You’ve no doubt heard about or read about the ever-declining number of public market stocks available to investors today. For instance, the Wilshire 5000 Index used to contain 5,000 stocks; today that number is closer to 3,500. With this decline in the opportunity set for investors in public markets, many are turning to the private space to access not only a wider range of opportunities, but perhaps also capture some of the potential outperformance that has frequently been synonymous with the space.

While more and more investors are flocking to private markets, the dynamics are often very different than those of the public markets. For investors trying to conduct due diligence on funds in this asset class, you’ll want to adjust some of the questions you ask and characteristics you look for to ensure you are able to select managers who have the potential to deliver strong returns. This article is the first in a brief series that will touch on some of the differences in investing in public vs. private markets. It will also endeavor to offer some practical questions to ask as you are researching private markets strategies, which are those that provide access to the asset class but have more liquidity than traditional private funds. We will discuss deal flow (and why it matters as much as it does), performance and outlook of public vs. private markets, and some of the challenges associated with traditional drawdown structure funds.

A Large and Inefficient Opportunity Set

An overwhelmingly large percentage of companies are private, resulting in what equates to be a substantial opportunity set, albeit one that brings significant challenges. Despite the size of the deal market on the private side, it is not always an even playing field, and not nearly as efficient as the public markets. Informational advantages – largely achieved through scale and relationships – do exist and may be one factor that separates those who outperform and deliver on the promises of private market general partners.

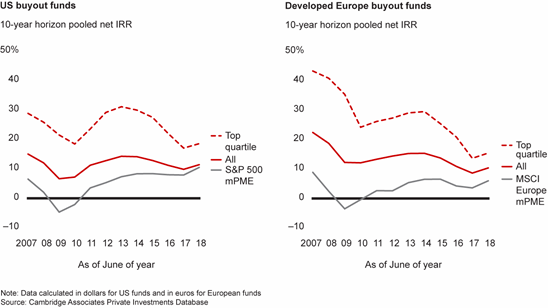

As the private equity buyout market has matured, you’ll notice in the U.S. vs. Developed Europe buyout funds charts that the average trend line of returns has decreased. And although Developed Europe buyout IRRs, in particular, have dropped from 2008, the spread over the public markets has remained healthy.

Past performance is not indicative of future results.

Source: Bain - Global Private Equity Report 2019

The longer-term trend of decreasing returns makes sense, as more capital flows to the asset class, deal valuations get driven up and generating alpha becomes increasingly difficult. Managers and investors often state that the high transaction multiples represent the biggest challenge at present. As you can see, this is a valid concern.

Past performance is not indicative of future results.

Source: Bain - Global Private Equity Report 2021

Unpacking the Top Quartile

Anyone who operates in the private markets knows that asset managers tout their meaningful deal flow as a competitive advantage. Given that, it’s imperative to look under the hood and unpack what specific advantages a manager’s deal flow is really creating. There has been no shortage of deals, but there is a limited number of good deals, and it’s often the case that the best deals are not undertaken through a competitive bidding process. Instead, they are going to be carried out in partnership with managers who have scale, relationships and access. That is a big reason why the outperformance has generally continued to persist for top-quartile managers. The importance of manager selection and portfolio construction cannot be overstated. When conducting due diligence in this space, a few key questions advisors should be asking asset managers are: ‘What is your breakdown of deal flow by each investment type and strategy? Credit? Co-investments? Secondaries?’ and ‘Where is the main source of your deal flow?’

Despite the growing opportunity set and new entrants coming into the space, top-quartile managers continue to find ways to set themselves apart, as is evidenced in the U.S. and Developed Europe Buyout Funds charts shown earlier. Finding attractive valuations continues to present a challenge, however, so one way for managers to ensure they can find what they believe to be the best deals is by having access to the most meaningful deal flow. Ultimately, a manager wants to be in the enviable position of seeing a lot but doing only a little. There is a clear correlation between those managers with good deals and those managers generating strong performance and claiming the coveted top-quartile spot.

