Weekly Research Briefing: Spring Has Sprung

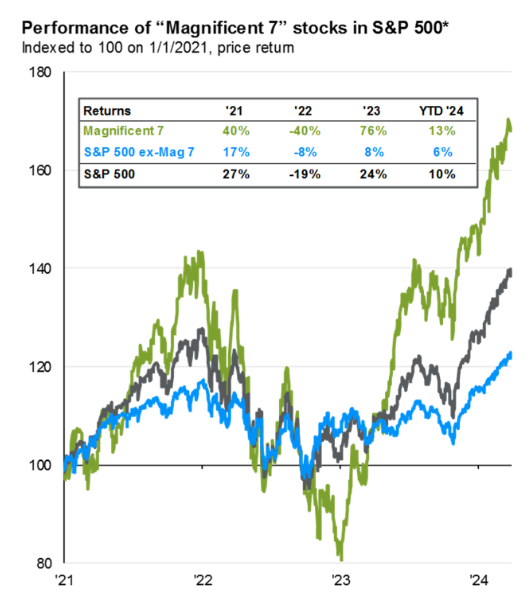

Joining the crocus in reaching for the sky last week were the equity markets which moved to new highs for the quarter end. Back-to-back double-digit percentage gains for the S&P 500 is not a frequent event and last happened in March of 2012. While the Mag-7 continued to get much of the attention, only 5 of the 7 companies outperformed the S&P 500 in the first quarter while the other 493 names managed a 6% gain. In another sign that the markets could be broadening out, the Euro Stoxx 50 nearly matched the S&P 500 on a US dollar basis for the first three months.

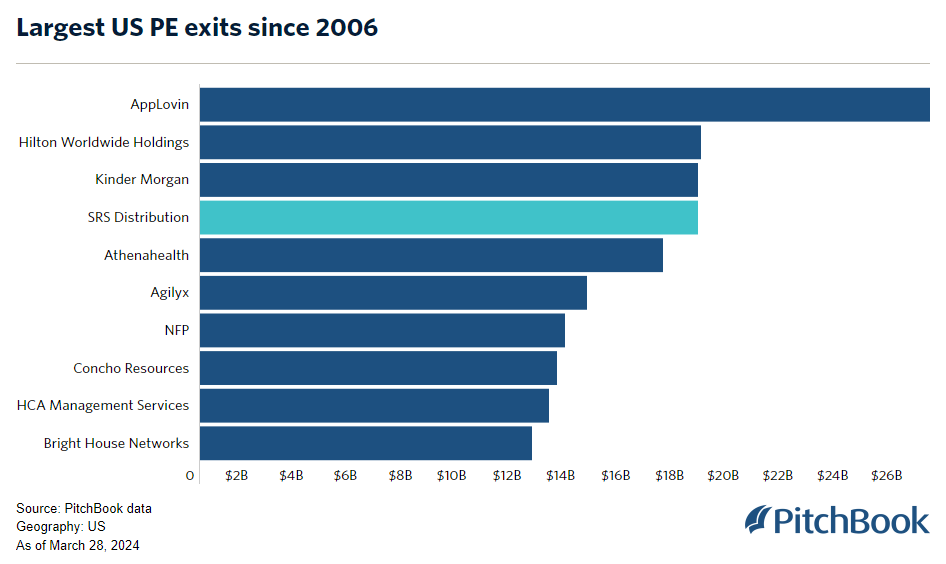

Of course, if you keep an eye on the credit and lending markets, then you already know that the global financial markets are more than just 7 companies. Credit spreads continue to narrow across most every sector and geography. Private credit firms and banks are in a war for talent that closely resembles an episode of Shogun. And deal activity continues to ramp up as the economy strengthens, cash flow generation improves and CEO's elect to pull the trigger on their favorite deals. This week it was Home Depot's turn to make a strategic move and re-enter the professional builder business in a major way by acquiring SRS Distribution. Home Depot will use its solid balance sheet and cash flow to make the $18 billion purchase. And with one fell swoop, HD will return $13 billion to the private equity markets which amounts to 10% of all PE exit value in the Q4 of 2023. Don't try and tell me that money will not be returning to PE investors this year.

The economic data continues to surprise. Monday's March ISM manufacturing data series finally woke up from its 20-month slumber. This followed China's surprising manufacturing and services strength over the weekend. At the same time, Friday's PCE inflation series (a Fed favorite) showed further slowing. So, a tug-of-war between economic growth and inflation continues to build. No idea which way the end result will break, but the good news is that the strengthening U.S. economy combined with falling inflation will give the Fed more options versus the alternative. Lots of Fed speak this week so maybe some signals from the hawks and doves. Since this week is the first of the month, we will get the monthly jobs data on Friday. Let's see if the NFP number cools from last month's hot +270,000 pace. Enjoy this great weather and the flowers and have a great week.

