Private Markets Due Diligence: Investment Strategies and Fund Structures

As showcased in the first blog in our series discussing private markets, the opportunity set within the asset class is large and inefficiencies exist that ultimately can lead to outsized risk/return characteristics. However, in what is an increasingly complex industry, not all private market investment opportunities are created equal. Not unlike the public markets, there are various ways in which investors can access the asset class (e.g., equities versus credit strategies, primary investing vs. direct investing) and different asset allocation mixes naturally produce different risk/return profiles. Additionally, fund structure itself can create different return characteristics as a result of what is/is not included in a given portfolio. As if private market investing wasn’t complicated enough…

…the landscape of funds within the private markets is vast, as are the available options within each sector. Over 4,600 private market investment firms have raised a fund in the past decade, and we expect the private markets landscape will continue to grow and diversify.1 Success in this asset class requires not just a healthy understanding of the various strategies available across the investment spectrum, but also the ability to then access those funds, managers, and/or deals that are most appealing. Unlike the public markets, access is not necessarily created equal within the private market landscape.

What follows is an exploration of the different forms of private market investing: primary fund investments, direct/co-investments, secondaries, real estate/real assets available to institutional and non-institutional investors alike. Liquidity considerations must also be understood when investing in the private markets.

Primary Fund Investments

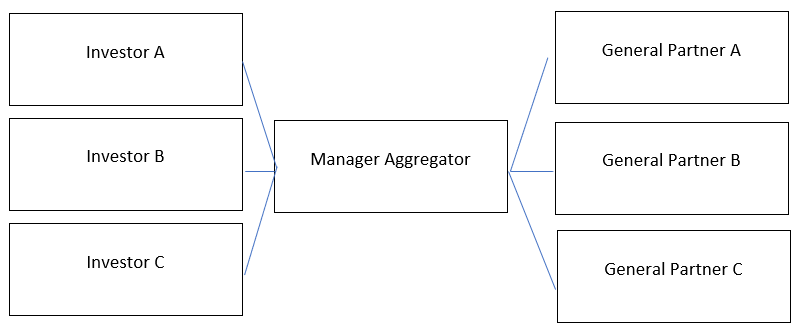

One may think about this as a bit of a history lesson in private equity investing, but that is not the case. Primary investing, though, has been around for some time and is a great way for investors to access a diversified portfolio of private market investments. This can be achieved via an individual investor targeting various primary funds on their own or instead utilizing a ‘fund-of-funds’ approach, which is a streamlined way for an individual investor to access the primary fund market in a single allocation (as shown below and similar to the hedge fund world). Generally, under the fund-of-funds model, the aggregator of capital also becomes the single-point allocator of capital. Specifically, an asset management firm/aggregator will seek to find best-in-class private markets managers – or General Partners – in which to allocate capital.

This model provides asset diversification and risk reduction in that idiosyncratic risk is reduced. Take this example: If a fund-of-funds allocates to ten underlying private market specialists that each have ten investments in their respective portfolios, that fund-of-funds now has exposure to 100 different private company investments. However, that diversification does come at a cost and, namely, through double-layer of fees.

In the traditional fund-of-funds approach, not only is the aggregator of capital charging (in most cases) a management fee and a performance fee, but so are the underlying manager’s primary funds. Yes, there are negotiations that can occur to help mitigate those fees, but generally there are elevated levels of fees associated with these structures. Not that those fees are unwarranted, however, as you are relying on the investment selection and due diligence expertise of the asset manager to identify top tier private market funds/General Partners to strive to generate meaningfully outsized returns.

Within the confines of conducting due diligence on primary investment managers, understanding portfolio construction is critical. That is, where will dollars be allocated across sectors, industries, business cycles, geographies and within the capital structure of an organization, are all important discussion points outside of the obvious question, “Where and how will the returns be generated?”.

Direct/Co-Investments

While investing in primary funds is one way to access the private markets, another approach involves allocating capital directly to private companies outside of a primary fund structure. Direct private investments and co-investments alongside a General Partner are exactly what they sound like – taking an investment position in a private company’s equity or credit, thereby circumventing a fund structure. In the case of a co-investment, that typically involves a minority purchase of equity or credit, completed alongside another private market-focused General Partner (i.e., there are two or more investors in a given transaction). Therefore, there are direct private equity investments, direct private credit investments, and similar terminology for co-investments (i.e., direct private equity co-investments, etc.).

