure of which could be harmful to Hamilton Lane. Accordingly, the recipients of this presentation are requested to maintain the confidentiality of the information contained herein. This presentation may not be copied or distributed, in whole or in part, without the prior written consent of Hamilton Lane.

The information contained in this presentation may include forward-looking statements regarding returns, performance, opinions, the fund presented or its portfolio companies, or other events contained herein. Forward-looking statements include a number of risks, uncertainties and other factors beyond our control, or the control of the fund or the portfolio companies, which may result in material differences in actual results, performance or other expectations. The opinions, estimates and analyses reflect our current judgment, which may change in the future.

All opinions, estimates and forecasts of future performance or other events contained herein are based on information available to Hamilton Lane as of the date of this presentation and are subject to change. Past performance of the investments described herein is not indicative of future results. In addition, nothing contained herein shall be deemed to be a prediction of future performance. The information included in this presentation has not been reviewed or audited by independent public accountants. Certain information included herein has been obtained from sources that Hamilton Lane believes to be reliable, but the accuracy of such information cannot be guaranteed.

This presentation is not an offer to sell, or a solicitation of any offer to buy, any security or to enter into any agreement with Hamilton Lane or any of its affiliates. Any such offering will be made only at your request. We do not intend that any public offering will be made by us at any time with respect to any potential transaction discussed in this presentation. Any offering or potential transaction will be made pursuant to separate documentation negotiated between us, which will supersede entirely the information contained herein.

Certain of the performance results included herein do not reflect the deduction of any applicable advisory or management fees, since it is not possible to allocate such fees accurately in a vintage year presentation or in a composite measured at different points in time. A client’s rate of return will be reduced by any applicable advisory or management fees, carried interest and any expenses incurred. Hamilton Lane’s fees are described in Part 2 of our Form ADV, a copy of which is available upon request.

The following hypothetical example illustrates the effect of fees on earned returns for both separate accounts and fund-of-funds investment vehicles. The example is solely for illustration purposes and is not intended as a guarantee or prediction of the actual returns that would be earned by similar investment vehicles having comparable features. The example is as follows: The hypothetical separate account or fund-of-funds consisted of $100 million in commitments with a fee structure of 1.0% on committed capital during the first four years of the term of the investment and then declining by 10% per year thereafter for the 12-year life of the account. The commitments were made during the first three years in relatively equal increments and the assumption of returns was based on cash flow assumptions derived from a historical database of actual private equity cash flows. Hamilton Lane modeled the impact of fees on four different return streams over a 12-year time period. In these examples, the effect of the fees reduced returns by approximately 2%. This does not include performance fees, since the performance of the account would determine the effect such fees would have on returns. Expenses also vary based on the particular investment vehicle and, therefore, were not included in this hypothetical example. Both performance fees and expenses would further decrease the return.

Hamilton Lane (Germany) GmbH is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (Germany) GmbH is authorised and regulated by the Federal Financial Supervisory Authority (BaFin). In the European Economic Area this communication is directed solely at persons who would be classified as professional investors within the meaning of Directive 2011/61/EU (AIFMD). Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane (UK) Limited is a wholly-owned subsidiary of Hamilton Lane Advisors, L.L.C. Hamilton Lane (UK) Limited is authorised and regulated by the Financial Conduct Authority (FCA). In the United Kingdom this communication is directed solely at persons who would be classified as a professional client or eligible counterparty under the FCA Handbook of Rules and Guidance. Its contents are not directed at, may not be suitable for and should not be relied upon by retail clients.

Hamilton Lane Advisors, L.L.C. is exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 in respect of the financial services by operation of ASIC Class Order 03/1100: U.S. SEC regulated financial service providers. Hamilton Lane Advisors, L.L.C. is regulated by the SEC under U.S. laws, which differ from Australian laws.

Any tables, graphs or charts relating to past performance included in this presentation are intended only to illustrate the performance of the indices, composites, specific accounts or funds referred to for the historical periods shown. Such tables, graphs and charts are not intended to predict future performance and should not be used as the basis for an investment decision.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

The calculations contained in this document are made by Hamilton Lane based on information provided by the general partner (e.g. cash flows and valuations), and have not been prepared, reviewed or approved by the general partners.

As of 6/30/2022