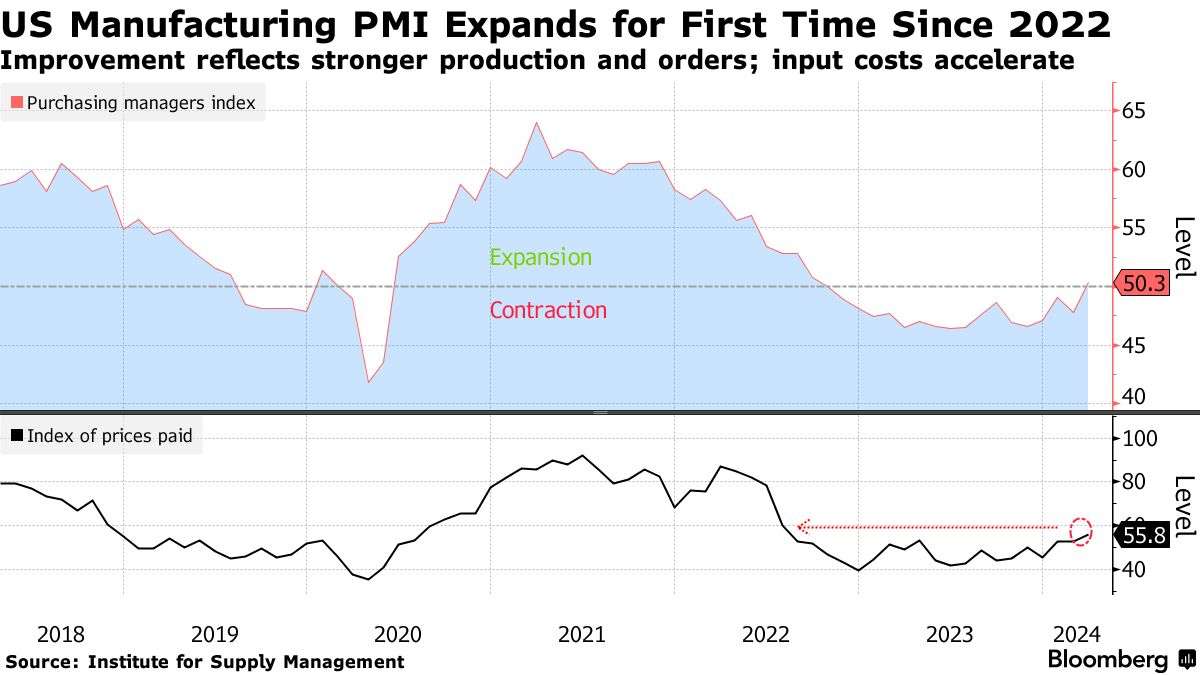

Manufacturing bosses are finally seeing their businesses blossom...

US factory activity unexpectedly expanded in March for the first time since September 2022 on a sharp rebound in production and stronger demand, while input costs climbed.

The Institute for Supply Management’s manufacturing gauge rose 2.5 points to 50.3 last month, according to data released Monday. While barely above the level of 50 that separates expansion and contraction, it halted 16 straight months of shrinking activity.

The March index exceeded all estimates in a Bloomberg survey of economists.

Production snapped back sharply from a month earlier with a gain of 6.2 points that was the largest since mid-2020. At 54.6, output growth was the strongest since June 2022.

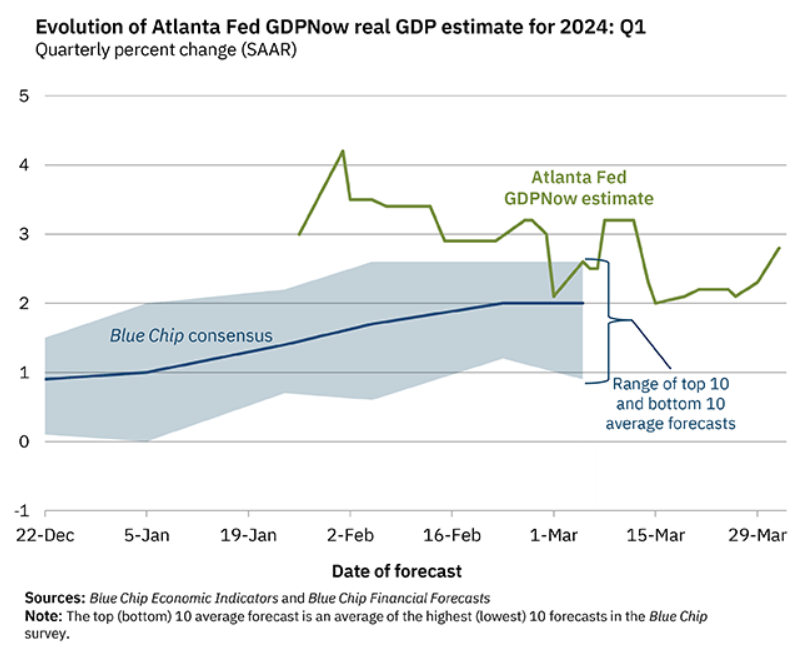

Today's ISM surprise pushing the Atlanta Fed's GDP now estimate back up toward 3% for the Q1...

Latest estimate: 2.8 percent -- April 01, 2024

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2024 is 2.8 percent on April 1, up from 2.3 percent on March 29. After this morning’s releases from the US Census Bureau and the Institute for Supply Management, the nowcasts of first-quarter real personal consumption expenditures growth and first-quarter real gross private domestic growth increased from 2.6 percent and 3.1 percent, respectively, to 3.2 percent and 3.9 percent.

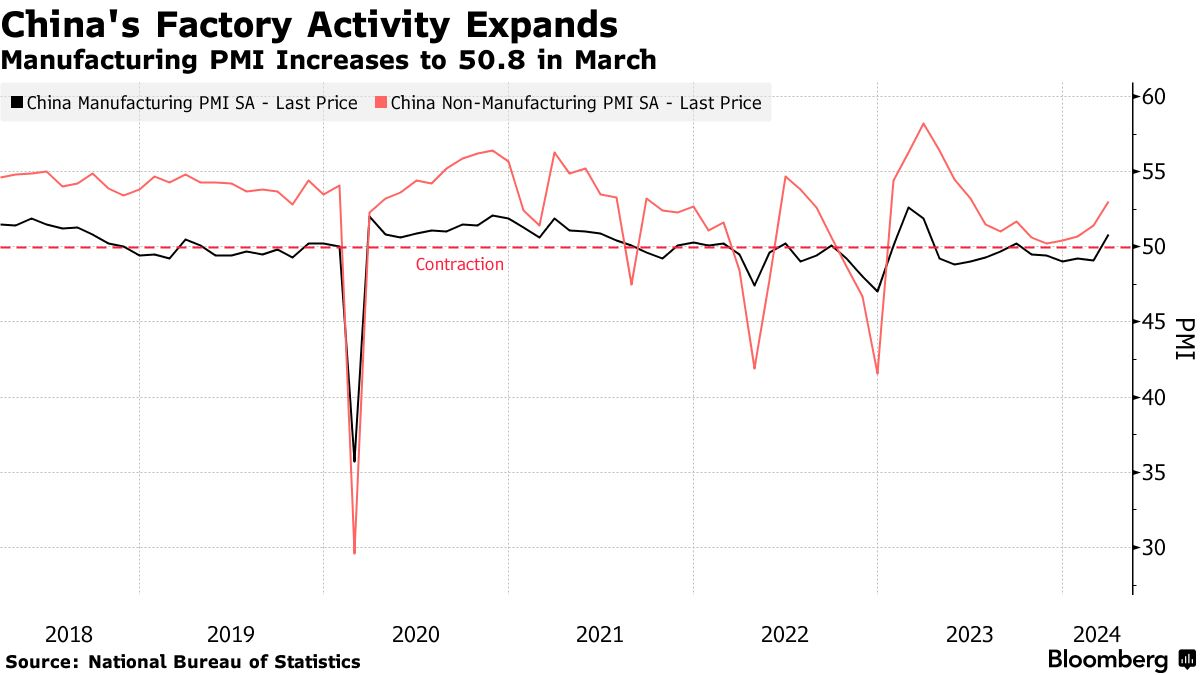

The first read on March activity in Chinese manufacturing, also surprises to the upside...