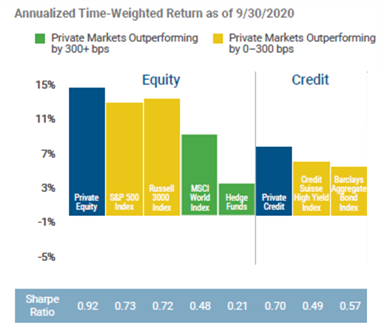

In terms of risk/return profile, one should expect a higher return for a direct equity investment versus a credit investment. By nature, credit investing is more “senior” to equity in a company’s capital structure and therefore, has greater downside protection and repayment priority compared to equity investors. For that seniority, one would typically expect a lower absolute return when compared to equity. That said, equity investors demand a higher return for inherently taking on greater risk. The chart below helps illustrate this point.

10-Year Asset Class Risk-Adjusted Performance2

Source: Hamilton Lane Data, Bloomberg (January 2021)

As one can see, private equity has, for the last 10 years on an annualized basis, outperformed private credit investments. Also, important to note is that both have outperformed public market peers over the same time frame. Why do these return profiles exist? Inefficiency and deal flow are integral pieces to that answer. Not only are the private markets inefficient, which allows for information asymmetry, but also that inefficiency is provided most notably through a network that provides access to interesting investment opportunities.

An important point to consider when comparing direct investing to primary investing – there are typically reduced or even no management fees/performance fees under the direct/co-investment strategies. While there may be fees at the asset manager level, these generally do not exist at the underlying private company investment level. In the context of determining capital allocation to private equity or private credit manager, clearly the risk/return profile is different and, therefore, should be considered in a total portfolio context as to what and where to invest private market dollars, alongside trying to isolate a top-quartile performer.

Secondary Investments

Secondary investing has the potential to provide meaningful and rather immediate upside to a portfolio. A secondaries transaction is one where an existing Limited Partner in a primary fund investment would like to, at some point during the fund’s life, exit that investment. By nature, in a secondary transaction, there is a seller seeking to exit their existing LP commitment for a reason: a life event, distress, liquidation, portfolio rebalancing, etc. Given private market investing – particularly a primary fund – is inherently illiquid, that seller cannot liquidate as is the case with a public market investment or even a hedge fund (with some notice period). When this situation occurs, a new buyer can typically acquire that “position” at a discount. In some cases, a steep discount depending on the seller’s motivations. That discount can create immediate upside performance where the existing NAV is the most appropriate valuation for that position (i.e., there is an instant mark-up from the discount to the current NAV at purchase). Take the below chart as an example.

.png)

The above chart illustrates a secondary transaction whereby one can acquire an investment at a 25% discount. The left side of the chart shows the position of the existing Limited Partner that is seeking to exit their investment. This would be considered a mostly funded investment, as there is $13 million invested with $2.8 million in unfunded capital. The right side of the chart shows the acquirer’s side of the transaction. As one can see, the acquirer is able to purchase the existing $13 million position for $9.8 million, which is a 25% discount to the current NAV. That 25% is immediate performance to the acquirer, as the position is marked to the current NAV post-acquisition, which is the selling party’s NAV.

An important point that should not be dismissed when looking at secondaries transactions is the remaining duration of the funds’ life. That is, when purchasing a secondary, the fund has been in existence for some time (e.g., purchasing midway through a primary fund’s 10-12 year life). By acquiring an existing position through a secondary transaction, one can mitigate J-curve risk. (The J-curve typically occurs during the investment phase of a traditional private equity fund, when the primary fund is charging fees and the investment portfolio is being accumulated over the course of the initial several years. As such, an investor may see a pronounced drawdown of capital – for fees and new investments - which can generate negative overall fund returns until the underlying investments begin to perform over time). Through a secondaries transaction, if one acquires a position later in the fund’s life cycle, the J-curve can be avoided altogether. The fund is more fully deployed, assets accumulated and can be in a position to be generating positive performance. These are important considerations when viewing secondaries transactions and secondaries managers. As noted in our first due diligence blog in this series, having a robust network and deal flow is important in isolating interesting secondary investment opportunities.