It is important to note that the difference is wider between competing firms within the private markets vs. competing firms within the public markets. This dynamic speaks to the efficiency of the public markets, where all information is publicly available, thereby creating a level playing field. Larger firms in the public space certainly have some advantages over smaller firms, but those are narrower. On the other hand, having scale in the private markets often equates to substantial competitive advantages over subscale competitors.

The private markets are highly fragmented, providing a significant informational advantage for those who possess the resources and have the access to utilize it. For those lacking these attributes, the private markets can be a very challenging space. With information and the ability to synthesis it efficiently, resourced firms tip the scales in their favor in underwriting and can stay away from overpriced and inferior deals.

Performance Over Time

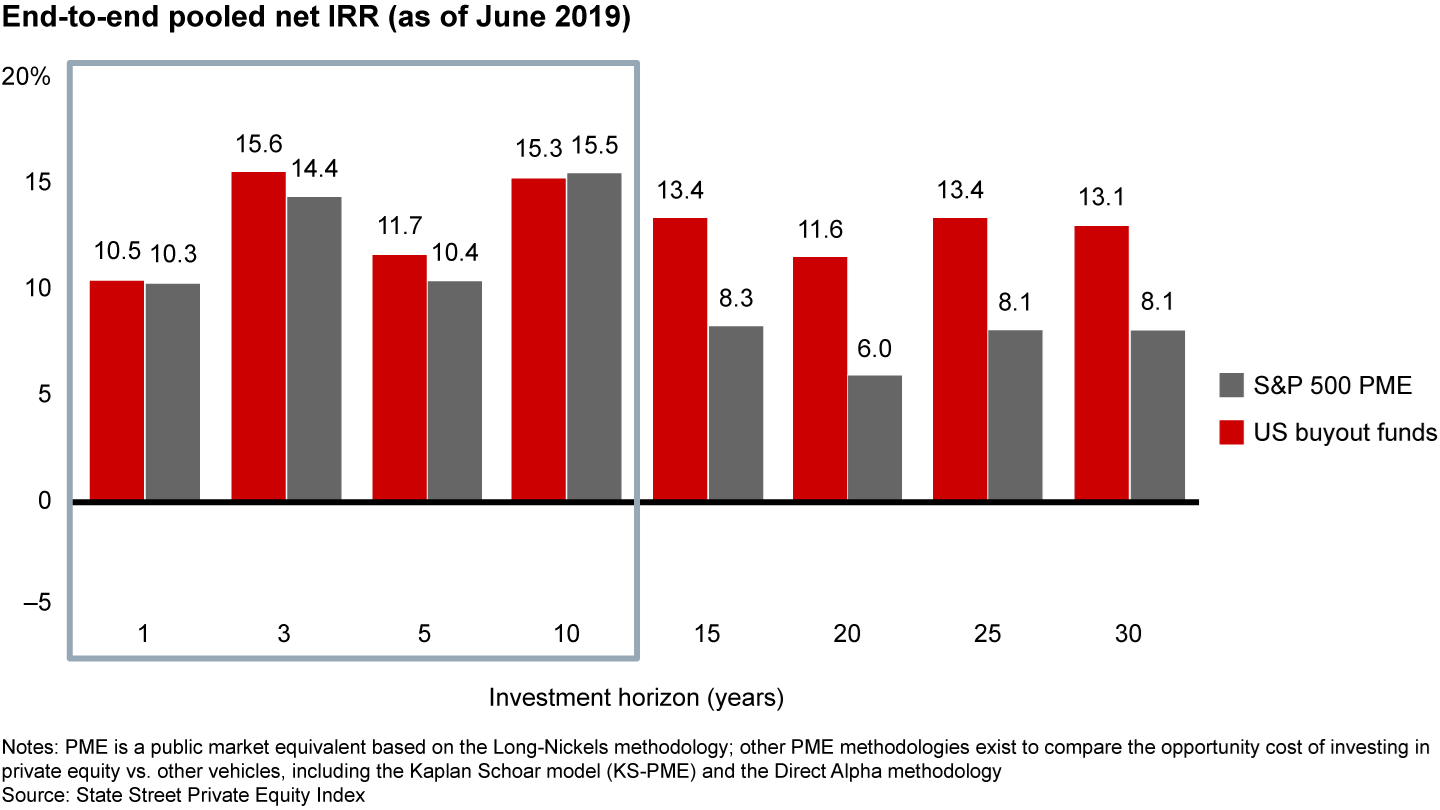

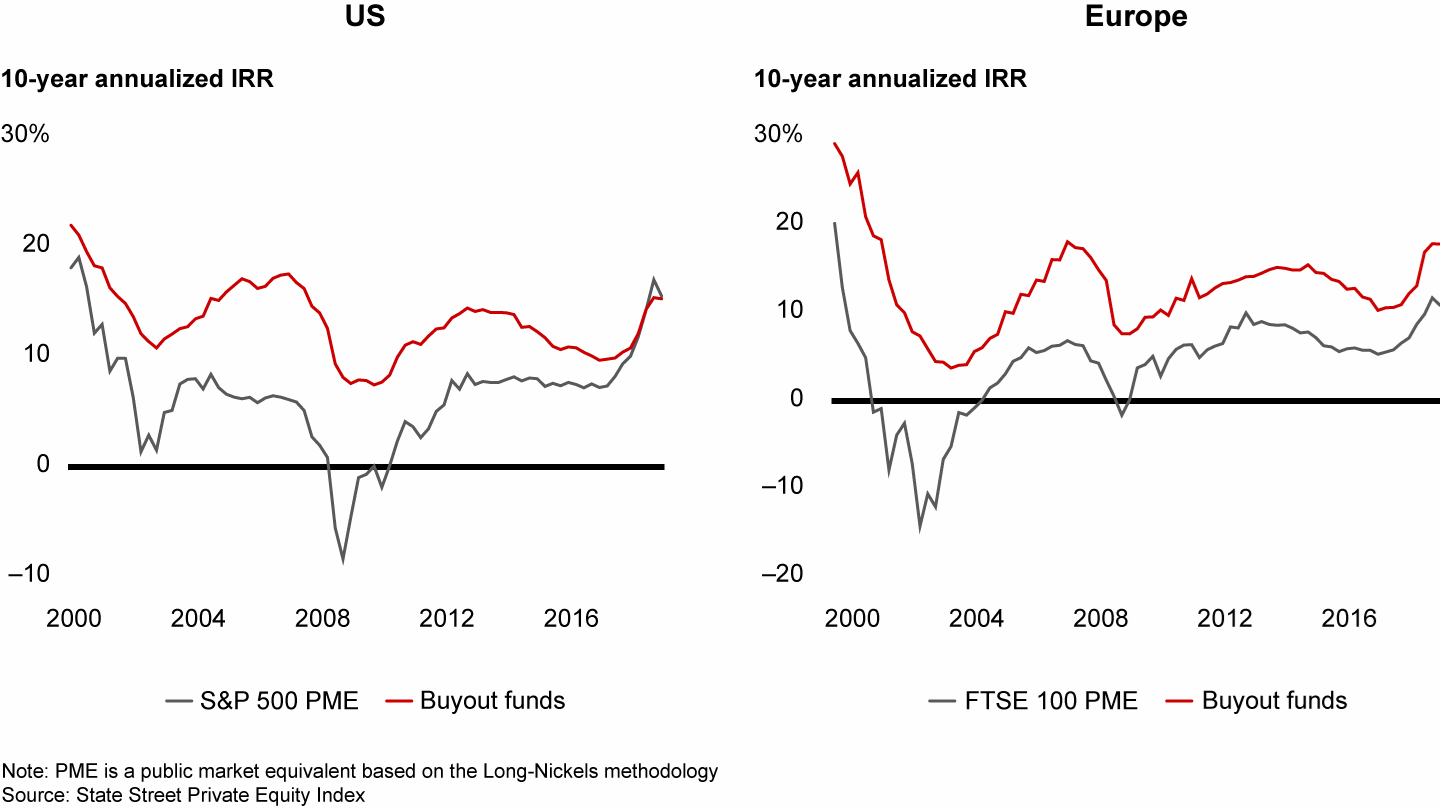

Let’s talk a bit more about performance. Over longer time periods, private equity has outperformed other equity-based assets on an absolute and risk-adjusted basis. But, when we look at shorter time periods, the outperformance isn’t as significant, primarily due to the public market’s recent strong performance.