China’s manufacturing activity expanded in March for the first time since September, a further sign that the world’s second-largest economy is stabilizing.

The official manufacturing purchasing managers index rose to 50.8 from 49.1 in February, the National Bureau of Statistics said in a statement Sunday. That beat the median forecast of 50.1 by economists in a Bloomberg survey and was the best reading since March last year.

A gauge of non-manufacturing activity climbed from the previous month to 53, compared with an estimate of 51.5. A reading above 50 suggests an expansion from the previous month, while a figure below that denotes contraction.

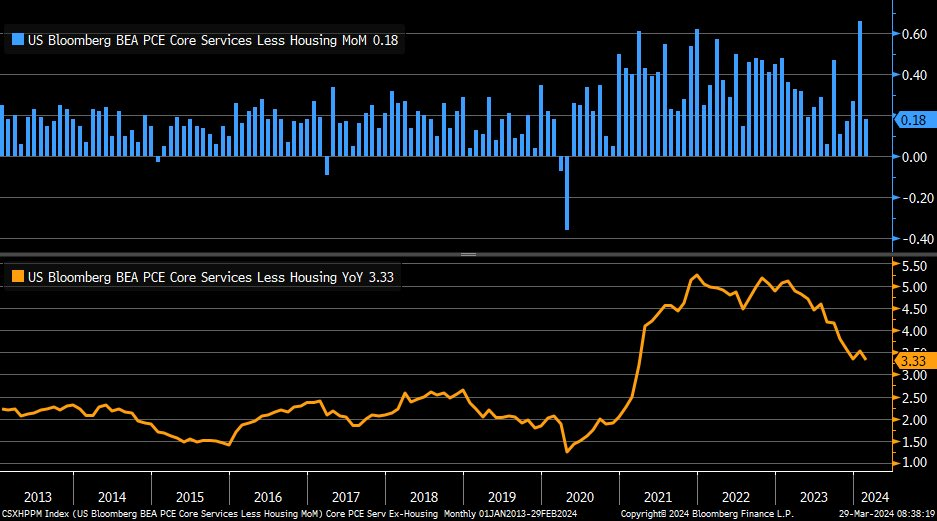

Friday's February PCE inflation figure came in slightly below expectations. Most importantly, the supercore PCE continued to slow...

@LizAnnSonders: So-called “supercore” PCE (core services ex-housing) #inflation increased by +0.18% month/month (blue) in February, a huge step down from prior month’s gain … year/year change (orange) eased to +3.33%

Fed Chair Powell gave us some insight on Friday after the PCE data was released...

(US) Fed Chair Powell: Fed is not under pressure to cut rates, but waiting too long could mean unneeded damages to the economy and the labor market; Still expect inflation to come down on a sometimes bumpy path to 2%

- Fed wants to see more good inflation readings before it can cut rates

- Rate decisions are not fully backed before the policy meeting

- Asked if he would ever be ready to declare victory over inflation: "We'll jinx it; I'm a superstitious person.''

- US banking system in a good place now

- Fed is ready for the economy to perform in unexpected ways; If begin to see unexpected weakness in the labor market “that would draw a policy response”.

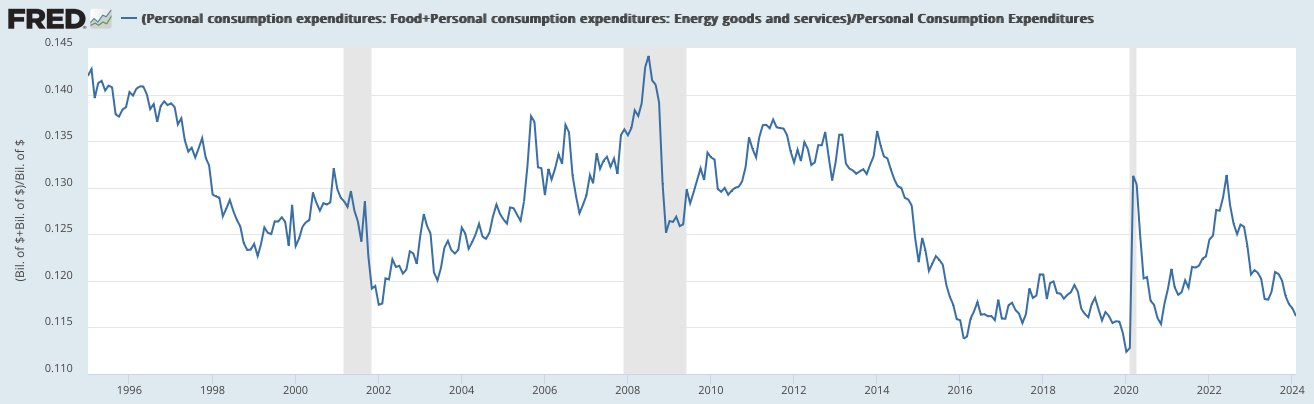

Good news for households as spending on food and clothes is near 30-year lows...