Real Estate/Real Assets

While the focus of this piece has been largely around the mechanics of investing in private companies through various fund structures, real assets can play an important role in a diversified private markets portfolio. There are various types of real asset investments, including real estate, precious metals, commodities, land and natural resources. The opportunity set within real assets is large, so allocating to any one single part of the market requires an area of expertise. Generally, these sorts of investments can provide low correlation to most other parts of a portfolio, liquid (e.g., liquid equities and credit investments) or otherwise. Likewise, however, broad economic movements can have adverse impacts on performance for real assets. For example, when commodity prices fall, say within the energy sector, having exposure to an energy-oriented manager may suffer as a result. These allocations can, on the other hand, act as good diversifiers and inflation hedges when needed.

How Do Investors Access Private Markets?

Historically, institutional investors have pursued several different avenues to access the private markets. They run the gamut from direct investments into companies, commingled primary funds that invest in a mix of private companies, multi-manager funds that invest in a group of investment General Partner funds, and separately managed accounts.

However, these vehicles often have high investment minimums (e.g., $5 million to $10 million), long lock-up periods (e.g., 7-15 years), or require clients to be qualified purchasers, such as institutions, endowments or ultra-high-net-worth, to invest. These features tend to present barriers for many advisors and their high-net-worth and mass affluent clients. In recent years, however, some of the large institutional private market managers have launched traditional ‘40 Act mutual fund structures to make private markets more accessible to newer groups of investor groups. These structures can help investors to build private market exposure in an efficient manner, almost akin to investing in a mutual fund structure (but built with private market assets).

Evergreen Funds

Often referred to as evergreen funds because of their perpetual fund life, investors have the ability to enter and exit these ‘40 Act vehicles throughout their existence. With some evergreen funds, the investor’s capital is immediately deployed into an already built portfolio of investments. This is quite different from traditional private investment structures, where the investor not only must access the transaction or fund, but then is required to commit capital over a multi-year period. The investor must meet capital call notices, fund its commitment, and only build private market over time (and with limited visibility at the outset). This is referred to as ‘blind pool’ risk which many evergreen fund structures have been able to largely avoid.

Thoughtfully constructing a diversified and fully invested portfolio is crucial to the success of these vehicles. For individual investors, certain evergreen fund structures may present potential advantages. Those that are in a position to deploy capital quicker can eliminate cash drag. Early deployment also gets the investor exposure to private markets sooner, a critical detail for individuals who have never had exposure, and do not have infinite investment horizons the way a pension fund or endowment might. Below are a few other differences between evergreen funds and other investment vehicles:

Investment minimums: Historically, the minimums for participating in a private equity partnership were around $5 to $10 million. Evergreen funds offer a lower entry point, typically from $50,000 to $100,000, depending on the fund and share class.

Liquidity: Traditional private equity partnerships include a 10-12-year commitment. Evergreen funds, however, may offer monthly or quarterly redemptions. Redemptions may be limited, and, typically, the fund will allow only a set percentage of total assets to be redeemed in a quarter. (As we cover later, investors should approach the asset class with a multi-year, long-term approach.) However, a vehicle that allows greater liquidity should nevertheless provide more flexibility than traditional partnerships and remove a hurdle for some individuals.

Diversification: A potential benefit of evergreen funds is that they often invest in more than one type of private market strategy. A fund may hold private credit, private equity and secondary investments, for example. This helps manage liquidity and gives the end investor broad exposure to private markets in one vehicle, instead of having to find different managers for each investment type.

Taxes: Most evergreen fund investors report the investment using a 1099. This is a simpler process than the K-1, a multipage document that is required for illiquid private partnerships.

Governance: Often filed as 40’ Act funds, evergreen funds are subject to SEC regulations, and are governed by a fund board. These measures provide an extra level of oversight that traditional investment structures do not possess.