Past performance is not indicative of future results.

Past performance is not indicative of future results.

Source: Bain - Public vs. Private Equity Returns Article

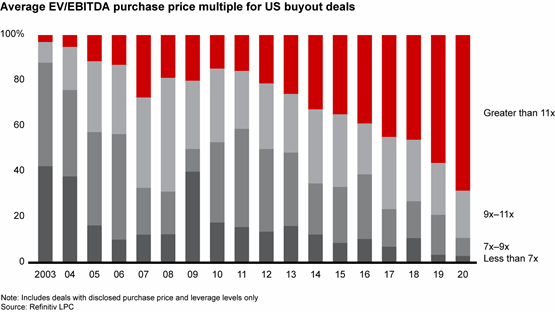

Interestingly, when looking at the figure below, the top-quartile manager performance trend line has remained steady as transaction multiples have been pushed up. This demonstrates why top-tier managers have continued to see substantial inflows as they have the access to high-quality deals that still drive returns even if they are paying up. Thinking about this another way, manager and fund count has grown significantly, so there are more managers in the quartile, but the other quartiles’ performance has suffered pointing to an increased manager dispersion, making manager selection even more critical. This is a significant differentiator as boutique managers may have some niche specialization, but they often simply do not get access to the quality high-profile deals.

Past performance is not indicative of future results.

Source: Bain - Public vs. Private Equity Returns Article

Traditional Private Market Structures

Traditionally, the private markets have been accessed through commingled funds. These structures present a few challenges for retail investors especially as they tend to have higher minimum investment amounts, which can make it difficult for individual investors to diversify across strategies and vintage years. Within these traditional structures, investors commit capital and then wait for the general partner to call or draw down their capital when needed. This presents another challenge in the way of liquidity management as investors must essentially maintain some level of liquidity to meet capital calls. This potentially leads to cash drag on time-weighted portfolio returns.

All of these factors are exacerbated further by the fact that traditional private markets partnerships are getting longer. Though funds are often assumed to be from 8 to 10 years, data from Pitchbook states that it often takes 11 to 14 years for a PE fund to reach an RVPI (residual value to paid) of less than .05x, which potentially increases risk for investors.

Staying Private

More and more, we see good companies choosing to remain private for longer, effectively expanding the opportunity set for private market investors. Access to capital for private companies has improved dramatically as the private markets have matured; in fact, Cobalt LP reported that 20 years ago there were 1,551 funds and 1,031 fund families in the private markets, whereas as of November 2020 there were roughly 11,769 funds and 7,681 fund families. The growth of available investment capital helps to alleviate the need for companies to go through a public listing process. In short, companies have a lot more options today than they had in the past.

For those that do choose to go public, they tend to be doing so much later in their lifecycle. Staying private longer means that a great deal of the growth and value creation is taking place while private. By the time companies go public, they are increasingly in a much more mature phase than had been the case historically.

Outlook Ahead

Given the meaningful opportunity set and the compelling dynamics outlined above, we believe the interest in and outlook for the private markets may continue to be strong. We anticipate that capital may continue to flow to the private markets at an increasing rate – this, of course, begs the question, “What about all the dry powder?” Capital overhang, or dry powder, in private markets is often cited as a concern; however, we believe a far more relevant metric is how quickly private markets managers are putting that capital to work.Evidence exists to suggest that private equity managers are in fact deploying capital in a healthy time frame. If assets are moving into the space and deals are getting done efficiently, there is potential for strong performance.

With that, we wrap our discussion of the various potential benefits of and outlook for the private markets, as well as the explanation of why scale, relationships and expertise really matter when it comes to investing in the private markets. In subsequent articles, we’ll delve into the structures and suggest some things to consider and questions to ask as you research the space.

Disclosures

The views expressed are those of the author at the time created. These views are subject to change at any time based on market and other conditions, and Hamilton Lane, disclaims any responsibility to update such views. No forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of trading intent on behalf of any Hamilton Lane portfolio.

This Hamilton Lane blog is not intended to provide investment advice. This blog should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security by Hamilton Lane, or any third-party. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your legal or tax professional regarding your specific situation.