@conorsen: Put those together -- spending on food and energy as a % of total spending are actually closer to historic lows than normal, let alone extremes on the high end:

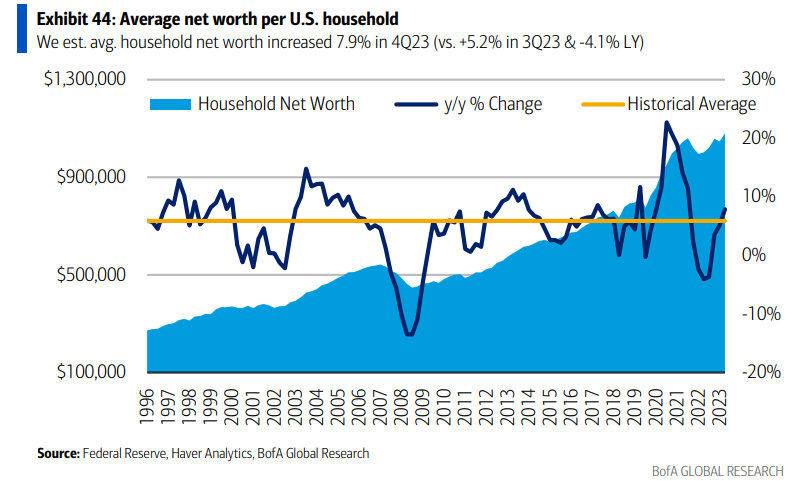

Higher home and stock prices combined with static debt have sent net household worth to a new high...

BofA Global

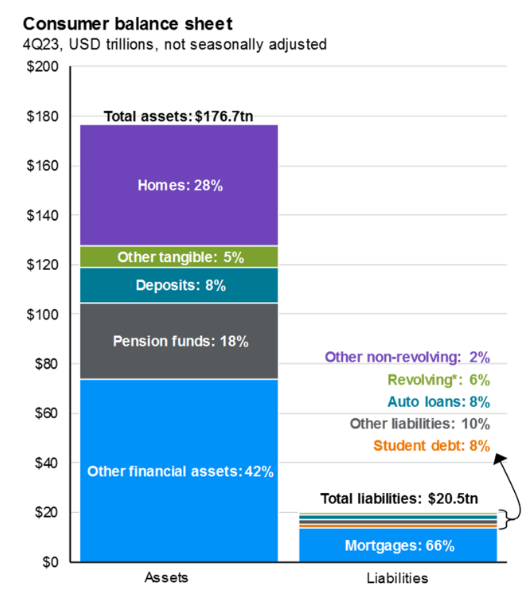

For a full picture of the consumer balance sheet...

Consumers aren't the only ones with strong balance sheets. Corporations have them also and are now getting to work using them...

“We’re back to average, or back to normal,” said Andre Kelleners, Goldman Sachs head of M&A in Europe, the Middle East and Africa. “We’ve seen a real, robust rebound from exceptionally low levels this period a year ago.”

Among the largest deals struck in the quarter were Capital One’s $35bn acquisition of Discover Financial, and chip design toolmaker Synopsys’s $35bn takeover of engineering software maker Ansys.

M&A has increased in anticipation of rate cuts from central banks, which investors bet could come as early as June. That has made financing for deals easier and cheaper to obtain, while IPOs have started to return to public markets that are trading at record highs.

“It’s clearly a better environment from a transaction point of view,” said Massimiliano Ruggieri, head of Emea investment banking at Morgan Stanley. “You can definitely point to a higher level of engagement from clients, both investors and issuers, that has continued throughout the quarter.”

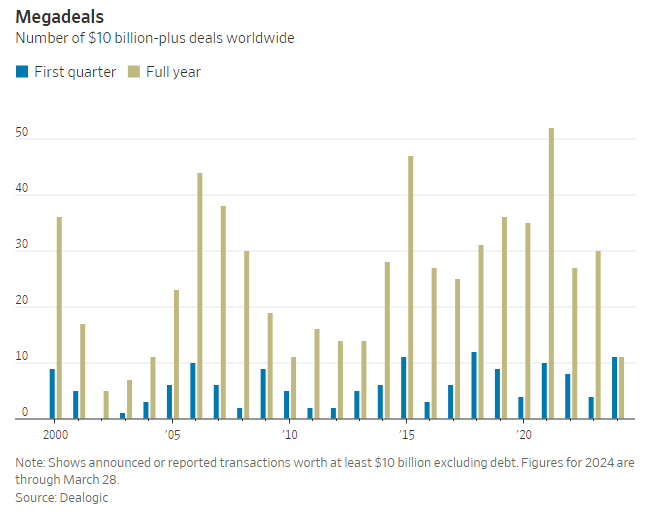

Blockbuster sized deals have returned to the marketplace...

Led by Capital One Financial’s $35.3 billion purchase of Discover Financial Services, buyers have unveiled 11 deals worth $10 billion or more this year, excluding debt, according to Dealogic, a data provider. That makes this one of the busiest starts to the year for monster takeovers this century.

On Thursday, Home Depot said it was making a big bet on SRS Distribution, a private-equity-owned roofing distributor, adding to the rush of deals.

The flurry of supersize acquisitions reflects a broader recovery. Last year, overall dealmaking value hit a decade low. Higher borrowing costs due to the Federal Reserve’s rate hikes made it more expensive to fund acquisitions, while stock-market swings challenged the ability of buyers and sellers to agree on price.

But global activity has resurged and total deal value is up 24% so far this year to $725.8 billion, bolstered by steadier interest rates and rising stock prices.

“History shows we are in the early innings of a cyclical M&A rally,” said Andre Kelleners, the head of M&A for Europe, the Middle East and Africa at Goldman Sachs. He pointed to a halving in deal volume in the past two years.

Home Depot sees a big win in its acquisition of SRS Distribution. Private equity and lenders also will see a big win from this $18b purchase...

Home Depot is placing an $18 billion bet that will take the retailer beyond its big orange stores.

The home-improvement retailer said Thursday it would buy a company that sells goods for professional roofing and other building projects, branching out to grab more spending by big contractors and construction firms.

Home Depot said it would acquire SRS Distribution, in a deal with an enterprise value of $18.25 billion. That figure includes SRS’s roughly $5.8 billion of debt. Home Depot expects SRS’s debt to be paid once the deal closes.

SRS is owned by private-equity firms and has been buying up local and regional distributors that it operates under their own brands. It has 760 locations and 4,000 trucks that bring materials to job sites. SRS had about $10 billion in revenue last year.

Over the past year, Home Depot has worked to build up what it calls its complex pro business, contractors working on large projects that typically purchase the bulk of their supplies through wholesale or specialty distributors such as SRS.

The strategic shift comes as Home Depot, which has about 2,300 stores, faces declining sales in its core retail business. Booming sales earlier in the pandemic subsided over the past year. The retailer’s sales fell 3% to $152.7 billion last year.