Side-by-Side Comparison

| Traditional Private Equity | Evergreen Funds | Mutual Funds | |

| Structure | Typically closed-end limited partnerships | Open ended fund structures with no termination date; typically priced monthly | Typically open ended structure; priced daily |

| Investor Eligibility | Qualified Purchasers | Usually Qualified Clients or Accredited Investors sometimes open to all investors | Generally open to all investors |

| Capital Deployment | Multi-year commitment period | Potentially fully deployed upon investment | Fully deployed upon investment |

| Administration | Typically involves processing capital calls over five-year commitment period Often greater than $5M USD minimum commitment | No Capital Calls Lower minimum investment (e.g., 50-100k) | Daily liquidity requires strict liquidity regulation and can lead to increased volatility due to market action |

| Liquidity | 7–15-year lock-up period | Limited liquidity; Typically quarterly | Ability to redeem daily |

| Diversification | Multiple manager selection requiring resources or Fund of Funds | Diversified exposure through single allocation | Strategy specific |

| Asset Allocation | Static and difficult to maintain target allocation | Potential for diversified exposure through single allocation, but strategy specific | Either dynamic or tied to benchmark depending on strategy |

| Tax Reporting | K-1 | 1099 | 1099 |

Conclusion

There are many facets of private market investing. When looking to allocate to the space, there are different ways that managers can invest capital, different fund structures they can offer, and a host of strategies available within the private markets vertical. Likewise, looking across the spectrum, there are varying levels of risk-return offered to investors.

So, why does this all matter? We have shown the private markets may provide excess returns on a risk-adjusted basis, but when looking at managers, one must do so in the context of their broader portfolio and asset allocation guidance. Whatever the addressable concern may be, there are solutions within the private market landscape that can provide varying solutions and exposures and, ultimately, the goal is to provide outside risk-adjusted returns in that process.

In the next blog post in this series, we'll focus on evergreen funds and the questions that should be asked around portfolio construction, liquidity and fees.

Disclosures

1 Data was sourced from Cobalt.

2 Footnotes for 10-Year Asset Class Risk-Adjusted Performance: Green means the private markets have outperformed the public benchmark by the requisite 300+ basis points that most investors look for in their private portfolios. Yellow means there is outperformance, but it is less than 300 basis points.

Indices used: Hamilton Lane All Private Markets with volatility de-smoothed; Hamilton Lane All Private Equity ex. Credit and Real Assets with volatility de-smoothed; S&P 500 Index: Russell 3000 Index: MSCI World Index: HFRI Composite Index; Hamilton Lane Private Credit with volatility de-smoothed; Credit Suisse High Yield Index; Barclays Aggregate Bond Index. Assumes risk free rate of 2.0% representing the average yield of the ten-year treasury over the last ten years.

Definitions

All Private Markets: Hamilton Lane’s definition of “All Private Markets” includes all private commingled funds excluding fund-of-funds, and secondary fund-of-funds.

Credit: This strategy focuses on providing debt capital.

The S&P 500 Index tracks 500 largest companies based on market capitalization of companies listed on NYSE or NASDAQ.

The Russell 3000 Index is composed of 3000 large U.S. companies as determined by market capitalization.

The MSCI World Index tracks large and mid-cap equity performance in developed market countries.

The HFRI Composite Index reflects hedge fund industry performance.

The Credit Suisse High Yield Index tracks the performance of U.S. sub-investment grade bonds.

The Barclays Aggregate Bond Index tracks the performance of U.S. fixed rate corporate debt rated as investment grade.

Desmoothing: A mathematical process to remove serial autocorrelation in the return stream of assets that experience infrequent appraisal pricing, such as private equity. Desmoothed returns may more accurately capture volatility than reported returns. The formula used here for desmoothing is:

rD(t) = (r(t) – r(t-1)*p)/(1-p)

Where rD(t) = the desmoothed return for period t, r(t) = the return for period t, p = the autocorrelation.

The views expressed are those of the author at the time created. These views are subject to change at any time based on market and other conditions, and Hamilton Lane, disclaims any responsibility to update such views. No forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of trading intent on behalf of any Hamilton Lane portfolio.

This Hamilton Lane blog is not intended to provide investment advice. This blog should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security by Hamilton Lane, or any third-party. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your legal or tax professional regarding your specific situation.