With this one deal, Home Depot will return PE capital equal to 10% of all PE exits in the Q4 2023...

This will also make for the largest PE exit in 18 years. A great win for Leonard Green & Partners and Berkshire Partners.

Away from the mega-deals, there are several strategic deals hitting the tape in the U.K. also...

Bidding wars are suddenly fashionable in London. While stock markets elsewhere have been busying themselves with record highs or a resurgent IPO market, the City has become the scene of fierce battles for unloved companies.

Spirent is the latest. As the City fretted over the future of Thames Water last week, the telecoms testing company said that it had agreed a 201.5p per share offer from US testing group Keysight, which valued its equity at £1.16bn. The bid trumped an earlier proposal from Viavi Solutions, which had agreed a 175p per share offer with the Spirent board. Viavi has criticised this new deal, saying it would “limit customer choice”.

Spirent was not the only UK business heading into Easter with rival suitors looking daggers at each other. Packaging group DS Smith said last week it was in talks over a 415p per share bid from US-listed International Paper, which would beat an earlier offer from local rival Mondi that had been agreed in principle. Neither has made a formal bid yet.

And in February, logistics group Wincanton left French suitor CMA CGM at the altar, preferring instead to recommend a £762mn offer from GXO.

What all these deals have in common, as well as their contested nature and the joy they have brought to (in some cases long-suffering) shareholders, is the nature of the combatants. All six suitors in the three deals are trade buyers in the same industry, rather than private equity firms or sovereign wealth funds.

PE still involved on the buying side of the equation when a stock becomes ignored and discarded as was the case with Nuvei Corp...

April 1 (Reuters) - Private equity firm Advent International has agreed to buy Canada's Nuvei, opens new tab in a deal that values the payments technology firm, which has received financial backing from actor Ryan Reynolds, at $6.3 billion.

The deal, valued at $34 per share, will take Nuvei private almost four years after the company was listed on the Toronto Stock Exchange.

The buyout of Nuvei, which has a market capitalization of nearly C$6 billion ($4.42 billion), would make it one of the more sizable take-private deals at a time when private equity dealmaking has slowed.

It represents a premium of 56% to the company's closing price on the Nasdaq before a potential deal was reported in the media in mid-March.

Current CEO Philip Fayer will continue to lead the company and Nuvei will remain headquartered in Montreal, it said.

Nuvei provides payments technology to businesses, allowing them to pay and accept payments regardless of their customers' location or preferred payment method.

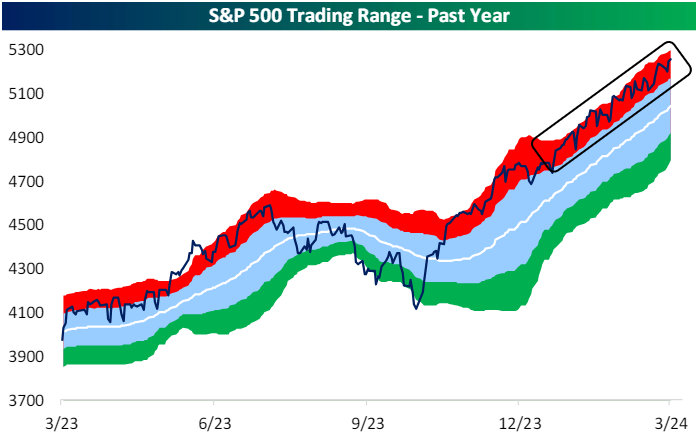

As for the public equity markets, they remain in overbought territory. And there is no rule that says this cannot continue...

@bespokeinvest: The S&P 500 has closed in overbought territory (>1 st. dev. above its 50-DMA) for 50 consecutive trading days. The last time the index had a longer streak of overbought closes was more than 25 years ago in April 1998 (60).

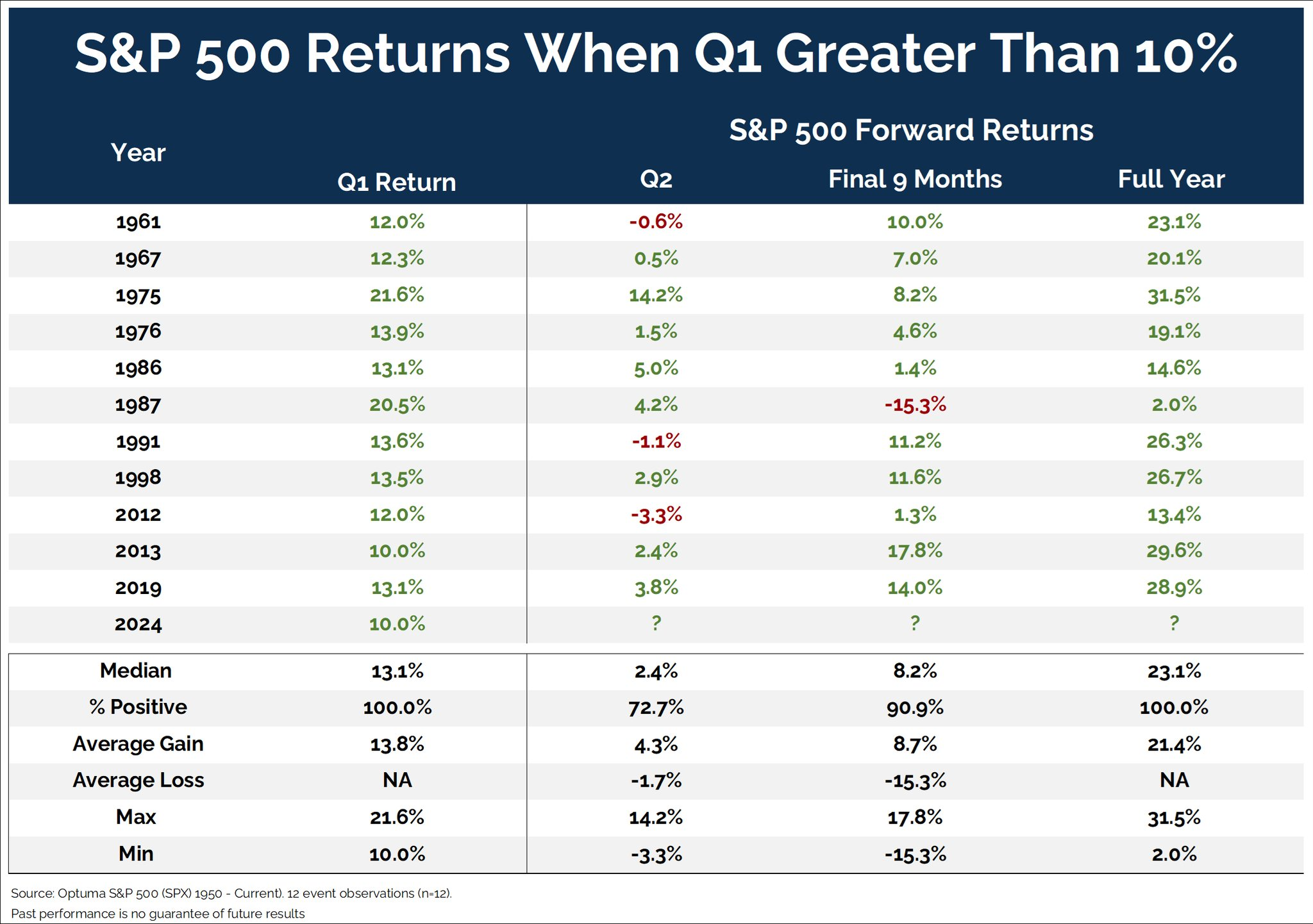

The first quarter is a closely watched signal for the rest of the year...

And typically, this ball in motion will stay in motion through the rest of the year which should be good news for all animal spirits and risk takers.

@granthawkridge

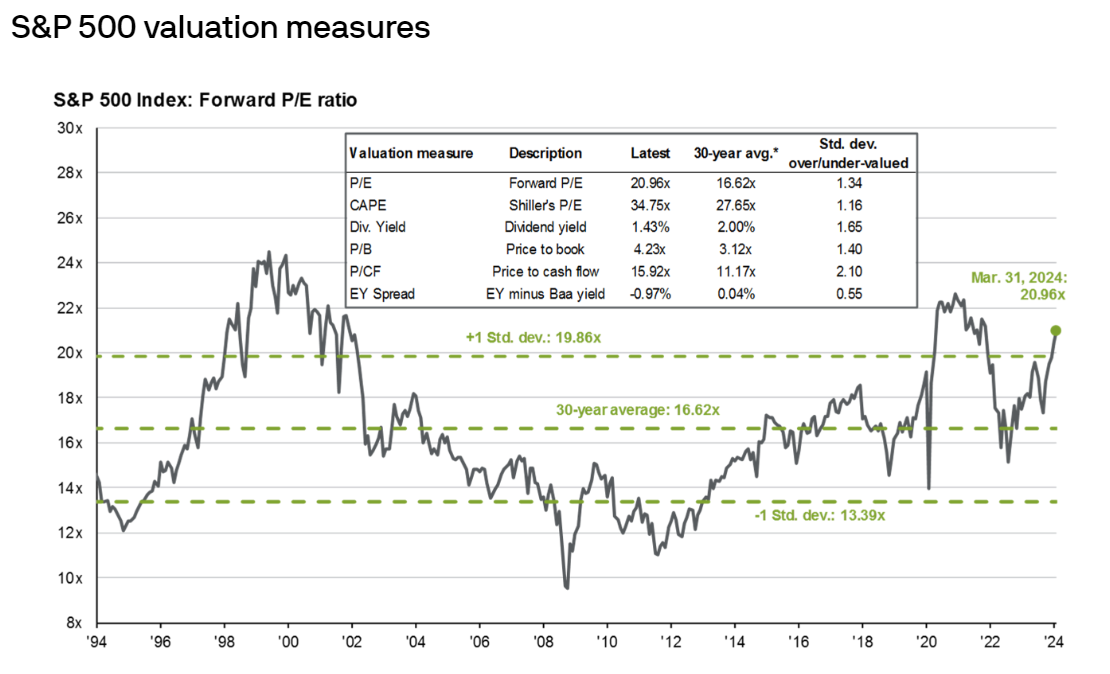

Fact: the S&P 500 is not cheap.

But until something breaks the credit markets, I see no reason to bet for it to get cheap.

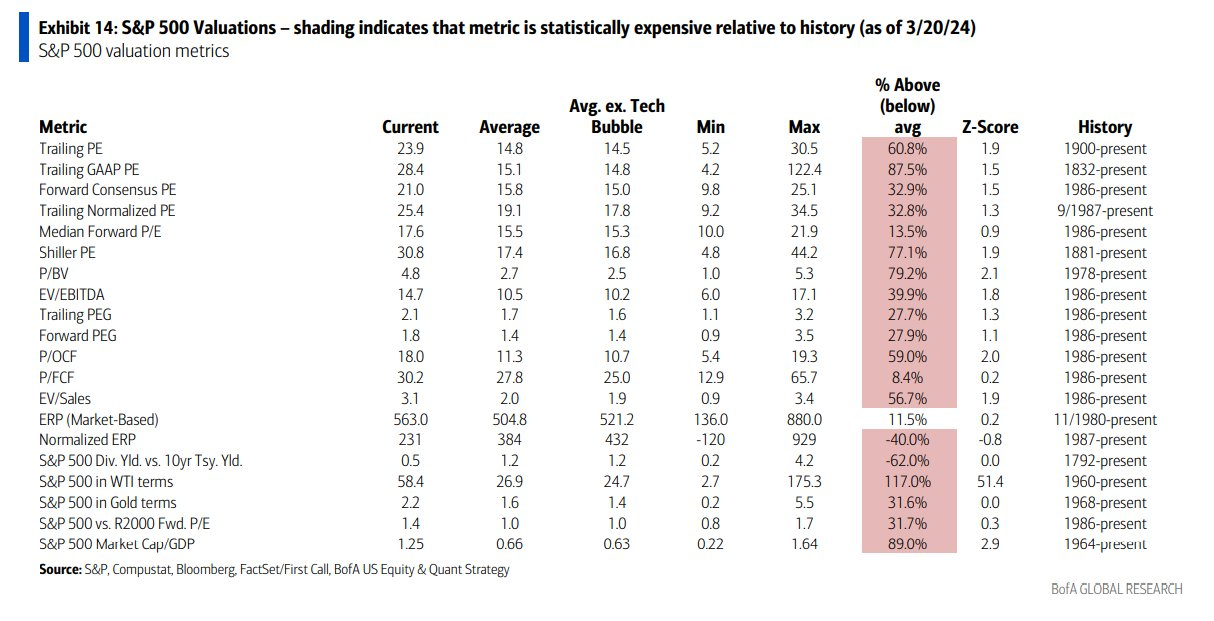

A full look at where all the valuation measures stand...

14.7x EV/EBITDA is a bit rich. 30x FCF is not that rich.

BofA Global

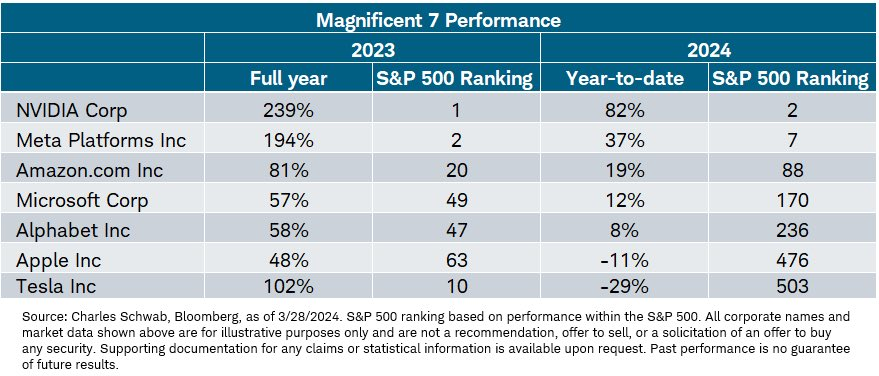

I know that you want to see details on the Mag-7...

Did you ever think that the S&P 500 could return +10% in a quarter where Apple was down double digits?

@LizAnnSonders

The good news is that the performance gap between the Mag-7 and the 493 is no longer accelerating wider...

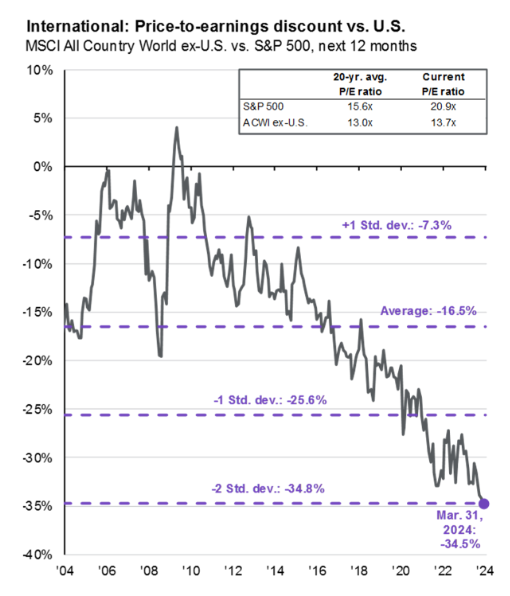

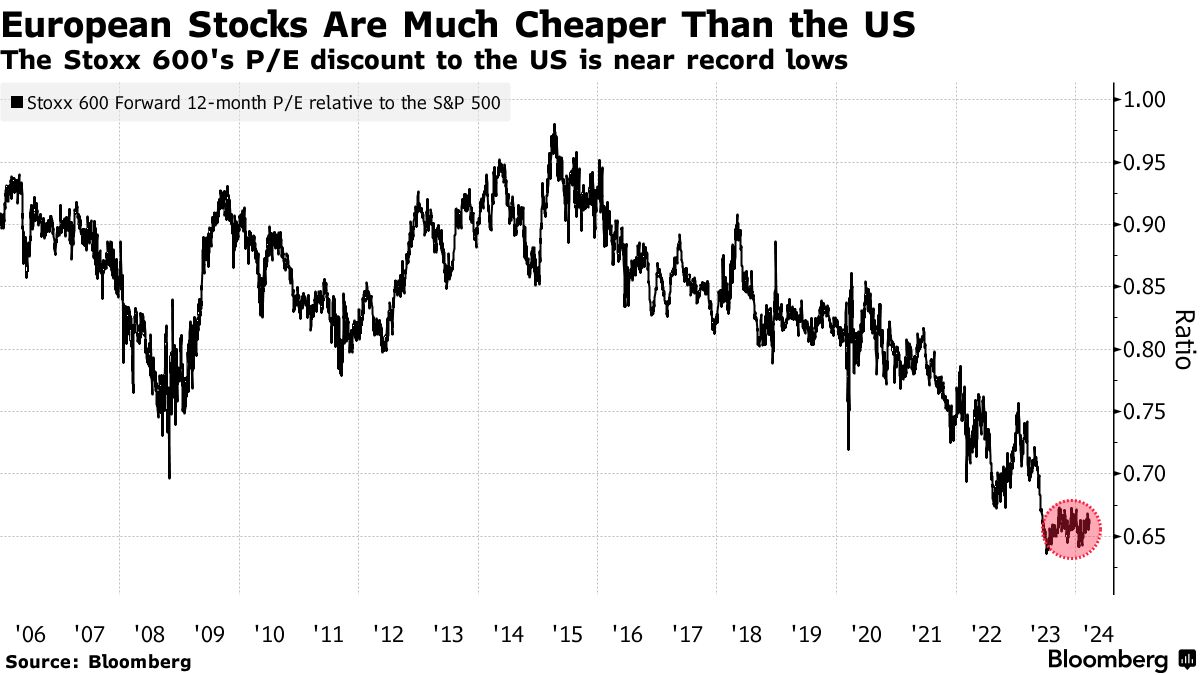

Two standard deviations wide now between U.S. and Int'l P/E valuations...

I know the mix of industries is very different, but this discount is beyond extreme.

The smartest public investors are now moving to take advantage of the European P/E discount...

Hedge funds are now the most exposed they have ever been to European stocks relative to a global benchmark, according to Goldman Sachs Group Inc. data. Mutual funds have also amped up allocations to the region’s equities by the most since June 2020, a recent survey by Bank of America Corp. showed.

The prospect of “Europe’s outperformance against US stocks certainly has legs,” Paul Brain, deputy chief investment officer of multi-asset at Newton Investment Management, said in an interview in London. “US big tech seems fully priced and may run into headwinds from competition and regulation after the recent rally.”

Euro area shares have risen by around 4% in March, outpacing their US peers, and investors expect them to keep climbing if a rebound in economic growth revitalizes corporate profits. That’s as the artificial intelligence fervor gripping the US market makes the fortunes of the S&P 500 Index increasingly reliant on a group of relatively expensive tech stocks.

Hedge funds’ allocation to Europe versus the MSCI All-Country World Index reached 5.8% overweight last week, the highest level on record, according to the Goldman Sachs data.

Despite Europe’s gains this month, its benchmark Stoxx 600 Index still looks cheap. Its forward 12-month price-to-earnings ratio of about 14 is only slightly higher than its long-term average, according to data compiled by Bloomberg. Even excluding richly valued tech stocks, the S&P 500 is in expensive territory.

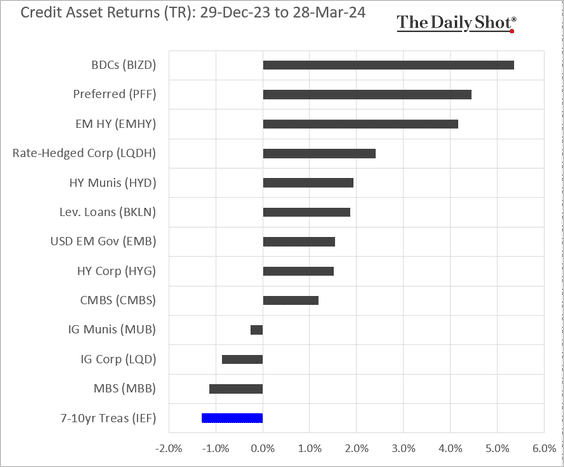

The risk-on environment in the Q1 also benefitted credit risk instruments for the three months...

The riskier, the better as narrowing credit spreads offset duration risk in most asset categories. We don't have private credit results yet, but you can guess where they might fall among their public cousins below: HYG/BKLN/BIZD.

You won't get away from the WRB without reading an article about how AI is helping make boring industrial companies better...

Companies growing more comfortable with artificial intelligence are bringing the latest tools into their supply chains, with goals of cutting costs, speeding up distribution and getting ahead of potential disruptions...

German software firm Celonis is working with snack-food supplier Mars to use generative AI to combine truck loads, cutting shipping costs and speeding up delivery.

Celonis Chief Executive Alex Rinke said Mars had manually evaluated factors such as the weather to determine which shipments could be combined and whether it needed to use refrigerated trucks for its freight.

With AI, “we can proactively tell them, ‘Here are all the truck loads that you have going out that you should consolidate,’” Rinke said. “That reduced manual touches by 80% and also made them more efficient as a company because they reduced shipping costs, reduced emissions and improved on-time shipments.”

Rinke said another company is using the technology to compare its contracts with suppliers against its final bills to make sure it isn’t missing out on rebates or discounts. That was previously a time-consuming process in which employees manually sifted through contracts.

“You get a really, really good understanding of where you have opportunities to save money because maybe you have better terms in your contracts than you are actually using,” he said.

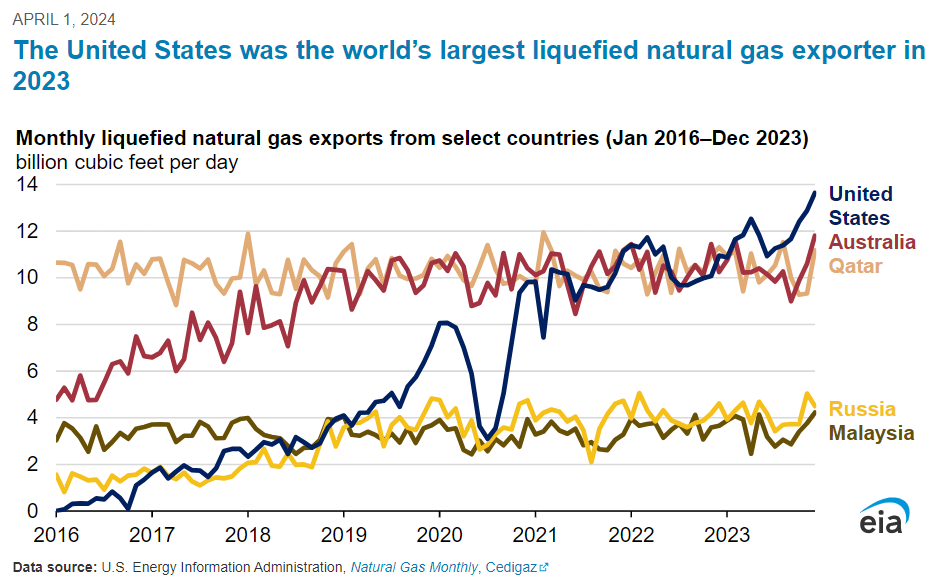

And while the world goes on a hunt for more power to fuel AI, the U.S. has now become number one in LNG exports...

The United States exported more liquefied natural gas (LNG) than any other country in 2023. U.S. LNG exports averaged 11.9 billion cubic feet per day (Bcf/d)—a 12% increase (1.3 Bcf/d) compared with 2022, according to data from our Natural Gas Monthly...

U.S. LNG exports increased in the first half of 2023 after Freeport LNG returned to service in February and ramped up to full production by April. Relatively strong demand for LNG in Europe amid high international natural gas prices supported increased U.S. LNG exports during the year. U.S. LNG exports set monthly records late last year: 12.9 Bcf/d in November, followed by 13.6 Bcf/d in December. We estimate that utilization of U.S. LNG export capacity averaged 104% of nominal capacity and 86% of peak capacity across the seven U.S. LNG terminals operating in 2023.

If United is offering pilots unpaid time off in May and through the summer, then you had better plan ahead for any summer travel...

United's reliance on Boeing deliveries is coming at a bad time with the consumer and business economy recovering so strongly. Expect plenty of cancellations and full prices this year.

BofA Global

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: Home Depot Inc.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.